Trip.com: After the Regulatory "Crackdown", Can It Still Be "Small and Beautiful"?

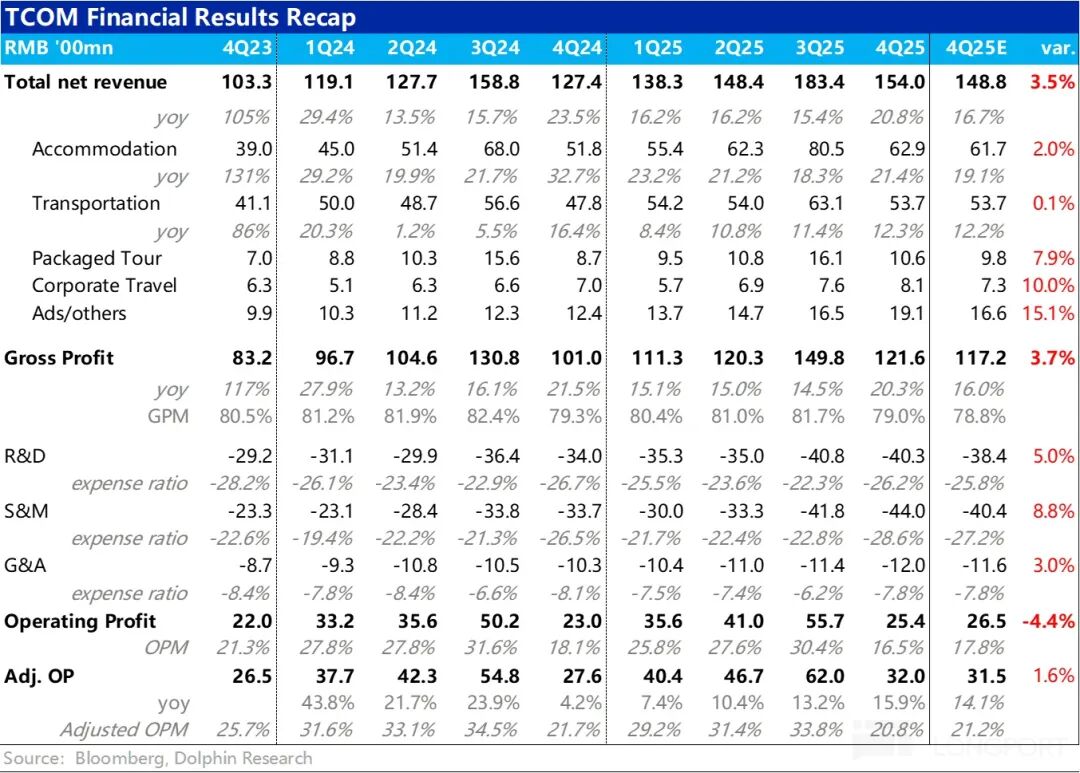

Early this morning on February 26, after the US stock market closed, Trip.com, which is currently under regulatory scrutiny, released its Q4 2025 fiscal year earnings report. Overall, the performance was not bad, with revenue growth broadly surpassing previous guidance and continuing to accelerate. However, operating expenses also rose across the board, increasing faster than revenue, resulting in GAAP operating profit falling short of expectations. Specifically:

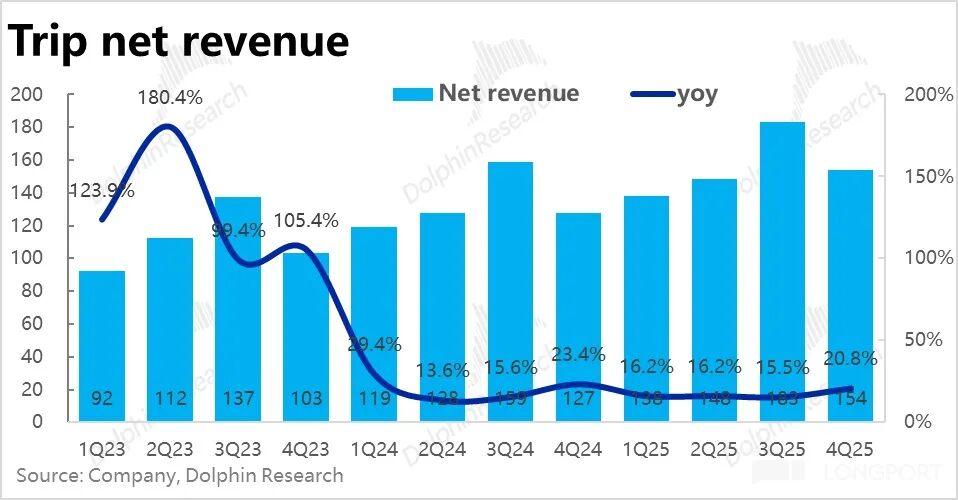

1. Strong revenue and accelerating growth: In terms of income, this quarter, Trip.com Group's overall net revenue posted a year-on-year growth rate as high as 21%, hitting a new high for the year, with a noticeable acceleration compared to the previous quarter.

Revenue growth across all business lines exceeded previous guidance and accelerated as well. Specifically, the larger-scale hotel and ticketing revenues performed steadily and slightly better than expected. However, the main reasons for the revenue beat were the three "smaller" businesses: corporate travel, packaged tours, and advertising & others.

Among them, the year-on-year revenue growth of packaged tours and advertising businesses exceeded 20% and 50% respectively, far surpassing expectations. According to the company, this was mainly due to strong sales of outbound/international travel products and incremental advertising revenue from overseas business expansion.

2. Overseas business maintains rapid growth, now accounts for nearly half of the group: According to disclosures, pure overseas business, Trip.com, saw booking volume growth of 60% YoY this quarter, the same as last quarter, maintaining rapid growth even as it moves into a high base period.

International business (pure overseas + outbound) accounted for about 40% of the group's total revenue in 2025, up from 35% in 2024, further highlighting its growing importance and contribution to the group.

Pure overseas business revenue is mainly contributed by mature developed markets such as Hong Kong and Singapore, while emerging markets like South Korea, Malaysia, and Indonesia are seeing rapid growth.

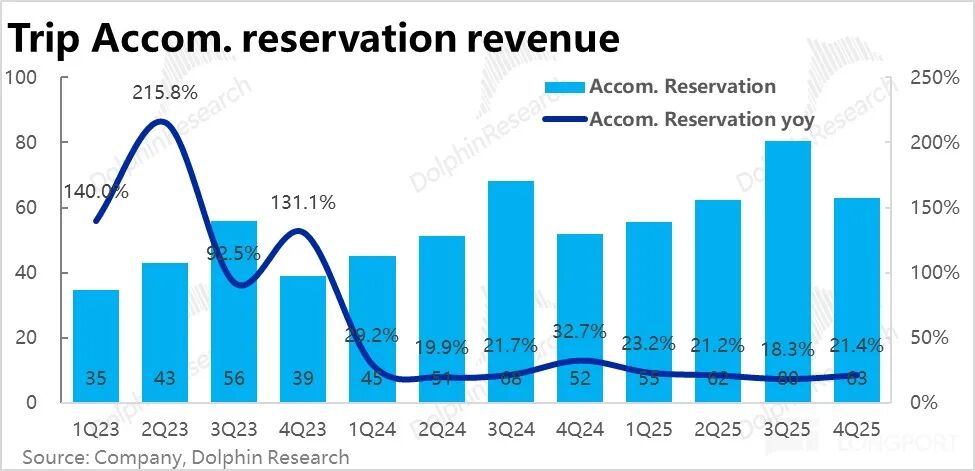

3. Domestic demand stabilizes: Among the two pillar businesses, hotel booking revenue grew about 21% YoY, accelerating by over 3 percentage points compared to the previous quarter, exceeding the upper end of previous guidance. Domestic hotels, which contribute the majority of revenue, saw bookings rise over 10% YoY, and average spending per order also stabilized and began to recover, indicating that domestic hotel and travel demand remains robust.

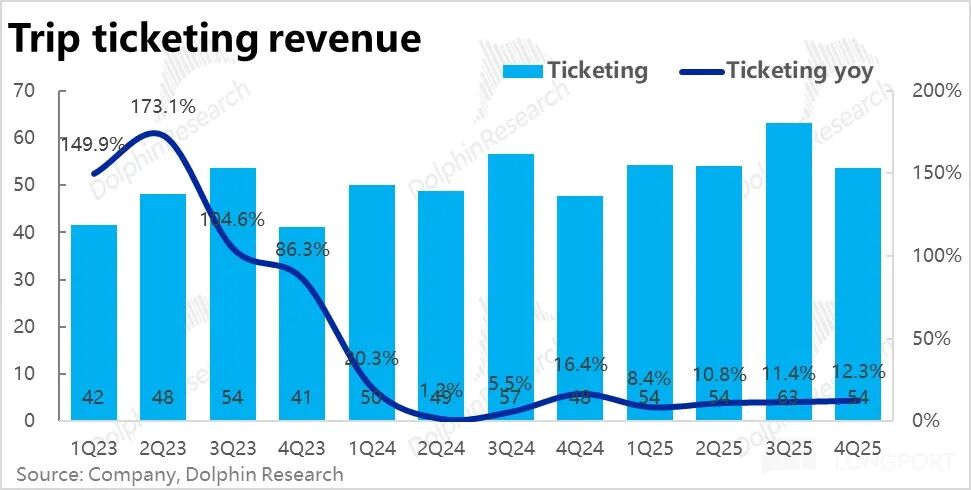

Ticketing revenue grew 12.3% YoY this quarter, with a slight acceleration quarter-on-quarter. On one hand, domestic transportation ticket revenue is still declining YoY due to deliberate reductions in additional charges (possibly also under regulatory pressure). The main driver is higher per-ticket revenue from international air tickets.

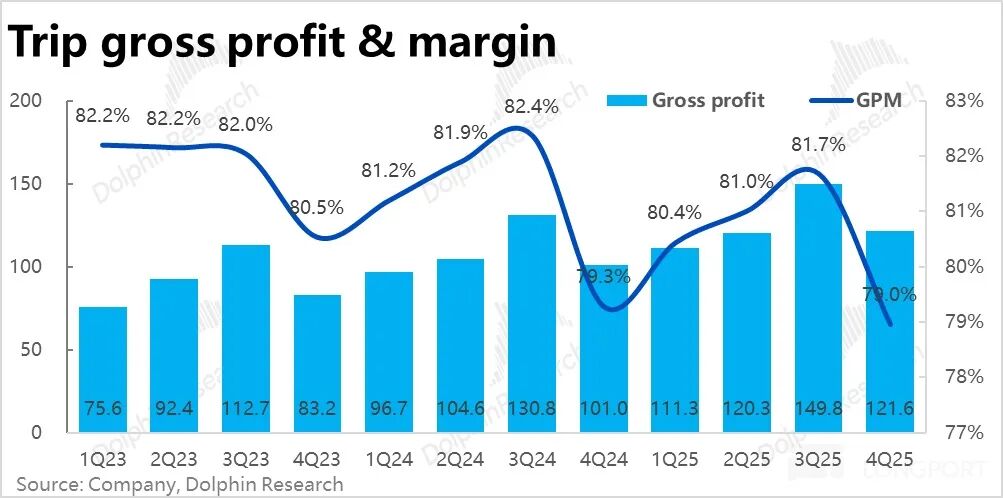

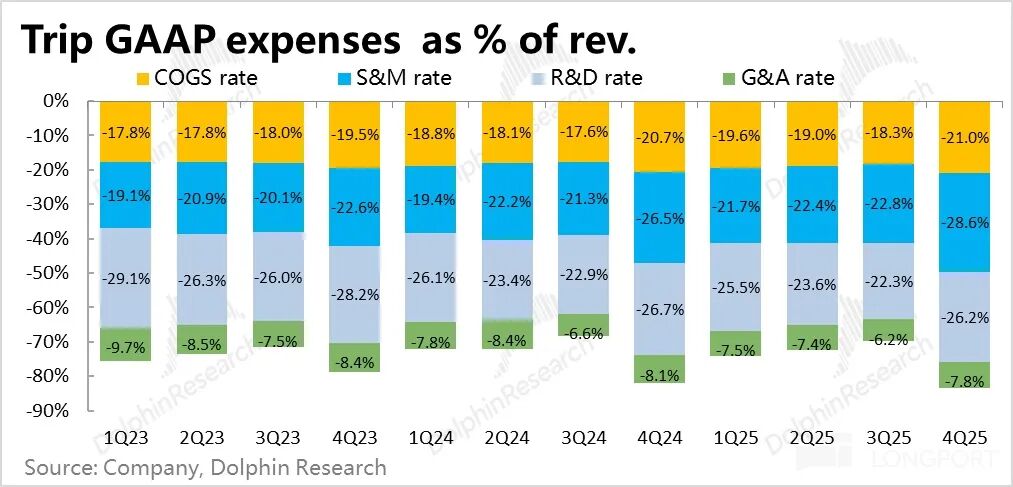

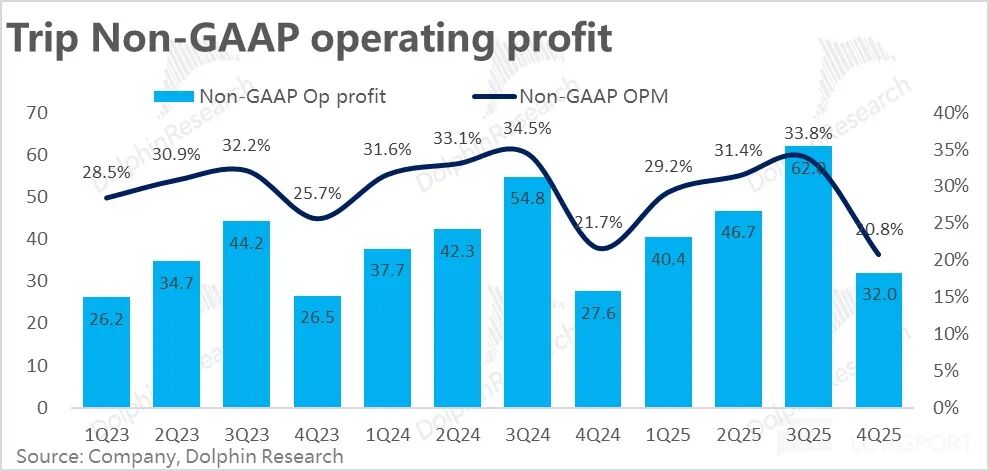

4. Gross margin decline narrowed: This quarter's gross margin was 79%, narrowing by 0.3 percentage points YoY, still shrinking but at the smallest rate in recent quarters. Previously, the decline was mainly due to the growing proportion of lower-margin overseas business, so as the profitability of overseas business improves, its drag on overall gross margin is also easing.

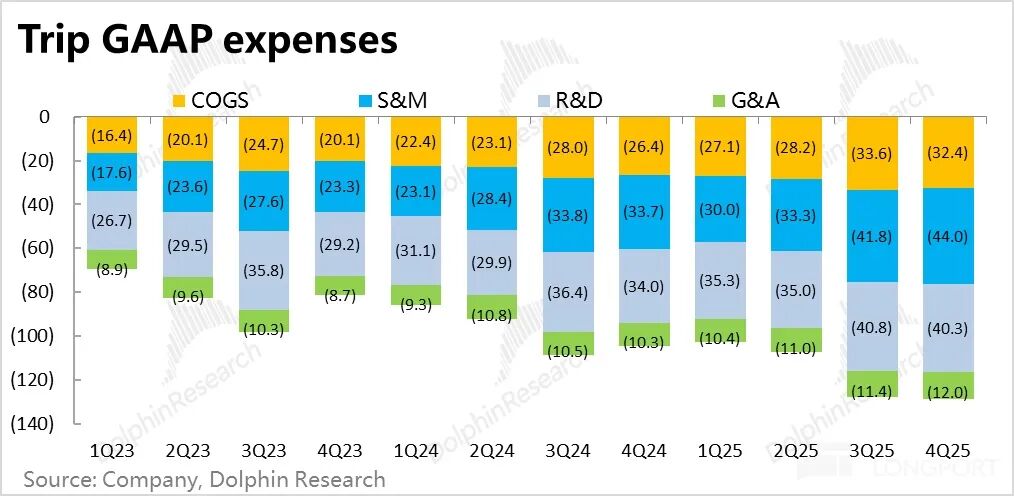

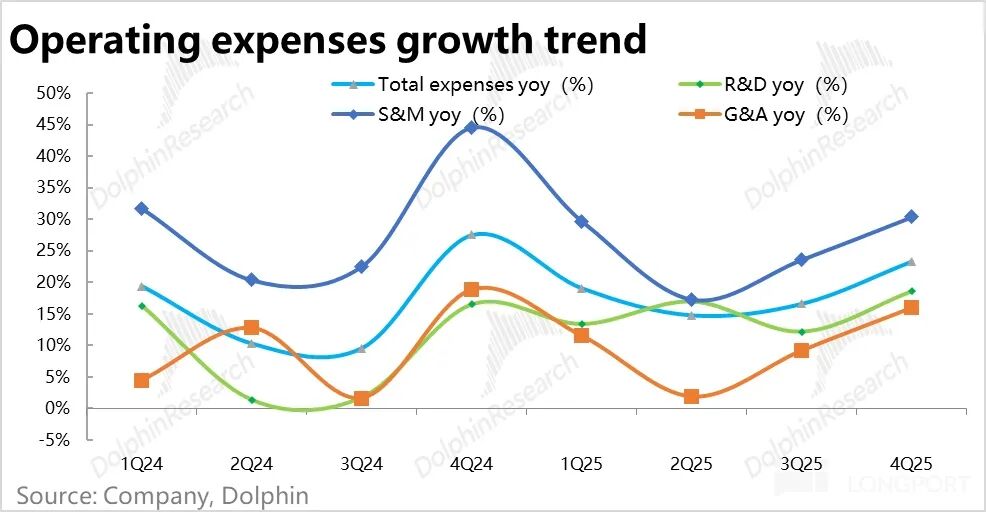

5. Significant rise in expenses, poor profit performance: This quarter, Trip.com's total operating expenses rose sharply by 23% YoY, with a clear acceleration from the previous quarter, and faster than revenue growth. Mainly, marketing expenses grew over 30% YoY, primarily for overseas expansion, though increased domestic competition may also play a role.

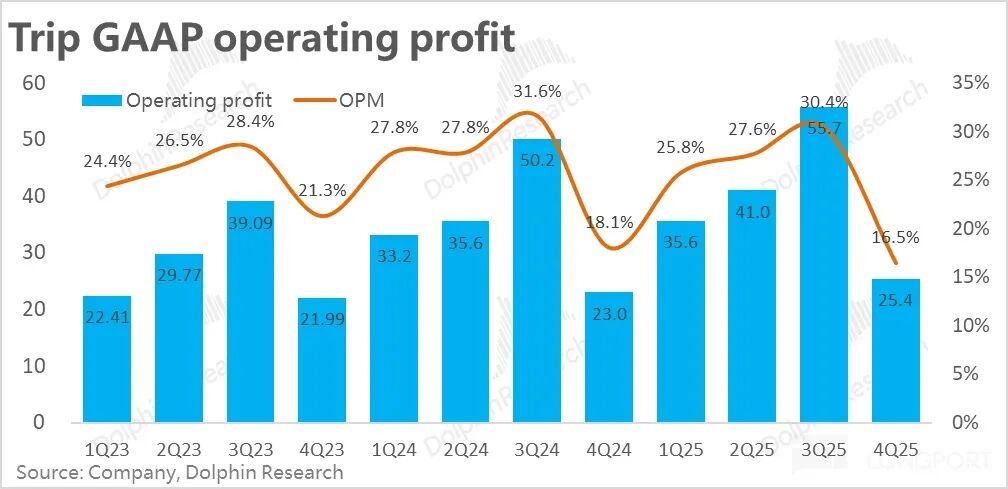

With gross margin slightly down and expenses growing faster than revenue, GAAP operating margin narrowed by 1.6 percentage points YoY, significantly below market expectations, resulting in GAAP operating profit increasing only about 10% YoY.

6. Major board reshuffle: In addition, Trip.com this quarter announced that original co-founders and board members Fan Min and Ji Qi resigned from the company, and two new independent directors were added. Both new directors come from financial backgrounds. According to the company, the change aims to optimize the board structure (more diversity and external backgrounds).

Dolphin Research Views:

1. Looking at the quarterly results, this quarter was mixed—on the positive side, business and revenue growth beat expectations across the board, domestic hotel and travel demand remained strong, and rapid overseas growth continued to drive the overall group. In terms of growth potential, it remains a leading large-cap Chinese stock.

As for shortcomings, the obvious issue is the sharp increase in expenses, which led to unimpressive profit growth. While the company attributes this mainly to overseas investment, it can't rule out that with domestic players like JD.com, Fliggy, and Douyin eyeing the travel business, customer acquisition and marketing needs in China are also increasing.

Given that Trip.com is already under regulatory investigation and market sentiment is sensitive, a mixed rather than an all-around beat may not be enough to fully reverse the current weakness in its stock price.

2. Looking ahead to the company's performance, based on guidance from the company meeting (at the upper end), total revenue growth is expected to be 17% next quarter, which will be somewhat slower than this quarter (though it can't be ruled out that the company is deliberately lowering expectations).

Specifically, core hotel and ticketing business growth is expected to be roughly the same as this quarter. The main drag will be advertising revenue, as the high base will likely slow growth from over 50% this quarter to around 20%.

Expense spending, especially marketing expenses, is expected to continue growing rapidly, possibly increasing by about 2 percentage points as a share of revenue, still driven by overseas investment. Thus, adjusted profit YoY growth may still be just over 10%.

In summary, similar to this quarter, growth remains solid (slowing slightly due to the high base), but profits remain weak.

3. On the business side, a. Domestic hotel and travel demand is generally stable, and average hotel spending per order has begun to stabilize and recover, providing steady growth prospects for the hotel and travel business. Ticketing volume growth is in line with the industry, but pure ticket sales generate limited revenue, while high-margin ancillary services like bundled insurance & ticket snatching must be kept low-profile in the current regulatory climate, so future income may still decline.

b. For overseas business, Trip.com is expected to maintain a 60% growth rate in order value, driving revenue from overseas hotels, packaged tours, and air tickets.

At the same time, in terms of profit, Trip.com's loss rate narrowed to low double digits by H2 2025, and will continue to naturally shrink with business growth, so breaking even is expected (though there is no clear timetable).

4. Outside of performance, the market's biggest concern is undoubtedly the potential impact of regulation. The actual impact of possible withheld payments may be limited.

More importantly, will this significantly impact Trip.com's competitive position and monetization potential in China? Although there is no official statement yet regarding specific regulatory developments, the company made no comments during this earnings call either.

According to media reports, the main regulatory concerns are that Trip.com uses an "automatic price adjustment" tool to semi-coercively require partner hotels to offer the lowest price on the internet, and also requires "special" hotels to not join other platforms—a classic "choose one of two" practice, both suspected of monopolistic behavior.

On this, Dolphin Research believes that since hotel and travel (especially high-end) supply is more limited and exclusive compared to goods, Trip.com's business moat may be higher than imagined. Drawing on previous experience from Alibaba and Meituan's antitrust investigations, mere regulatory scrutiny is unlikely to significantly affect Trip.com's market share, but it could lower the monetization ceiling for domestic hotels.

Besides this main risk, other factors include potential intensifying competition in China and possible disruption of OTA platforms by AI Agents—uncertain risks that may or may not materialize, but the problem is, the market currently dislikes "uncertainty." For example, the possibility of AI replacing SaaS or autonomous driving replacing ride-hailing—these uncertainties haven't stopped software companies and Uber from being continuously sold off.

A more detailed value analysis has been published in the Longbridge App's "Trends–In-depth (Investment Research)" section under the same title.

Detailed Review Below

I. Core businesses remain solid, "smaller" businesses deliver surprises

This quarter, Trip.com Group's overall net revenue was about 15.4 billion yuan (excluding business tax), with a year-on-year growth rate rising to 21%, the highest quarterly growth this year, showing strong momentum.

Specifically, hotel and ticketing revenue, which account for the largest share, grew steadily this quarter, both accelerating over last quarter and slightly exceeding previous guidance. The main sources of the revenue beat were corporate travel, packaged tours, and advertising & others—three smaller-scale businesses. Their actual growth far exceeded previous guidance, with YoY growth of packaged tours and ad revenue both above 20% and 50% respectively.

According to disclosures in the earnings call, the main contributors were international packaged tour products and incremental ad revenue from overseas business.

1. Solid core growth, slight acceleration

By revenue type, this quarter, hotel booking revenue grew about 21% YoY, accelerating by over 3 percentage points compared to the previous quarter, exceeding the upper end of prior guidance (18%–19%). Apart from the high base effect, both domestic and overseas hotel average order values still show a downward trend, which should also be one of the reasons hotel and travel revenue growth keeps decelerating.

Ticketing revenue grew 12.3% YoY this quarter, with a continued slight quarter-on-quarter acceleration. As previously mentioned, with last year's deliberate reduction in bundled ticket sales gradually fading, ticketing revenue growth is steadily recovering. Additionally, according to the company, growth in higher average income international air tickets was also a key contributor.

2. Advertising and corporate travel outperformed expectations

For the other three smaller-scale businesses that outperformed expectations:

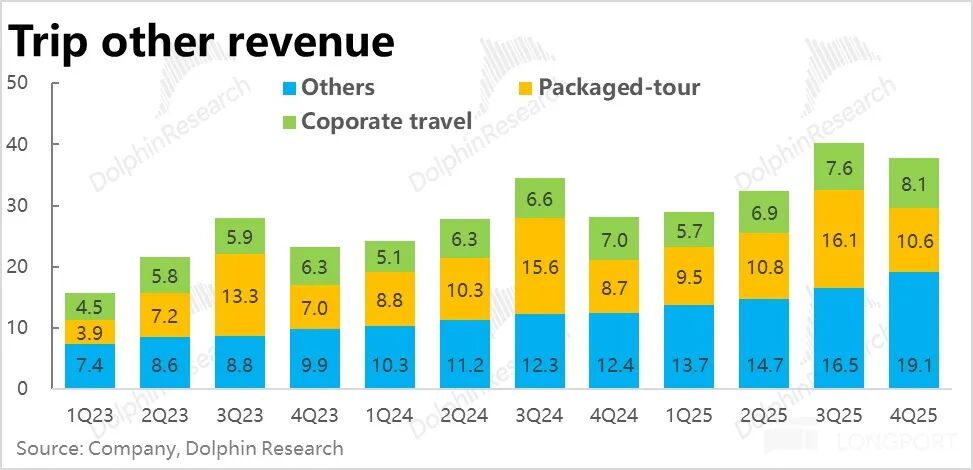

1) Corporate travel revenue was 810 million, up 15% YoY, consistent with last quarter's growth, also far better than previous guidance, which was only 4%. According to the company, the outperformance was due to higher penetration of corporate travel services.

2) Packaged tour product revenue was 1.06 billion, up 21% YoY, far exceeding expectations and showing a marked acceleration from previous single-digit growth. According to the earnings call, this was due to international outbound vacation tours and domestic senior tourism.

3. Other revenue, mainly from advertising, surged 54% YoY, far exceeding expectations. The company said this was thanks to incremental ad revenue from outbound and pure overseas business.

II. Expenses rise significantly, profit performance poor—overseas expansion or competitive pressure?

Regarding profit performance, this quarter's gross margin was 79%, narrowing by 0.3 percentage points YoY, still shrinking but at the slowest rate in recent quarters. Previously, the decline was mainly due to the increasing share of lower-margin overseas business, so as overseas business profitability improves, its drag on overall gross margin is lessening.

On expenses, Trip.com's total operating expenses grew sharply by 23% YoY this quarter, clearly accelerating compared to last quarter and faster than revenue growth.

Specifically, marketing expenses grew over 30% YoY, and while the company said this was mainly for overseas expansion, the impact of rising domestic competition (from JD.com, Fliggy, Douyin, etc.) cannot be ruled out.

Meanwhile, R&D and administrative expenses also grew compared to last quarter, reaching around 16%–18%, indicating the company is in a period of broadly expanding spending.

On a GAAP basis, with gross margin still slightly down and expenses rising sharply, the two combined, GAAP operating margin narrowed by 1.6 percentage points YoY to 16.5%, significantly below market expectations. GAAP operating profit thus only grew about 10% YoY.

After adding back stock-based compensation, non-GAAP operating profit was 3.2 billion yuan, up 16% YoY, slightly beating market expectations. This was mainly because stock-based compensation this quarter was higher than last year, at 4.3% of total revenue, compared to 3.6% last year.

Dolphin Research does not agree with excluding stock-based compensation from expenses, and mainly references GAAP-based results.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Hyperliquid price prediction – HYPE eyes $38, but watch THIS golden pocket first

If You’re Bearish on XRP, Listen to What David Schwartz Said

刚刚!央行重磅表态:降准还有一定空间

深夜放鹰!鲍威尔:经济强劲,美联储无需急于降息,有时间了解特朗普政策影响