The Surplus of Oil That Was Expected but Didn’t Occur

The Myth of a 2026 Oil Glut: Separating Fact from Forecast

With every market cycle comes a reassuring narrative—this time, for 2026, it’s the “inevitable oil glut.” The argument centers on rising crude output, continued Iranian exports despite sanctions, and speculation that OPEC+ may gradually increase production. The prevailing belief is that excess supply will soon overwhelm the market, leading to falling prices. Yet, when examining the physical oil market, this scenario doesn’t hold up. There’s little evidence of storage tanks filling up or a surge in floating storage. OPEC+ shows no signs of reckless production increases, and tanker freight rates suggest that supply security, not oversupply, is the market’s main concern. In reality, the so-called glut seems to exist only in analysts’ models, not in the real world.

What a True Oil Glut Looks Like

Historically, a genuine oil surplus is marked by steadily rising OECD inventories, a futures curve that slips into deep contango, and producers—especially OPEC+—cutting official selling prices to clear excess barrels. Tankers would be left idle, unable to find buyers for their cargoes. These patterns were clear in 2015–16 and again in 2020. Today’s market, however, doesn’t resemble those periods.

Forecasts vs. Reality

Despite this, many institutional outlooks still predict that oil supply will outpace demand in 2026. The International Energy Agency (IEA) expects global oil demand to grow by 850,000 barrels per day, while supply could rise by 2.4 million barrels per day, suggesting a surplus. The U.S. Energy Information Administration (EIA) also anticipates global inventories will build by over 3 million barrels per day this year. On paper, these numbers point to a glut. But for such a surplus to be real, it must show up as consistent, visible increases in storage—not just in forecasts.

Inventory Data Paints a Mixed Picture

Current inventory figures tell a more nuanced story. U.S. weekly data has been volatile, with one week showing a massive 16-million-barrel build—the largest in three years—while another reported a 9-million-barrel draw, reflecting tighter gasoline and distillate stocks. This back-and-forth doesn’t fit the pattern of a market flooded with oil. Instead, it points to a system where refinery activity, import schedules, and weather disruptions interact with tight logistics. OECD stocks haven’t surged, and Goldman Sachs recently raised its late-2026 price outlook, citing lower-than-expected inventories. In short, a surplus that doesn’t appear in storage isn’t a surplus at all—it’s just a forecast waiting for confirmation.

Floating Storage and OPEC+ Actions

Floating storage offers another reality check. In past gluts, tankers were used as makeshift storage, with oil sitting offshore in plain sight. Currently, about 900 million barrels are stored on water worldwide—a decrease from recent highs and far from crisis levels. If a true glut were underway, these numbers would be climbing rapidly. Recent moves by Saudi Arabia, Iran, and other Gulf exporters are more about hedging against potential U.S. military action than dealing with oversupply.

OPEC+ behavior further supports this view. If members believed a glut was imminent, they would be aggressively defending market share. Instead, the group is considering only a modest 137,000 bpd increase for April—a cautious approach. Saudi Arabia’s export boost in February was a strategic move to mitigate risks from possible U.S.-Iran tensions, not a sign of panic. The group is maintaining spare capacity as a tool, not abandoning it.

Tanker Rates Signal Tightness, Not Surplus

Freight rates reinforce this interpretation. Tanker earnings on Middle East–Asia routes have soared above $200,000 per day, and the Baltic Exchange’s dirty tanker index has climbed sharply, both driven by heightened Iran-related risks. Such spikes are not typical of an oversupplied market. Instead, they reflect precautionary bookings, higher war-risk premiums, and exporters moving oil early to avoid potential disruptions. High freight costs act as a tightening mechanism, making some shipments uneconomical and slowing the movement of barrels. A true glut would require frictionless placement of excess oil, which is not the case today.

Geopolitical and Investment Constraints

Geopolitical factors, especially involving Iran, add to market fragility. About a third of OPEC+ output is affected by sanctions, military threats, or political instability. Prices are sensitive to shocks, and any escalation around the Strait of Hormuz could sharply reduce tanker capacity and tighten supply, even if production remains steady. A market with such vulnerabilities cannot be described as oversupplied.

Investment trends also matter. Global upstream oil and gas investment is expected to fall below $570 billion in 2026, with around 40% of that needed just to offset natural declines in existing fields. There’s no sign of excessive overbuilding—current spending barely maintains output. Without ongoing investment in new projects, supply growth projections become increasingly uncertain, especially given risks of delays, cost overruns, or geopolitical setbacks.

Demand Remains Resilient

On the demand side, pessimism has not matched reality. Global oil consumption continues to grow outside the OECD, driven by sectors like petrochemicals and aviation. Even with modest demand growth, prices remain supported in a market constrained by investment and geopolitical risks. The bull case doesn’t require booming demand—just enough to keep the market balanced in the absence of a safety cushion.

Market Psychology and Risks

In a true glut, markets would ignore risk. Instead, oil prices react quickly to geopolitical developments, OPEC+ statements move benchmarks, and tanker routes are closely watched. These behaviors don’t reflect a market awash in oil, but one that remains sensitive to shocks.

Challenges to the Glut Narrative

Some still argue that non-OPEC supply growth, especially from the U.S. and Brazil, will overwhelm demand. However, U.S. shale expansion has slowed due to capital discipline and rising costs, while Brazil’s offshore projects are unlikely to deliver enough barrels to create a structural surplus, especially amid ongoing geopolitical uncertainty. Russian flows are also under pressure from sanctions, shadow fleets, and rerouting costs, with Ukrainian attacks further disrupting production.

Other Complicating Factors

Quality and refining capacity add further complexity. A surplus of one crude grade doesn’t translate to a universal glut. Differences in crude quality, refinery configurations, and regional demand can create local shortages even when overall supply appears comfortable. A glut based on oil that can’t be efficiently processed is not a true economic surplus—it’s a mismatch.

Freight market trends highlight this point. Expanded Middle Eastern exports increase shipping distances and tighten vessel availability, especially as exporters book ships early to avoid disruptions. Rising freight costs act as an additional tax on supply chains, reinforcing the idea that the system has little slack.

No Guarantees of a Bull Market

None of this guarantees a sustained bull market for oil. Demand could weaken if global economic growth slows or if diplomatic breakthroughs with Iran reduce risk premiums. OPEC+ could also misjudge the balance and overshoot production. Still, the narrative of an inevitable glut is hard to reconcile with current evidence: floating storage isn’t surging, inventories aren’t ballooning, OPEC+ isn’t panicking, and freight rates aren’t collapsing. Geopolitical risks remain elevated, and upstream investment isn’t booming. These are not the hallmarks of a market drowning in crude. Instead, the market could tighten quickly if just one variable changes.

The Real Risk: Market Fragility

The greatest danger for policymakers, industry, and consumers is not underestimating a surplus, but underestimating the market’s fragility. With limited spare capacity, low investment, and ongoing geopolitical risks, the oil market could turn bullish not from a major shock, but simply from the lack of a safety margin.

Conclusion: The Glut Exists Only on Paper

The “oil glut” of 2026 may persist in forecasts and models, but in the real world—where oil is stored and shipped—abundance is nowhere to be seen.

By Cyril Widdershoven for Oilprice.com

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Palantir - Starting the bullish reversal soon!

Reading Intraday Character After Emotional opens

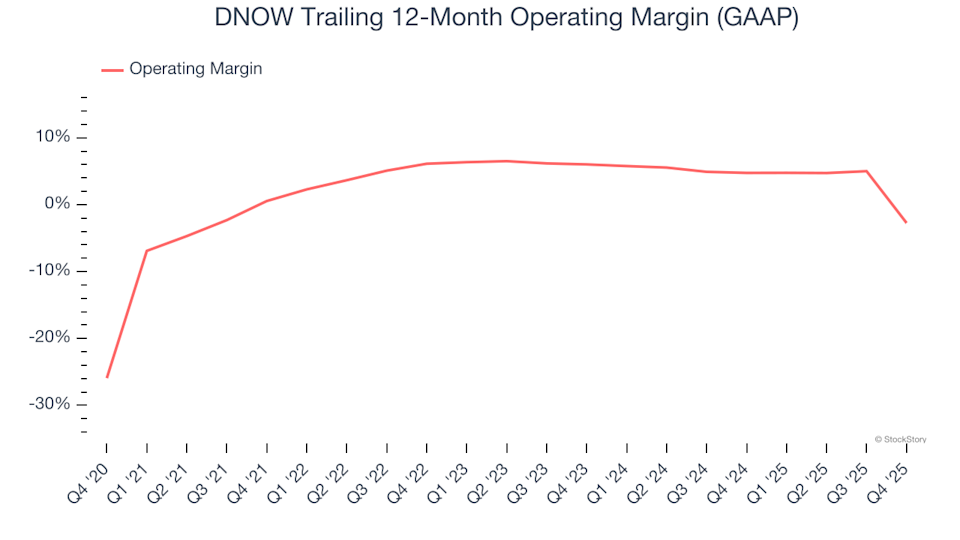

3 Reasons Why DNOW is a Risky Choice and One Alternative Stock Worth Buying

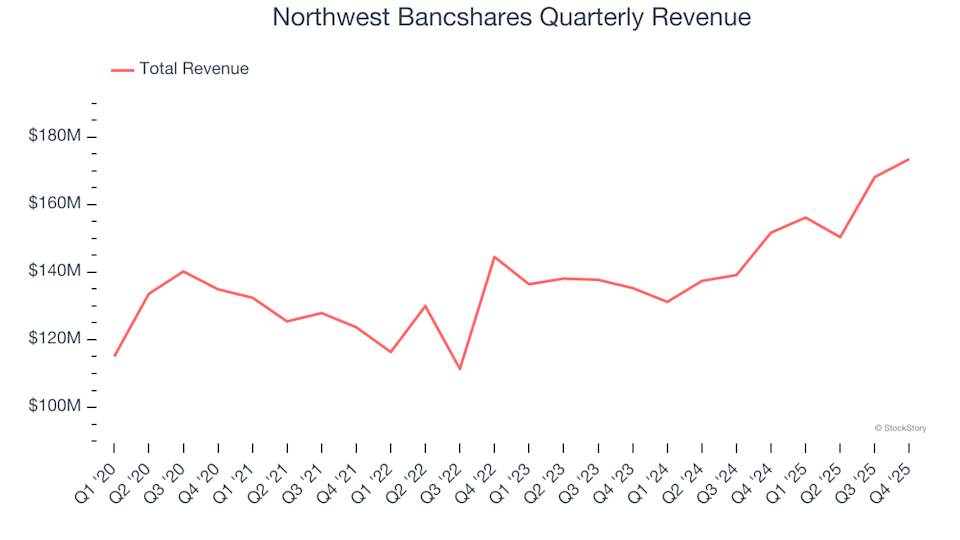

3 Reasons to Steer Clear of NWBI and One Alternative Stock Worth Buying