Warrior Met Coal, Inc. (HCC): A Bull Case Theory

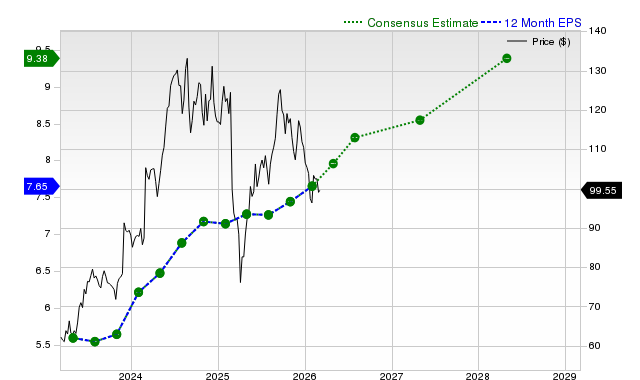

We came across a on Warrior Met Coal, Inc. on Common Sense Capital’s Substack. In this article, we will summarize the bulls’ thesis on HCC. Warrior Met Coal, Inc.'s share was trading at $87.05 as of February 23rd. HCC’s trailing and forward P/E were 85.01 and 16.23 respectively according to Yahoo Finance.

Warrior Met Coal ($HCC) is transitioning from a development-focused miner to a major metallurgical coal producer as the Blue Creek mine begins its ramp-up, marking a structural inflection point for the company. The mine, one of North America’s largest untouched high-volatile “A” metallurgical coal reserves, is expected to increase total production capacity by roughly 75%, positioning Warrior as one of the lowest-cost, high-quality coal producers globally. The company’s legacy Mines 4 and 7 continue to generate strong cash flow, funding the Blue Creek expansion while maintaining a lean cost structure.

Warrior benefits from a logistics moat through direct access to the Port of Mobile, enabling efficient exports to Europe, South America, and increasingly Asia, where India’s rapid steel production growth creates a structurally non-substitutable demand for premium coking coal. The 100%+ rally over the past year largely reflects the market pricing in the production ramp and operational excellence; however, upside remains significant if metallurgical coal prices rise beyond current levels due to the company’s high operating leverage, where incremental price gains flow almost entirely to the bottom line.

Blue Creek’s completion shifts Warrior from high capital expenditures to a free cash flow generation phase, with sustaining capital expected to normalize around $140–150 million annually, supporting shareholder returns through dividends and buybacks. At the current share price near $92, the stock appears fairly valued for its production and commodity risk, but any meaningful pullback would provide a compelling entry point, offering margin of safety and an attractive risk/reward profile for investors positioned to benefit from the cyclical upside in global metallurgical coal prices.

Previously, we covered a

Warrior Met Coal, Inc. is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Royal Caribbean Cruises Ltd. (RCL) Is Gaining Attention: Key Information to Consider Before Investing

Realty Income Corporation (O) is Drawing Interest from Investors: What You Need to Be Aware Of

NVIDIA Price Rebounds Ahead of GPU Technology Conference With $225 in Sight

NetApp, Inc. (NTAP) is Drawing Interest from Investors: Key Information You Need to Know