What to Expect in the Week Ahead (Nonfarm Payrolls, and Earnings from CrowdStrike, Broadcom and Marvell)

A widely circulated sell-side note triggered a selloff in numerous AI-linked stocks last week, driven by fears of impending large-scale layoffs, which in turn fueled a rally in bonds.

The February payrolls report is likely to show subdued headline job growth—largely attributable to disruptive cold weather in late January and early February rather than underlying labor-market weakness.

Persistent US tariff uncertainty looms over reports from retail giants which will show slowing profit growth and tighter margins.

Key earnings: CRWD, AVGO, COST and MRVL, etc.

Key earnings: CRWD, AVGO, COST and MRVL, etc.

📆 Earnings & Economic Calendar

Week overview

Over the coming week, the market will continue to focus on employment data to gauge both the impact of AI revolution on the job market and the implications of labor-market conditions for Fed interest-rate decisions. Earnings reports from major retailers and semiconductor companies are also due to roll out.

Monday (Mar. 2)

Macro: ISM Manufacturing

The ISM Manufacturing PMI is expected to drop to 51.2 in February—still signaling expansion, though at a noticeably slower pace than January's reading, which marked the strongest growth since August 2022.

Key earnings: $AST SpaceMobile (ASTS.US)$, $Credo Technology (CRDO.US)$, $MongoDB (MDB.US)$

Tuesday (Mar. 4)

Key earnings: $CrowdStrike (CRWD.US)$, $Target (TGT.US)$ and $Best Buy (BBY.US)$

$Target (TGT.US)$ is expected to report another decline in same-store sales for the fourth consecutive quarter, even as the company continues efforts to boost customer traffic. Citi analysts warn that another retail giant $Best Buy (BBY.US)$ could miss consensus earnings-per-share estimates due to persistently soft demand and continued market share erosion, while a shortage of memory chips may further pressure sales and inventory levels in the coming months.

Wednesday (Mar. 4)

Macro: Services PM

The services sector showed signs of cooling in February. While PMIs are expected to confirm continued expansion, the pace of growth likely slowed compared to January.

Key earnings: $Broadcom (AVGO.US)$, $Rigetti Computing (RGTI.US)$

Citi expects $Broadcom (AVGO.US)$ to deliver a modest EPS beat on stronger margins, with sales roughly in line with consensus. Semiconductor solutions revenue is projected to surge nearly 50%—a record high—driven by rising AI-related corporate spending.

Thursday (Mar. 5)

Macro: Initial Jobless Claims

Key earnings: $Costco (COST.US)$, $Marvell Technology (MRVL.US)$

$Marvell Technology (MRVL.US)$ carries a Hold rating ahead of Q4 2026 earnings, as explosive prior growth moderates. Trailing YoY revenue growth of ~45% still leads peers, but recent quarters point to a sustainable 20–35% range. Guidance signals 21% YoY growth, in line with consensus, and the company has a solid history of beating estimates. Key risks remain customer concentration, though stabilizing growth and margin gains could create a post-earnings buying opportunity.

Friday (Mar. 6)

Macro: Nonfarm Payrolls and Unemployment Rate

February payrolls are expected to fall by 30,000—a marked slowdown from January’s unexpectedly robust figure. The deceleration largely stems from the late-January/early-February cold snap rather than any fundamental softening in hiring trends.

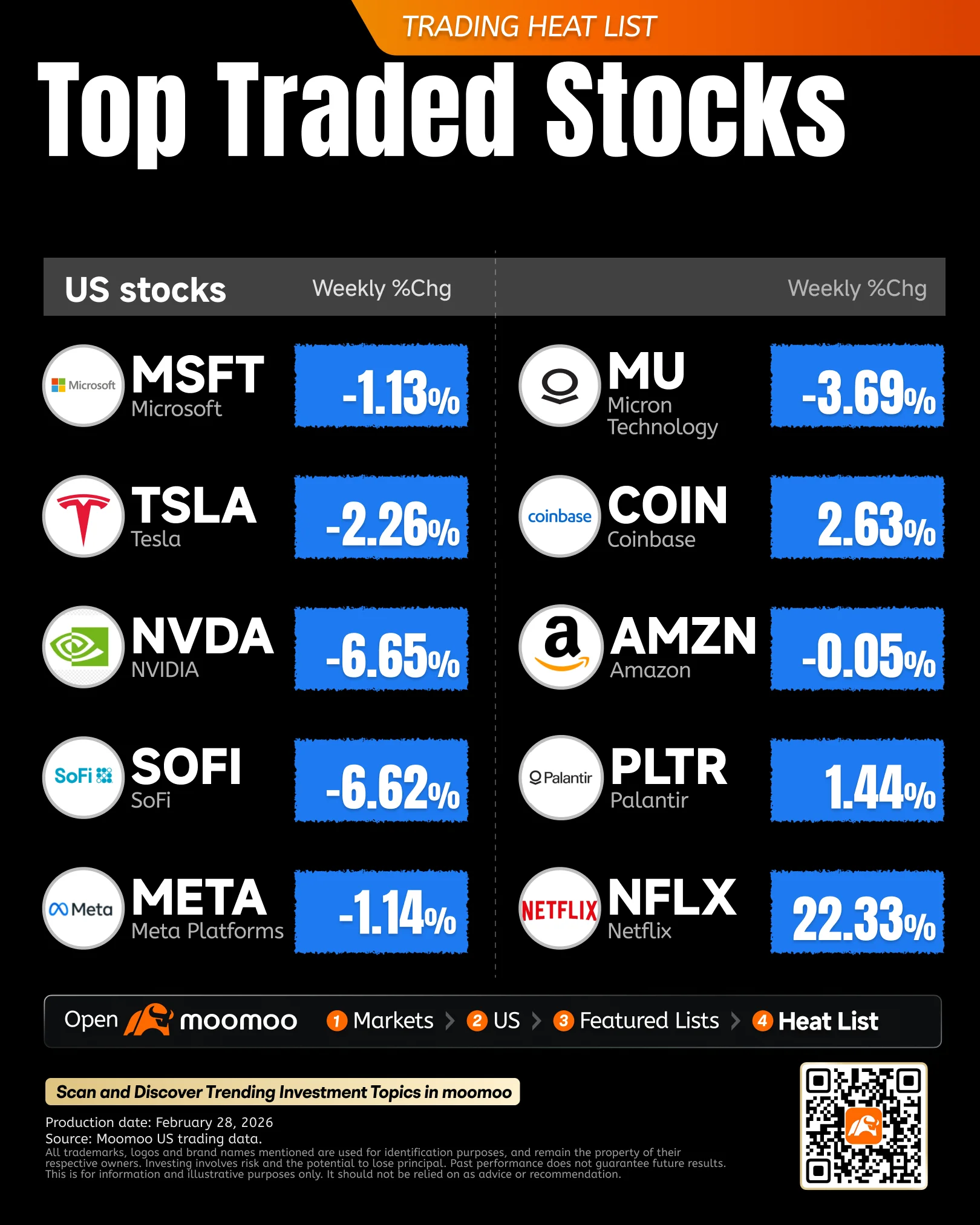

🎩Heat List

Last week, A Citrini Research gave a 'report from 2028' painting a grim picture: widespread job losses for white-collar workers as AI agents take over human tasks en masse —— AI fear still remain. The "Nvidia Earnings Week" dominated the narrative, market slid as investors from Wall Street concerns about Nvidia's profit sustainability despite earnings beat.

AI chip giant $NVIDIA (NVDA.US)$ released its highly anticipated FY26Q4 earnings, delivering financial metrics that crushed expectations across the board. Management provided guidance that soared past market consensus, yet the stock dipped as investors were under concerns about "AI bubble".

Software stocks and megacap tech names, including $NVIDIA (NVDA.US)$, kept sliding, compounding their steep losses from the past month. This time, semiconductor stocks—especially recently red-hot memory plays like $Micron Technology (MU.US)$, which had surged while software names tanked—also came under heavy selling pressure.

$Netflix (NFLX.US)$ shares soared after the streaming giant declined to match an improved bid from $Paramount Skydance (PSKY.US)$ for $Warner Bros Discovery (WBD.US)$. While Paramount’s streaming operations are much smaller than Netflix’s, the deal would combine two major legacy film and television studios under a single owner, plus a portfolio of cable networks.

Megacap tech stocks are under pressure as investors grow skeptical about the enormous spending on AI infrastructure, questioning whether the potential returns can justify the huge costs. Recent earnings from $Microsoft (MSFT.US)$ and $Amazon (AMZN.US)$ triggered negative market reactions, and even Nvidia’s blockbuster results earlier this week failed to reverse the broader selloff.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Crypto Market Drops Further as Extreme Fear Persists

Arvinas, Inc. (ARVN) Makes Significant Progress on Oncology and Neurology Trials

Schrodinger, Inc. (SDGR) Transition to Licensing Model Triggers Robust Revenue Growth