美股收盘 | 三大指数集体收跌;新能源车股重��挫,Rivian大跌超14%,特斯拉跌近6%;热门中概股普跌,极氪跌超23%

美联储票委理事库格勒表示,必须同时关注就业、通胀目标。如果通胀停滞或上升,暂停降息是合适的。如果就业市场突然放缓,逐步降息是合适的。2024年FOMC票委、美国里士满联储主席巴尔金称,缩表(QT)意在让资产负债表正常化,而不是紧缩。

美联储票委理事库格勒表示,必须同时关注就业、通胀目标。如果通胀停滞或上升,暂停降息是合适的。如果就业市场突然放缓,逐步降息是合适的。2024年FOMC票委、美国里士满联储主席巴尔金称,缩表(QT)意在让资产负债表正常化,而不是紧缩。  鲍威尔的言论使降息预期明显降低,目前12月降息的可能性不到61%

鲍威尔的言论使降息预期明显降低,目前12月降息的可能性不到61%

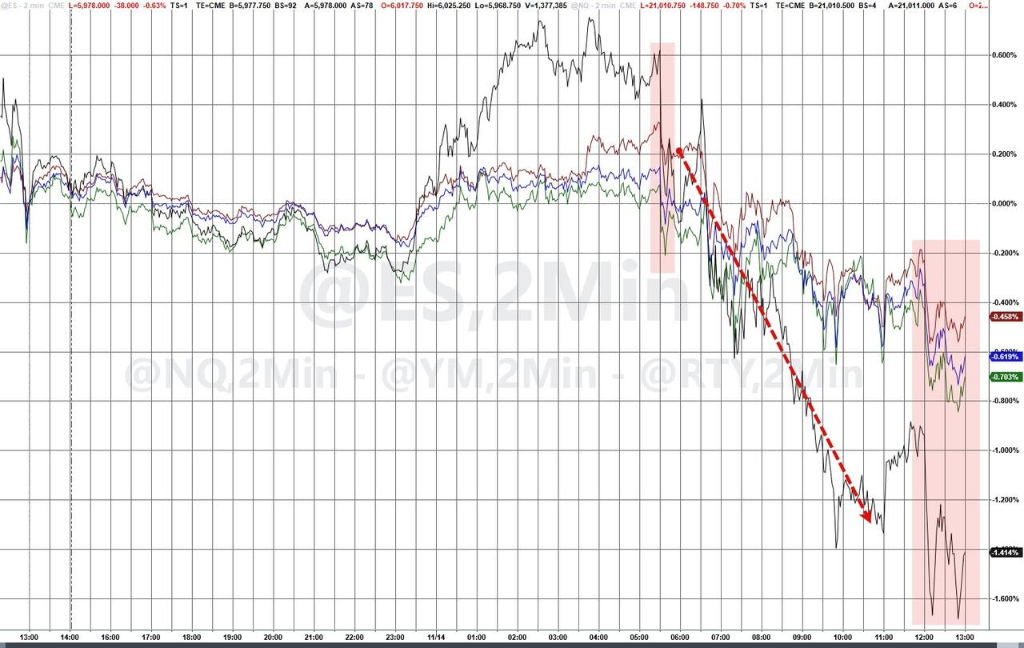

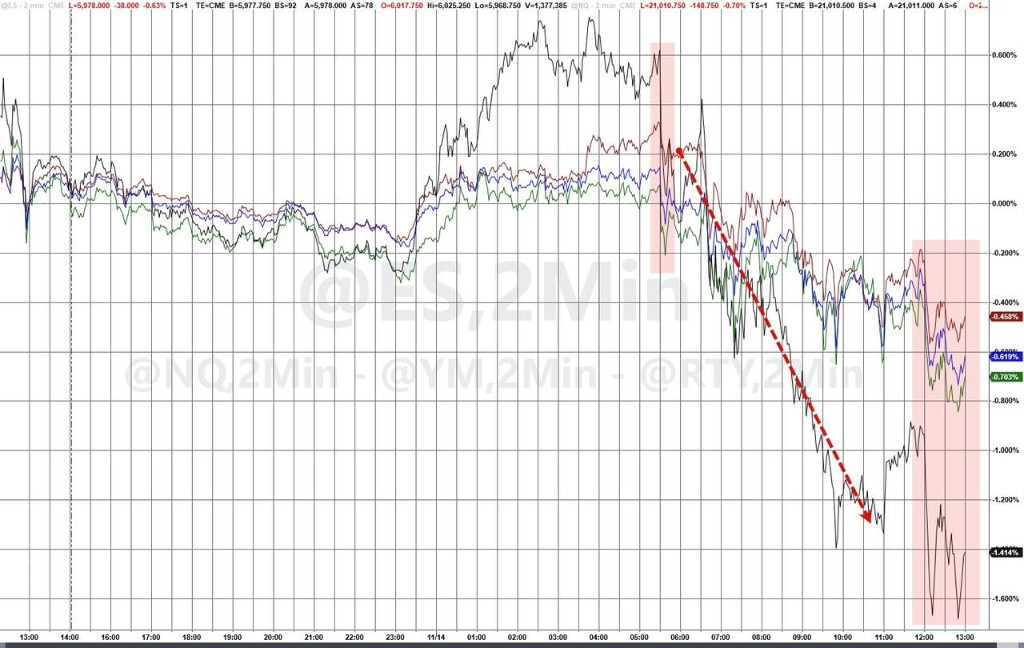

鲍威尔言论加剧股市跌势

鲍威尔言论加剧股市跌势

In October, US PPI accelerated rebound, first-time jobless claims at a nearly six-month low, traders reduced rate cut bets, small cap stocks and Chinese concept indexes fell more than 1%, nvidia rose nearly 2% before turning down, Tesla dropped nearly 6%, zeekr plunged over 23%, jd.com dropped over 6%, Bilibili dropped more than 12%, netease rose more than 10%. The US dollar rose for the fifth consecutive time, the euro hit a one-year low, the Japanese yen fell below 156, offshore RMB briefly fell 200 points to temporarily breach 7.26 yuan. Gold oscillated lower and once fell by 1.4%, US bond yields turned higher, bitcoin fell below $0.088 million, and oil prices rose.

U.S. Treasuries, gold, silver, copper, U.S. stocks, and non-U.S. currencies were under pressure throughout the day. On one hand, according to CCTV news, the U.S. Republican Party won control of the House of Representatives. On the other hand, Powell stated that the Federal Reserve does not need to rush to cut interest rates, leading the market to reduce bets on a Fed rate cut, with the probability of a 25 basis points cut in December being slashed from 82.5% to 60.6%. The strong dollar impacts everything, with the dollar index rising above 107 during the session, setting a new high for over a year. The yen fell below the 156 mark, and the euro broke below 1.05 for the first time since October 2023, while spot gold once dipped to 2530 dollars.

In terms of economic data, the U.S. PPI for October rebounded across the board, with a year-on-year increase of 2.4%, exceeding expectations. The stickiness in the service industry has intensified, with the core PPI excluding food and energy rising 0.3% month-on-month in October, faster than projected. Coupled with the accelerating year-on-year CPI growth released on Wednesday, it shows that the battle against inflation by the Federal Reserve is not yet won. Last week, the number of first-time applications for unemployment benefits in the U.S. fell to 0.217 million, the lowest level since May. According to research reports from China International Capital Corporation, attention should still be paid to the last non-farm and inflation reports before the December meeting. If data exceeds expectations, the Federal Reserve may maintain flexibility not to cut rates in December.

Federal Reserve voting member Governor Cook stated that both employment and inflation targets must be monitored simultaneously. If inflation stagnates or rises, it is appropriate to pause rate cuts. If the job market suddenly slows, gradual rate cuts would be appropriate. 2024 FOMC voting member and President of the Federal Reserve Bank of Richmond, Barkin, stated that balance sheet normalization through quantitative tightening (QT) is aimed at normalizing the balance sheet, not tightening.

Federal Reserve voting member Governor Cook stated that both employment and inflation targets must be monitored simultaneously. If inflation stagnates or rises, it is appropriate to pause rate cuts. If the job market suddenly slows, gradual rate cuts would be appropriate. 2024 FOMC voting member and President of the Federal Reserve Bank of Richmond, Barkin, stated that balance sheet normalization through quantitative tightening (QT) is aimed at normalizing the balance sheet, not tightening.

Internationally, concerns about the economic outlook for the Eurozone increased due to potential tariff measures that the U.S. may implement. Traders raised their bets on an ECB rate cut in 2025, predicting that the European Central Bank will cut rates by a cumulative 146 basis points by December 2025, the highest since the end of October. The yield on German two-year government bonds fell by 6 basis points to 2.10% at one point. Econostream Media reported that ECB officials discussed the possibility of consecutive rate cuts. Additionally, the Bank of Mexico cut rates by 25 basis points to 10.25%, in line with expectations.

Powell's comments have significantly reduced rate cut expectations, with the possibility of a cut in December currently being less than 61%.

Powell's comments have significantly reduced rate cut expectations, with the possibility of a cut in December currently being less than 61%.

Federal Reserve Chairman Powell stated that the Fed does not need to rush to cut rates, which caused U.S. stock indices to extend their declines and close near the day's lows, with the Dow falling more than 250 points at one point. All sectors except for energy and technology declined, and Trump's trade is continuing to wane.

All three major indices of the US stock market fell. The S&P 500 index closed down 36.21 points, a decrease of 0.60%, at 5949.17 points. The Dow Jones, closely related to the economic cycle, closed down 207.33 points, a decrease of 0.47%, at 43750.86 points. The technology-heavy Nasdaq closed down 123.07 points, a decrease of 0.64%, at 19107.65 points. The Nasdaq 100 index closed down 0.66%. The Nasdaq Technology Market Cap Weighted Index (NDXTMC), which measures the performance of Nasdaq 100 technology component stocks, closed down 0.27%. The Russell 2000 small-cap index, which is more sensitive to the economic cycle, closed down 1.37%. The fear index VIX closed up 2.14%, at 14.32.

Powell's remarks exacerbated the stock market's decline.

Powell's remarks exacerbated the stock market's decline.

Most US sector ETFs fell, with news of Trump's health secretary nominee causing a decline of about 2.6% in the biotechnology ETF. The medical care ETF, consumer discretionary ETF, and internet stocks index ETF fell by up to about 1.6%, the banking sector ETF fell by over 0.8%, the technology sector ETF fell by over 0.3%, while the semiconductor ETF rose by over 0.2%, and the energy sector ETF increased by about 0.4%.

Most of the 11 sectors of the S&P 500 index fell. The industrial sector fell by 1.69%, the consumer discretionary sector fell by 1.54%, the medical care sector fell by 1.54%, the real estate sector fell by 0.93%, the materials sector fell by 0.7%, the telecommunications sector fell by 0.66%, the utilities sector fell by 0.38%, the financial sector fell by 0.26%, the consumer staples sector fell by 0.22%, the information technology/technology sector rose by 0.05%, and the energy sector rose by 0.14%.

"The tech seven sisters" were mixed. Google A closed down 1.84%, Tesla closed down 5.77%, Amazon closed down 1.22%, "metaverse" Meta closed down 0.49%, fined nearly 0.8 billion euros for violating EU antitrust regulations, and Meta will appeal the decision of the EU Commission. Nvidia closed up 0.33%, having initially risen nearly 2% before turning down. Apple closed up 1.38%, and Microsoft closed up 0.4%.

Most chip stocks rose. The Philadelphia Semiconductor Index rose 1.4% to lead but closed down 0.03%. The industry ETF SOXX closed down 0.06%. The Nvidia double leveraged ETF rose 0.43%. ASML ADR rose 5.7% before closing up 2.9%, with strong AI demand, and the company expects an average sales growth rate of 8% to 14% over the next five years. Intel closed up 0.44%. Arm Holdings closed up 0.93%. Taiwan Semiconductor ADR closed up 0.99%, Qualcomm closed up 2.21%, KLA Corp closed up 0.07%, AMD closed down 0.33%, Micron Technology closed down 0.74%, On Semiconductor closed down 2.15%, Broadcom closed down 1.84%, and Wolfspeed closed down 5.82%.

AI concept stocks collectively fell. Super Micro Computer closed down 11.41%, Serve Robotics closed down 6.1%, Dell Technologies closed down 0.07%, BullFrog AI closed down 6.2%, C3.ai closed down 3.19%, Oracle closed down 1.36%, CrowdStrike closed down 1.01%, Palantir closed down 2.5%, Snowflake closed down 1.12%, while AI voice company SoundHound AI, which is partially owned by Nvidia, closed up 5.74%, and BigBear.ai closed up 1.17%.

China concept stocks experienced a general decline. The Nasdaq Golden Dragon China Index fell by 1.81%, closing at 6449.21 points. Among ETFs, the FTSE China 3X Long ETF (YINN) declined by 3.16%, the China Technology Index ETF (CQQQ) fell by 2.60%, and the China Concept Internet Index ETF (KWEB) dropped by 1.51%. The FTSE A50 futures also closed lower by 0.36% during the overnight session, settling at 13478.000 points.

Among popular China concept stocks, Zeekr dropped by 23.68%, while Volvo sold its 30% stake in Lynk & Co to Zeekr for a transaction value of 5.4 billion yuan. Bilibili fell by 12.8%, with significant increases in mobile game and advertising revenue, showing a 26% year-on-year growth in Q3 revenue, marking the first positive adjusted net profit. Fangdd Network declined by 10.13%. JD.com fell by 6.56%, with Q3 revenue exceeding expectations with a 5% year-on-year growth, net profit surged by 48%, and active users grew by double digits for three consecutive quarters. Miniso dropped by 6.35%, XPeng Motors fell by 5.39%, NIO declined by 3.9%, Trip.com fell by 3.46%, Alibaba dropped by 1.54%, PDD Holdings declined by 0.95%, Li Auto fell by 0.54%, and Baidu dropped by 0.48%. Netease rose by 10.41%, affected by a decline in gaming business, while Q3 revenue and net profit both shrank, but the performance of PC games was bright, achieving double-digit growth in both current and compared revenue.

Bitcoin futures fell by over 1.9%, and most cryptos concept stocks declined. The crypto 'meme stock' Ideanomics fell by 7.69%, Riot Platforms dropped by 6.35%, the crypto exchange giant Coinbase declined by 2.07%, and MSTR, a 'big holder of bitcoin,' fell by 0.22%. Mercurity Fintech ADR dropped by 34.5%.

Reports indicate that the Trump team plans to cancel the $7,500 electric vehicle tax credit, leading to a sharp decline in electric vehicle concept stocks. Nikola fell by 22.76%, Workhorse dropped by 14.49%, Rivian, a 'Tesla rival,' declined by 14.3%, WeRide ADR dropped by 17.07%, and Jia Yueting’s FFIE fell by 2.82%.

Other key individual stocks: (1) Trump Media Tech (DJT) fell by 6.71%. (2) Disney rose by 6.23%, hitting nearly 12% growth at one point during the trading session, with adjusted EPS in Q4 exceeding expectations. (3) The fashion luxury goods group capri holdings rose by 4.43%, and Tapestry rose by 12.8%, prior to which capri holdings announced the termination of its merger with Tapestry. (4) Cisco fell by 2.13%, with last quarter's revenue declining by 6%, still better than expected, but the upward guidance was somewhat lacking. (5) The 13F report shows that Berkshire Hathaway reduced its holdings in Apple, Bank of America, Utah Beauty, Charter Communications, and other stocks in Q3. The shareholding ratio for Bank of America at the end of Q3 was 10.4%. Major holdings include Apple, American Express, Bank of America, Coca-Cola, and Chevron. (6) 'Affordable weight loss drug supplier' Hims & Hers Health (HIMS) fell by 24.46%, marking the worst single-day performance since the US IPO. Amazon launched electronic health products targeting Prime members, and analysts stated that Hims faces a 'severe threat.'

European stock markets closed up over 1%, ending two consecutive days of decline, with both French and German indices rising over 1%. The eurozone blue chip Stoxx 50 index briefly rose by 2%, and the struggling UK luxury goods company Burberry rose by 18.7% after announcing a reform plan.

The pan-European STOXX 600 index closed up 1.08%. The eurozone STOXX 50 index closed up 1.97%. The FTSE pan-European superior 300 index closed up 1.04%.

Technology stocks rose by 3.13%, leading the rally, while automotive and oil and gas stocks both rose by about 1.7%. Siemens in the European market rose by 4.91%, reaching a record high as the company’s Q4 revenue exceeded expectations.

Germany's DAX 30 index closed up 1.37%. France's CAC 40 index closed up 1.32%. The Netherlands AEX index closed up 1.33%. Italy's FTSE MIB index closed up 1.93%. The UK FTSE 100 index closed up 0.51%. Spain's IBEX 35 index closed up 1.29%.

The investment return rate of European stocks lags behind that of US stocks at the largest margin in nearly 30 years. After Trump's election, global funds preferred to invest in US assets, which may further exacerbate the lagging situation of European stocks. So far this year, the S&P 500 index has risen about 25%, reaching a historical high, while the European Stoxx 600 index has only risen about 5%.

Powell has struck down traders' expectations for rate cuts by the Federal Reserve, causing the two-year US Treasury yield, more sensitive to interest rates, to rise towards the close, nearing a four-month high. The money market has raised expectations for a faster and larger rate cut by the European Central Bank, leading to a steepening of the German bond bull market:

US bonds: At the close, the yield on the benchmark 10-year US Treasury fell by 1.58 basis points to 4.4354%, trading within a range of 4.4808%-4.3863% during the day. At 09:02 (UTC+8), it refreshed the day's high, with a rebound occurring when the US weekly employment data and PPI indicators were released at 21:30 (UTC+8). At 01:28 (UTC+8), it refreshed the day's low after Federal Reserve Chair Powell's speech at 04:00 (UTC+8) dashed market rate cut expectations, causing yields to briefly rise back to flat. The yield on the two-year US Treasury rose by 5.28 basis points to 4.3448%, with a trading range of 4.2396%-4.3638% during the day, as Powell's speech indicated a hawkish stance, raising yields sharply from flat and refreshing the day's high.

HSBC has raised its forecast for the yield on 10-year US Treasury Bonds at the end of 2025 to 3.5%, up from the previous forecast of 3%.

European bonds: At the close, the yield on the 10-year German bond fell by 4.9 basis points to 2.341%. The yield on the two-year German bond fell by 6.3 basis points to 2.102%. The yield on the 10-year UK bond fell by 3.7 basis points. The yield on the two-year UK bond fell by 6.2 basis points. The yield on the 10-year French bond fell by 6.8 basis points. The yield on the 10-year Italian bond fell by 8.5 basis points.

The usd rose 0.4% on the day of Powell's speech, standing above 107 during the session, marking a five-day winning streak and a new high not seen in over a year. The yen fell below 156 against the dollar for the first time since July, while the euro dropped below 1.05 against the dollar during the session for the first time since October 2023. The offshore yuan fell nearly a hundred points, and during the European stock market period, it temporarily dropped 200 points to slightly breach 7.26 yuan. Bitcoin futures fell more than 1.9%.

Usd: The usd index DXY ended up 0.39%, at 106.901 points, with significant fluctuations during the day. At 19:14 (UTC+8), it rose to 107.064 points, crossing the 107-point mark for the first time since November 1, 2023 (the daily peak was 107.113 points), then fell to a daily low of 106.382 points at 00:26 (UTC+8) after Federal Reserve Chairman Powell's speech, significantly expanding its gains. The Bloomberg usd index rose 0.27%, closing at 1288.18 points, with an intraday trading range of 1283.52-1290.02 points.

Non-us currencies: The euro fell 0.32% against the usd to 1.0530, breaking below the 1.05 mark for the first time since October 13, 2023. The british pound fell 0.30% against the usd to a four-month low, while the usd rose 0.52% against the swiss franc. Among commodity currencies, the aud fell 0.55% against the usd to a three-month low, the nz dollar fell 0.52% against the usd, and the usd rose 0.43% against the cad. The swedish krona fell 0.11% against the usd, and the norwegian krone fell 0.12% against the usd.

Yen: The yen fell 0.53% against the usd to 156.28 yen, with an intraday trading range of 155.35-156.42 yen. According to Bloomberg, the Japanese government is enhancing the details of the economic stimulus plan, proposing to issue a 0.03 million yen subsidy to low-income households.

Offshore yuan (CNH): The offshore yuan fell 101 points against the usd, closing at 7.2538 yuan, with overall trading throughout the day in the range of 7.2364-7.2665 yuan.

Cryptos: The largest cryptocurrency by market cap, bitcoin futures, closed down 1.92% at 88,520.00 usd. The second-largest, ether futures, closed down 1.89% at 3,136.00 usd.

International oil prices rose by about 0.4%, with US oil briefly increasing by 1.4% to surpass $69. Despite the International Energy Agency (IEA) predicting a global oil market surplus of over one million barrels per day next year, US EIA gasoline inventories dropped sharply by more than 4 million barrels last week, hitting a two-year low, indicating a rebound in demand to last year's high, supporting the rise in oil prices:

US Oil: WTI December crude futures rose by $0.27, an increase of over 0.39%, closing at $68.70 per barrel. During the Asian afternoon session, US oil fell by more than 0.7%, approaching $67.90, and in pre-market trading, it rose by over 1.4%, nearing $69.40.

Brent Oil: Brent January crude futures rose by $0.28, an increase of 0.39%, closing at $72.56 per barrel. Brent oil fell by nearly 0.7% to below $71.80 in European stock pre-market, while in US pre-market trading, it rose by over 1.3%, breaking above $73.20.

On the news front, the International Energy Agency (IEA) released a monthly report stating that if OPEC+ continues to push forward with its production recovery plans, the global oil supply surplus will further exacerbate. Last week, US EIA crude inventories increased by more than 2 million barrels, while gasoline inventories sharply declined by over 4 million barrels. Due to weak oil demand, ubs group lowered its forecast for Brent crude prices from $87 per barrel to $80 per barrel.

Natural Gas: US December natural gas futures fell by approximately 6.64%, closing at $2.7850 per million British thermal units. European benchmark TTF Dutch natural gas futures rose by 5.53%, closing at €46.275 per megawatt hour. ICE UK natural gas futures rose by 5.43%, closing at 116.800 pence per kilocalorie.

A strong US dollar pressured metals, leading to a decline in London’s base metals markets, with gold dropping to a two-month low. Following the Republican Party's overwhelming victory in the November 5 elections, gold prices have fallen by over $170.

Gold: COMEX December gold futures closed down 0.59% at $2571.20 per ounce, hitting a daily low of $2541.50 at 17:52 (UTC+8). Spot gold fell more than 1.4% in early European trading to below $2530, then saw a V-shaped rebound during regular trading hours in the USA, but turned down again after Powell's speech, closing down 0.25% at $2566.54 per ounce.

Silver: COMEX December silver futures closed down 0.38% at $30.545 per ounce, hitting a daily low of $29.750 at 17:51 (UTC+8). Spot silver fell nearly 2.1% in early European trading below $29.70, then rose more than 1.1% to above $30.70 at the close.

Among London industrial metals, lead and tin fell about 2.4%, and zinc dropped about 1.3%: copper closed down $57, a decrease of 0.63%, reported at $8990 per ton. COMEX copper futures fell 0.11%, reported at $4.0783 per pound. Aluminum closed down $14, reported at $2516 per ton. Lead closed down $48, a decline of 2.39%, reported at $1960 per ton. Zinc closed down $38, down more than 1.27%, reported at $2942 per ton. Nickel closed down $111, reported at $15619 per ton. Tin closed down $731, a decrease of more than 2.46%, reported at $28932 per ton. Cobalt remained flat, reported at $24300 per ton.

Editor/rice

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AUD/JPY trades above 111.00 after paring recent losses

NZD/USD recovers early lost ground; climbs back closer to 0.6000 amid modest USD pullback

Jupiter surges 17% after rebound – Traders still bet on JUP’s dip

国际金融协会警告:特朗普任期内,美国国债将“爆炸式增长”