Western Digital's Strong Earnings Beat and $4B Buyback Can't Offset 0.90% Drop as $2.78B Volume Ranks 40th in Market Activity

Market Snapshot

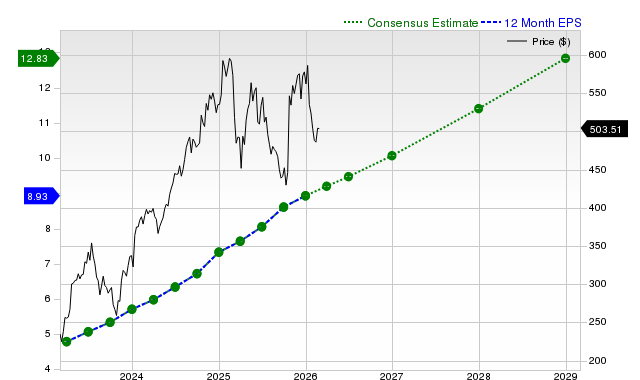

Western Digital (WDC) closed 0.90% lower on 2026-02-27, with a trading volume of $2.78 billion, ranking 40th in market activity for the day. Despite a strong earnings report—surpassing expectations with $2.13 earnings per share (EPS) and $3.02 billion in revenue—the stock faced downward pressure. The company’s 25.2% year-over-year revenue growth and a net margin of 35.52% highlighted operational strength, yet the price decline suggests short-term skepticism or profit-taking after a prior rally. The stock’s 52-week range ($28.83–$309.90) and a beta of 1.80 indicate heightened volatility compared to the broader market, consistent with its exposure to cyclical storage demand and AI-driven infrastructure trends.

Key Drivers

Earnings Beat and Strategic Buybacks

Western Digital’s Q1 2026 earnings report underscored resilience, with $2.13 EPS outpacing the $1.93 consensus and revenue reaching $3.02 billion, a 25.2% year-over-year increase. The cloud segment accounted for 89% of total revenue, driven by 215 exabytes shipped to customers—a 22% YoY jump. These results, coupled with a 35.5% net margin and 41.5% return on equity, demonstrated strong profitability. However, the stock’s 0.90% decline on the day suggests mixed investor sentiment. A key positive catalyst was the board’s authorization of an additional $4.0 billion in share buybacks, signaling confidence in cash flow and reinforcing balance-sheet strength. Analysts noted that the buyback expansion, combined with a multi-year HDD roadmap targeting 40TB UltraSMR and 100TB+ HAMR drives for AI/data centers, positioned WDCWDC-0.90% as a long-term beneficiary of the storage boom.

Analyst Optimism and AI-Driven Roadmap

Recent analyst activity further fueled bullish sentiment. Wedbush, JPMorgan, and Mizuho all raised price targets, with Wedbush setting a $325 objective and JPMorgan upgrading from $94 to $175. Zacks added WDC to its top growth/momentum lists, while Morgan Stanley and Wells Fargo highlighted its strategic positioning in AI infrastructure. The company’s Innovation Day roadmap, emphasizing high-capacity, cost-effective HDDs for cloud and AI workloads, reinforced its competitive edge. Management’s focus on HAMR (Heat-Assisted Magnetic Recording) and ePMR (Enhanced Perpendicular Magnetic Recording) technologies aligns with growing demand for scalable storage solutions, particularly in data centers. CEO Irving Tan’s emphasis on AI as a “strategic enabler” underscored the company’s commitment to capturing market share in this high-growth segment.

Dividend and Buyback Dynamics

Western Digital’s dividend announcement also drew attention, with a $0.125 per share quarterly payout yielding 0.2%. While the dividend payout ratio of 5.02% remains conservative, the buyback authorization and recent insider transactions—such as a $4.0 billion repurchase—highlighted management’s prioritization of shareholder returns. However, near-term risks emerged, including plans to monetize the remaining SanDisk stake, which could create equity overhang. Insider sales by executives and directors, though small in scale, added short-term selling pressure. Analysts debated whether these actions signaled caution or capital optimization, with some noting that the SanDisk monetization could reduce leverage but potentially dilute investor confidence.

Market Positioning and Competitive Landscape

WDC’s strategic focus on AI/data-center HDDs contrasts with broader industry challenges in the consumer storage market. The company’s 215 exabytes shipped in Q1 2026, a 22% YoY increase, reflected strong enterprise demand. Gross margin expansion to 46.1% (up 770 basis points YoY) and $653 million in free cash flow demonstrated operational efficiency. However, the stock’s beta of 1.80 and elevated volatility exposed it to macroeconomic risks, particularly in a high-interest-rate environment. Competitors like Seagate and Samsung remain key players, but WDC’s AI roadmap and buyback program could differentiate it in the mid-to-long term. Analysts projected 2026 EPS of $4.89, up from $2.13 in Q1, assuming continued execution in enterprise storage.

Balancing Short-Term Volatility and Long-Term Growth

The 0.90% drop on 2026-02-27 occurred despite a strong earnings report and positive strategic moves, suggesting that investors priced in some of the recent optimism. The stock’s 50-day moving average of $236.61 and 200-day average of $164.14 indicated a mix of near-term momentum and longer-term trends. While the AI and data-center roadmap provided a clear growth narrative, near-term risks—such as SanDisk monetization and insider sales—introduced uncertainty. Analysts remained cautiously optimistic, with consensus price targets averaging $265.58 and a “Moderate Buy” rating. The key challenge for WDC will be sustaining its earnings momentum while managing shareholder dilution risks and maintaining technological leadership in a rapidly evolving sector.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The Zacks Rank Demystified: Discovering Top Consumer Discretionary Stocks to Buy

Is CLEAR Secure, Inc. (YOU) a Good Investment as a Trending Stock Right Now?

Here’s What You Should Understand About Zscaler, Inc. (ZS) Besides Its Popularity

Here’s What You Should Understand About Intuitive Surgical, Inc. (ISRG) Besides Its Popularity