Graphic Packaging Holding Company (GPK): A Bull Case Theory

We came across a bullish thesis on Graphic Packaging Holding Company on Chop Wood, Carry Water’s Substack by Alexandru Dragut. In this article, we will summarize the bulls’ thesis on GPK. Graphic Packaging Holding Company's share was trading at $12.10 as of February 23rd. GPK’s trailing and forward P/E were 10.99 and 8.85 respectively according to Yahoo Finance.

Graphic Packaging Holding Co. (GPK) is a leading provider of paper-based consumer packaging, producing the boxes, cups, trays, and cartons found in everyday products from cereal to coffee and quick-service meals. Despite recent market skepticism, GPK’s underlying business generates approximately $700 million in annual owner earnings, reflecting a 19% yield on current market capitalization.

The apparent weakness is largely due to three temporary headwinds: the ramp-up of the company’s largest-ever capital investment at the Waco, Texas facility, unusual pricing pressure from overcapacity in bleached board competitors, and broader softness in consumer packaged goods (CPG) volumes. These factors mask the resilience of GPK’s core business, which serves diversified, high-quality customers, including General Mills, Coca-Cola, Procter & Gamble, and leading quick-service restaurants, with no single customer representing more than 10% of sales.

GPK’s North American folding carton operations command roughly 40% market share, while European operations are expanding via the AR Packaging acquisition. The company’s vertical integration—internal production of recycled paperboard—and modernized facilities like Kalamazoo K2 and Waco provide a durable cost advantage, while innovation initiatives such as KeelClip™, Boardio™, and PaperSeal™ position GPK to capture a $15 billion plastic-to-fiber conversion opportunity. Multi-year supply contracts, operational integration, and proprietary formats create a contract-cycle-bound moat. Free cash flow is set to normalize in 2026 at $700–800 million as CapEx drops post-Waco, enabling debt reduction and potential value compounding.

While risks exist, including execution by the new CEO, ongoing bleached board overcapacity, and potential CPG volume softness, GPK’s diversified customer base, low cyclicality, and strategic investments offer a compelling margin of safety. At current prices, the market appears to underappreciate the company’s normalized earnings and cash flow trajectory, creating a potential opportunity for significant upside.

Previously, we covered a

Graphic Packaging Holding Company is not on our list of the

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

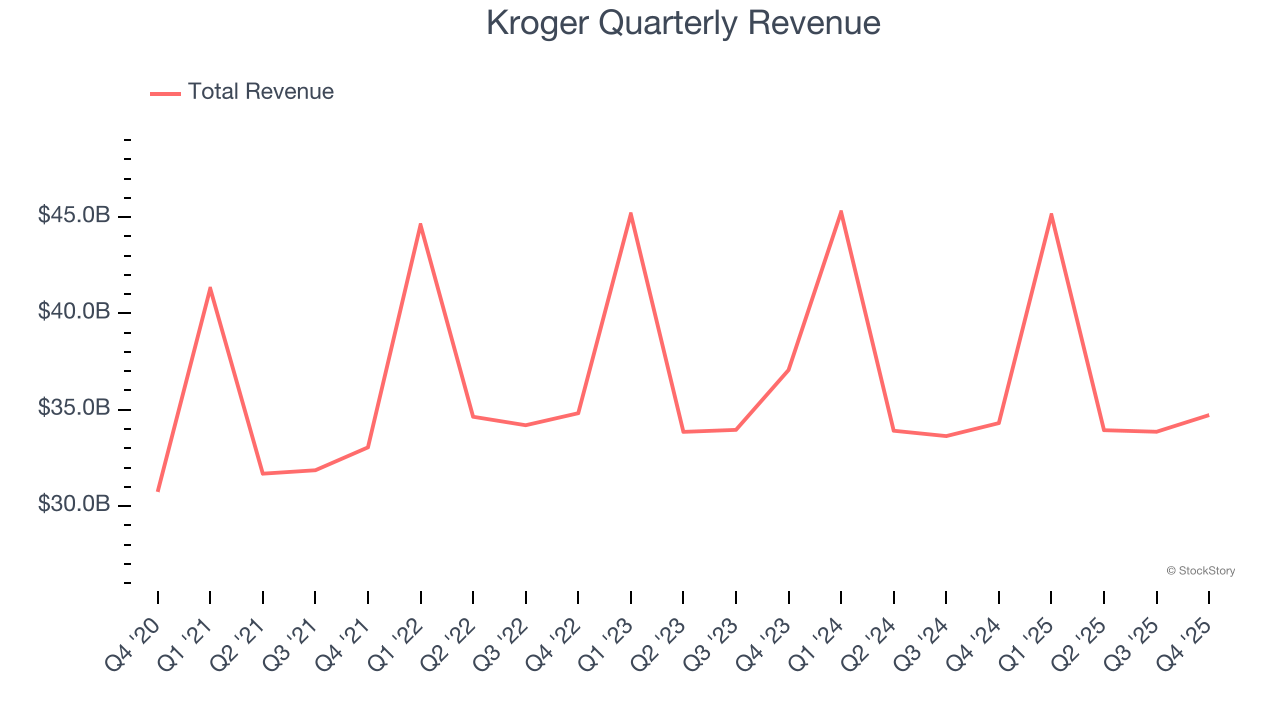

Kroger (NYSE:KR) Reports Sales Below Analyst Estimates In Q4 CY2025 Earnings

Why Is IREN Stock Falling Thursday?

WTI finds it difficult to remain above $76 amid optimism for easing tensions in the Middle East

Job layoff announcements saw a decrease last month, offering a welcome relief