MGM Resorts International (MGM): A Bull Case Theory

We came across a bullish thesis on MGM Resorts International on The Rational Investor’s Substack by Maxx Waring. In this article, we will summarize the bulls’ thesis on MGM. MGM Resorts International's share was trading at $36.36 as of February 11th. MGM’s trailing and forward P/E were 49.16 and 17.83 respectively according to Yahoo Finance.

MGM Resorts International, through its subsidiaries, operates as a gaming and entertainment company in the United States, China, and internationally. MGM presents a compelling investment opportunity driven by multiple near- and long-term catalysts. Despite a temporary slowdown in Las Vegas tourism and room remodels at the MGM Grand in 2025, the company is executing a strategic plan that positions it for substantial upside.

MGM is aggressively buying back 7-8% of its shares annually, funded by a business generating a 14.2% Owner Earnings yield. BetMGM, the company’s 50/50 digital sports betting and iGaming joint venture, turned profitable in 2025, distributing $100 million back to MGM and setting the stage for $125-200 million in cash distributions in 2026, providing a direct boost to buybacks and Owner Earnings.

Additional near-term catalysts include the Northfield Park sale, closing in the first half of 2026, which will inject $420 million of proceeds for share repurchases, and the stabilization of Las Vegas Strip operations as MGM Grand’s remodels are completed, conventions return, and RevPAR growth resumes. MGM China’s ongoing recovery continues to provide $200-300 million in annual dividends, further funding capital returns. The company is also executing the Osaka integrated resort in Japan, scheduled to open in 2030.

MGM’s 42.5% stake in Osaka represents a future $350-450 million annual Owner Earnings contribution, supported by monopoly positioning and a lower tax rate relative to Macau. GAAP net income is expected to swing from loss to profit in 2026 as one-time charges abate, attracting investor attention.

At the current share price, MGM trades at roughly 7x Owner Earnings with significant buyback acceleration underway. With stabilized core operations, growing digital cash flows, and Osaka’s long-term potential, MGM Resorts offers an attractive risk/reward profile with a bullish target of Buy up to $46 per share.

MGM’s stock price has appreciated by approximately 38.25% since our coverage. Maxx Waring shares a similar bullish view but emphasizes near-term catalysts like BetMGM profitability, Northfield Park sale, Las Vegas Strip stabilization, and Osaka, projecting a Buy up to $46 per share.Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

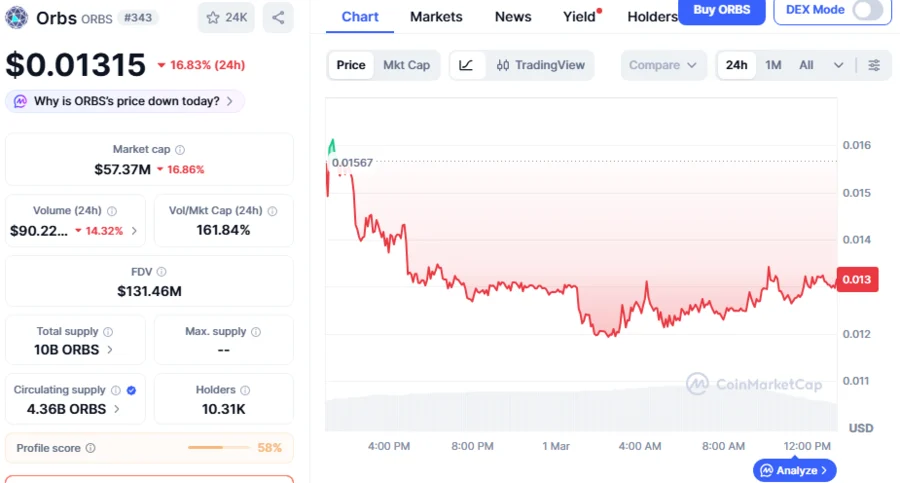

ORBS Price Erupts 36.9% As Analyst Identifies Large Bullish Candle That Sets To Trigger Further Market Rally

Uniswap Price Eyes $4.60 as Fee Burn Vote Advances

移动游戏、广告营收大增,B站Q3营收同比增长26%,经调净利润首次转正

Trending news

MoreORBS Price Erupts 36.9% As Analyst Identifies Large Bullish Candle That Sets To Trigger Further Market Rally

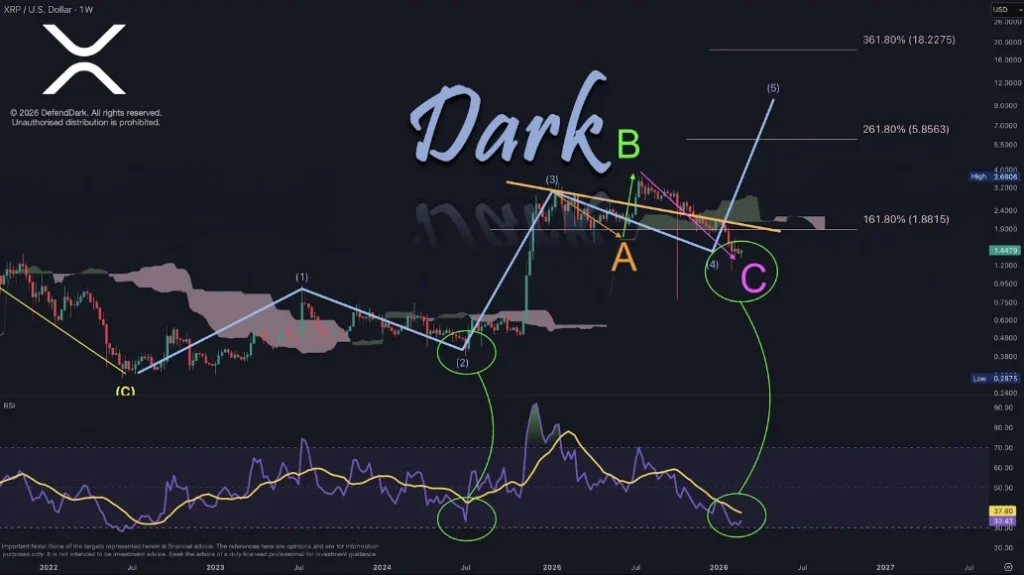

XRP Price News 2026: Degens Favor DeepSnitch AI as Top Pick for 100X as Power Protocol RSI Hints at Price Correction, Chainalysis Reports 50% Spike in Ransomware Incidents but Ransom Payouts Decline