BioMarin's Q4 Beat: A Tale of Priced-In Roctavian Write-Downs vs. Guidance Reset

The numbers tell a story of two realities colliding. On one side, BioMarinBMRN+1.01% delivered a clear beat on its core profitability metric. The company posted adjusted earnings per share of 46 cents, handily topping the Zacks Consensus Estimate of 25 cents. Revenue also came in stronger, with total revenues of $875 million beating the $830 million consensus. This was driven by a powerful 31% year-over-year surge in Voxzogo sales to $273 million, alongside solid growth across its enzyme therapies.

Yet the headline figure was a stark miss. Reported earnings plunged 50% year over year, a dramatic decline that overshadowed the adjusted beat. The culprit was a $119.2 million inventory write-off charge tied to the company's decision to voluntarily withdraw Roctavian from the market. In other words, the market was expecting this negative catalyst, but the sheer size of the charge still created a jarring gap between the whisper number and the print.

This expectation gap perfectly explains the market's reaction. Despite the better-than-expected adjusted EPS and revenue, shares of BioMarin were down 2.6% in after-hours trading. This is the classic "sell the news" dynamic. The negative Roctavian write-down was already priced in, perhaps even overpriced, as investors braced for the impact. The beat on adjusted earnings was merely a technicality against that heavy cloud. The stock's decline shows that in this game, beating the adjusted number isn't enough if the headline reality is still a major disappointment.

The Roctavian Overhang: A Major Setback Priced In

The Roctavian withdrawal was the dominant negative expectation that shaped the entire earnings narrative. The story began in October 2025, when BioMarin announced it would remove valoctocogene roxaparvovec-rvox (ROCTAVIAN) from its product portfolio. The company had been seeking a buyer, but by February 2026, it had failed to find one. On February 23, it made the formal decision to voluntarily withdraw valoctocogene roxaparvovec-rvox from the market. This sequence of events created a prolonged period of uncertainty, with the market braced for the financial and strategic fallout.

| Total Trade | 20 |

| Winning Trades | 8 |

| Losing Trades | 9 |

| Win Rate | 40% |

| Average Hold Days | 7.05 |

| Max Consecutive Losses | 3 |

| Profit Loss Ratio | 1.3 |

| Avg Win Return | 7.87% |

| Avg Loss Return | 5.5% |

| Max Single Return | 18.12% |

| Max Single Loss Return | 17.67% |

The direct financial impact was immediate and severe. The company booked a $119.2 million inventory write-off charge tied to this withdrawal. This single item was the primary reason for the stark 50% year-over-year decline in reported earnings, creating the expectation gap that overshadowed the adjusted beat. In other words, the market had priced in a negative catalyst, but the sheer size of the charge still delivered a jarring reality check.

Strategically, the exit from the hemophilia gene therapy market introduces a significant near-term revenue gap and a new layer of uncertainty. Roctavian was a key asset in a high-value, niche segment. Its removal means BioMarin must now fill that void with its other pipeline and commercial products, a challenge that analysts are already grappling with. The mixed guidance for the full year further compounds this, as the company resets its forward view without this major revenue stream. This is the core of the "priced-in" dynamic: the market had anticipated a setback, but the scale of the financial hit and the strategic reset were the actual news that moved the stock lower.

Guidance Reset: The Real Catalyst for the Price Target Lift

While the Q4 print was a clash of expectations, the real catalyst for Bernstein's price target increase is a forward-looking bet on operational strength. The firm lifted its target to $94 from $90 and maintained an Outperform rating, explicitly citing operational excellence and the strategic value of the Amicus acquisition. This is a clear signal that the current earnings miss is being discounted. The target hike is based on a belief in what BioMarin can do, not what it just did.

That belief hinges on a major strategic reset, which is now fully priced into the guidance. For the full year 2026, BioMarin is guiding to total revenues of $3.325 billion to $3.425 billion. This range misses the market consensus of $3.507 billion. In other words, the company is formally resetting expectations downward, acknowledging the Roctavian void and the softness in Voxzogo guidance. This is a credibility check: management is being conservative, which may temper near-term hype but sets a lower bar for future beats.

The key driver for that future optimism is the pending Amicus Therapeutics acquisition. Expected to close in the second quarter of 2026, this deal is positioned as a compelling opportunity to reach more patients around the world and further strengthen revenue growth through the next decade. It brings in high-growth, marketed products like Galafold and Pombiliti, adding diversification and a new revenue stream. For Bernstein, this transaction represents the primary upside catalyst that justifies the elevated price target. The market is now being asked to look past the current guidance reset and the Roctavian write-down, betting instead on the operational excellence and portfolio expansion that the Amicus deal promises.

Catalysts and Risks: The Path to $94

The path to Bernstein's $94 target is now defined by a clear sequence of near-term events and a crowded field of skeptical analysts. The primary catalyst is the successful closing of the Amicus Therapeutics acquisition, which management expects to complete in the second quarter of 2026. This deal is the linchpin for the price target hike, promising to accelerate and diversify revenues with high-growth products like Galafold and Pombiliti. Its closure will mark the start of a new chapter, moving the stock's narrative from a guidance reset to a strategic expansion.

Yet the road ahead is fraught with execution risks that could derail this optimism. First is the softness in Voxzogo sales guidance, which Bernstein noted as looking soft on Voxzogo and solid on Enzymes. While Voxzogo's explosive 31% growth in Q4 is a bright spot, any stumble in its momentum would directly pressure the company's top-line trajectory. Second is the integration of Amicus itself. Merging two rare-disease focused companies requires flawless execution to realize the promised synergies and accretion to earnings. Any misstep here could turn a strategic opportunity into a costly distraction.

Most pressing is the continued financial and strategic pressure from the Roctavian exit. The $119.2 million write-down was a major hit, and the voluntary withdrawal from the hemophilia gene therapy market leaves a void that must be filled. The company's own FY2026 sales guidance of $3.325 billion to $3.425 billion already reflects a reset, missing the market consensus. This sets a low bar, but it also means there is little room for error. The stock must now deliver on the Amicus promise while navigating this legacy overhang.

This creates a crowded and uncertain consensus. While Bernstein is raising its target, other major firms have been cutting theirs. Piper Sandler slashed its target from $122 to $84, and Leerink Partners downgraded the stock from Outperform to Market Perform, cutting its price target to $60. This divergence in analyst sentiment highlights the tension between the long-term strategic bet on Amicus and the near-term operational challenges. For the stock to climb toward $94, it will need to prove that the operational excellence Bernstein cites can overcome these near-term headwinds and deliver on the Amicus promise. The market is being asked to look past the current fog of uncertainty, but the catalysts and risks are now laid bare.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

又一美联储理事呼吁:谨慎对待进一步降息!

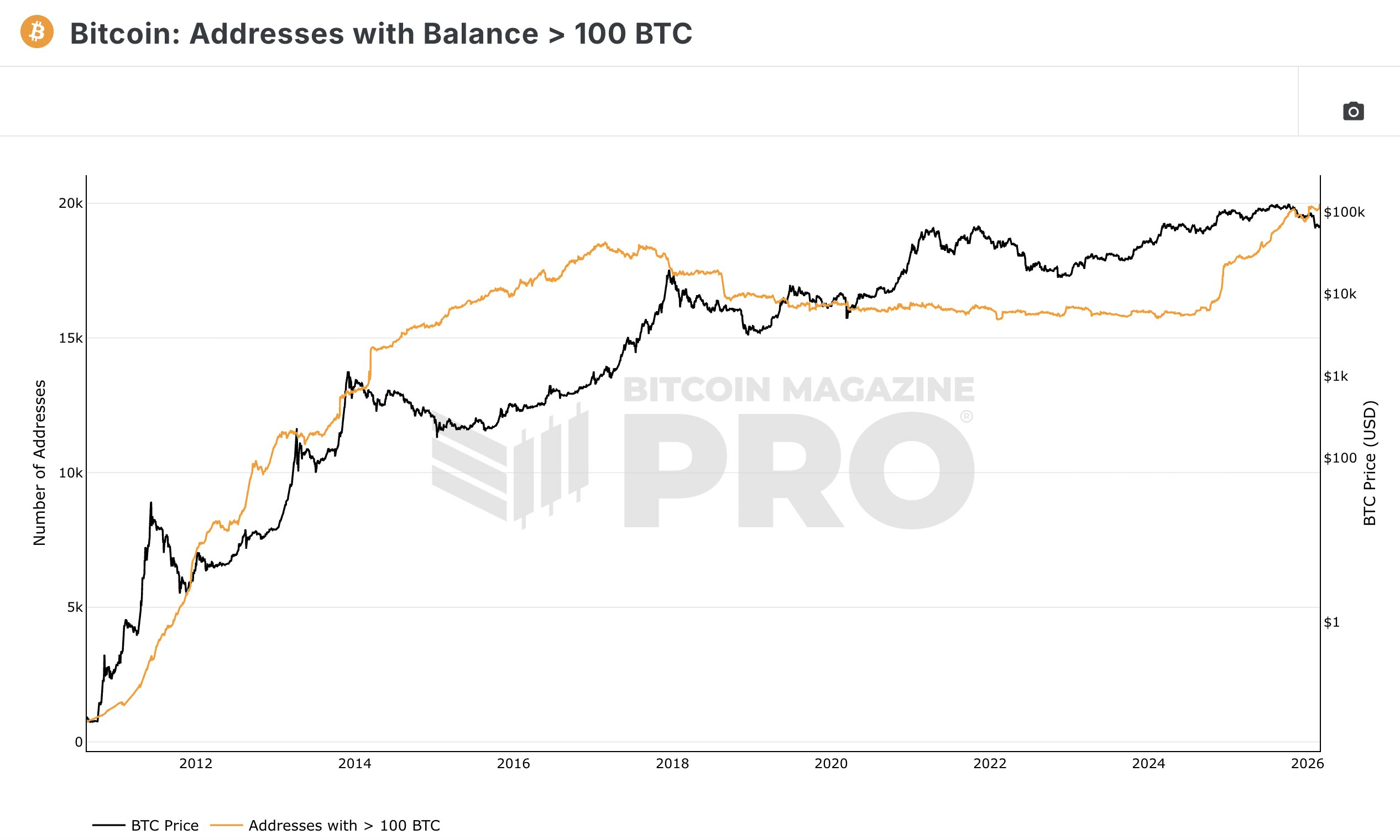

Bitcoin whale addresses holding 100 BTC hit ATH – Strategic play for H2 rally?

Ethereum smart accounts are finally coming 'within a year' — Vitalik Buterin