Kinross Gold's 2025 Performance and BofA's Target Price: Analyzing Through a Commodity Equilibrium Lens

Kinross 2025 Performance: A Strong Foundation for the Gold Market

Kinross’s 2025 results have established a solid operational and financial platform for the company as it navigates the current gold market landscape. The company achieved its production objectives, delivering 2,152,000 ounces of attributable gold over the year, fully in line with its guidance. This reliable output, paired with careful cost management, led to an outstanding financial year.

One of the most notable achievements was Kinross’s cash generation. Kinross recorded a historic $2.5 billion in free cash flow for 2025, representing an 85% increase compared to the previous year. This impressive liquidity, driven by robust production and strong margins, enabled the company to return a substantial $1.5 billion to shareholders and debt holders through dividends and share repurchases.

These results highlight Kinross’s ability to efficiently produce gold and translate that output into significant cash flow, even amid fluctuating gold prices. The company’s strong cash position provides the flexibility to manage its finances, invest in future growth, and reward shareholders—key strengths as Kinross looks toward 2026.

Gold Price Trends: Supportive Yet Unpredictable

The external environment for gold remains highly favorable, offering a strong backdrop for Kinross’s operations. By late February 2026, gold’s spot price was around $5,187 per ounce, close to record highs. This follows a dramatic rally, with prices peaking near $5,589 in January and surging more than 64% during 2025. Major financial institutions remain optimistic: Goldman Sachs has raised its year-end 2026 forecast to $5,400 per ounce, while J.P. Morgan anticipates an average price of $5,055 in the final quarter. These projections reflect a fundamental shift in demand, not just a typical commodity cycle, with central bank purchases and investor hedging against macroeconomic risks cited as primary drivers.

Central banks, particularly China, are leading the way in diversifying reserves away from the US dollar, with Goldman predicting average monthly purchases of 60 tonnes in 2026. At the same time, investors are increasing their exposure to gold through ETFs, physical holdings, and options, seeking protection against long-term currency devaluation. These positions are considered “sticky,” reflecting deeper structural changes rather than short-term speculation.

While this environment supports high prices, it also introduces volatility. Gold has shown remarkable resilience, posting consecutive monthly gains throughout most of 2025. However, the rally’s strength, fueled by a mix of structural and speculative demand, means prices remain sensitive to shifts in sentiment. For Kinross, this translates into operating in a lucrative but potentially turbulent market.

Looking Ahead to 2026: Production, Costs, and Shareholder Returns

Kinross’s strategy for 2026 emphasizes stability and prudent management. The company has outlined clear targets: attributable gold production between 2.1 and 2.3 million ounces and an all-in sustaining cost (AISC) of $1,380–$1,480 per ounce. This approach ensures a predictable output and a competitive cost base, which are crucial for maintaining healthy margins in a volatile price environment.

Key assets such as Tasiast and Paracatu are expected to play significant roles in achieving these goals. Kinross’s disciplined approach to capital allocation further strengthens its financial position. Management has committed to returning 40% of free cash flow to shareholders in 2026, following the record $1.5 billion distributed in 2025. This underscores the company’s focus on rewarding investors.

This outlook offers several advantages. Consistent production supports market supply, while a competitive cost structure ensures strong cash flow even if gold prices retreat from their highs. This dual focus enables Kinross to fund dividends, reduce debt, and invest in growth, all while maintaining a robust balance sheet.

Key Drivers and Risks for 2026

Kinross’s investment case for 2026 centers on two main factors: the company’s ability to deliver on its operational plan and the sustainability of elevated gold prices. The primary catalyst is straightforward—successfully achieving the 2026 production and cost targets. Meeting these objectives is crucial for converting 2025’s record cash flow into ongoing returns. This will allow Kinross to maintain its pledge to return 40% of free cash flow to shareholders. Any shortfall in production or cost overruns would directly impact the company’s ability to generate cash and fulfill its strategy.

The main external risk is whether gold prices can remain at their current elevated levels. The recent rally has been driven by specific demand factors that may not persist. A significant drop from the current price near $5,200 would compress margins for producers like Kinross, threatening the strong cash flow seen in recent years. While banks such as Goldman Sachs point to ongoing central bank buying and investor hedging as support, these factors are not guaranteed. If investor sentiment shifts, volatility could increase.

Central bank demand, particularly from China, remains a crucial variable. Goldman forecasts average monthly purchases of 60 tonnes in 2026. Any sustained reduction in buying from major reserve holders would signal weakening support for current price levels, potentially prompting a reassessment of the outlook for gold producers.

Ultimately, 2026 will test both Kinross’s operational discipline and the broader market’s appetite for gold as a hedge against long-term risks. The company’s guidance sets a clear path, but the outcome will depend on the stability of the underlying commodity environment.

BofA’s Upgraded Target: Market Confidence and Company Strength

Bank of America’s recent decision to raise its price target for Kinross reflects growing market confidence, underpinned by a positive gold outlook and Kinross’s proven execution. On February 26, the bank increased its target for Kinross Gold to $42.75 from $37.50, maintaining a Buy recommendation. This move followed Kinross’s February 18 announcement, which confirmed the company had met all key guidance metrics for 2025.

The timing of the upgrade is notable, as it directly responded to Kinross’s confirmation of its operational and financial strategy. The company’s record $2.5 billion in free cash flow and $1.5 billion returned to shareholders demonstrated its ability to generate significant liquidity within a competitive cost structure, providing a solid basis for the stock’s valuation.

BofA’s rationale is closely tied to both commodity market dynamics and Kinross’s fundamentals. The bank’s revised gold price forecasts for 2026, which align with the structural demand trends discussed earlier, provide macroeconomic support. On the company level, the target increase reflects confidence in Kinross’s strong balance sheet and disciplined approach to capital allocation. The company’s robust cash flow enables it to fund operations, pay down debt, and return capital to shareholders—core elements of its 2026 strategy.

In summary, BofA’s upgrade combines positive market conditions with Kinross’s demonstrated operational excellence. The higher price target acknowledges both the likelihood of continued gold market strength and Kinross’s ability to capitalize on these conditions through efficient operations and strong cash generation.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

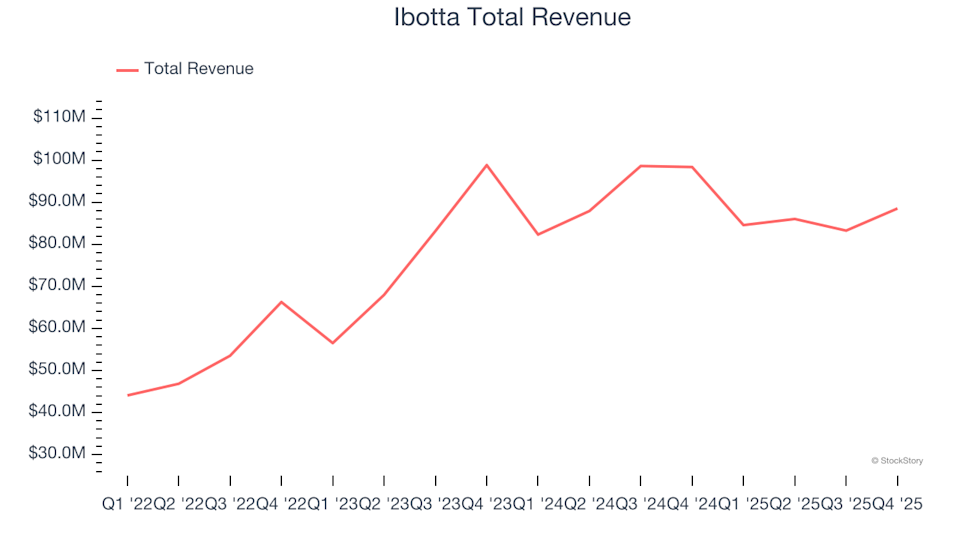

Advertising & Marketing Services Stocks Q4 Performance: Comparing Ibotta (NYSE:IBTA)

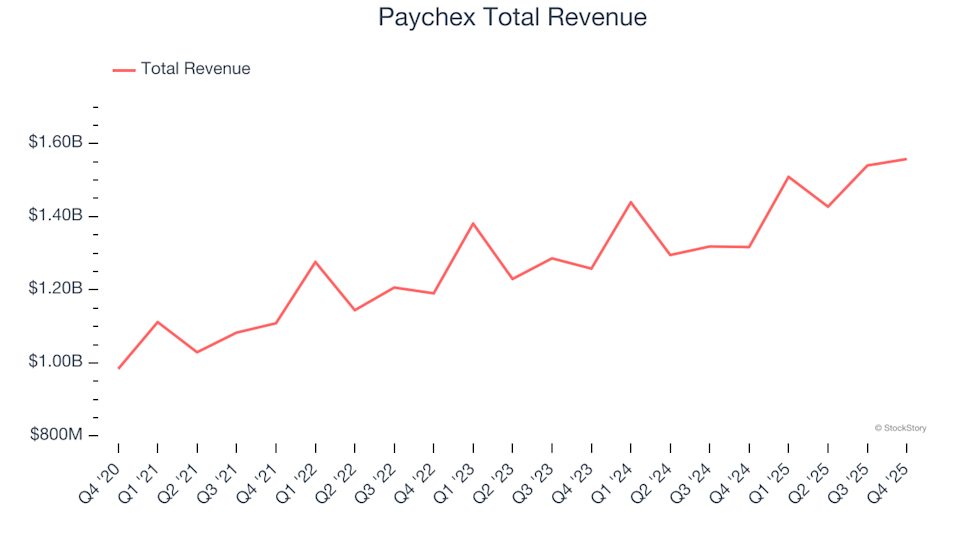

HR Software Stocks Q4 Recap: Paychex (NASDAQ:PAYX)

Three Bitcoin signals show $80K is next BTC price target for bulls