February employment report, Broadcom’s financial results, and growing concerns about AI: Key events to monitor this week

Market Recap: Early 2026 Performance

The first two months of 2026 have wrapped up, offering a mixed picture for major US stock indices. The S&P 500 ended Friday at 6,878.88, down about 0.5% for the week but still up roughly 0.5% since the start of the year. The Dow Jones Industrial Average dropped around 1% (about 520 points) on Friday, yet it has gained 1.9% year-to-date. Meanwhile, the Nasdaq Composite, known for its technology focus, declined 0.9% on Friday and is now down approximately 2.5% for 2026.

Key Market Drivers and Sector Pressures

Nvidia's impressive quarterly results on Wednesday failed to calm concerns about ongoing disruptions from artificial intelligence. Additionally, renewed selling in private credit lenders highlighted persistent stress within the financial sector.

Looking ahead, investors are focused on the upcoming February employment report and a significant earnings release from Broadcom, a major player in the semiconductor industry.

Geopolitical risks remain in the spotlight as well. Tensions between the United States and Iran continue, with recent Geneva negotiations ending without resolution. The US embassy in Jerusalem has allowed nonessential staff and their families to leave, reflecting heightened military activity in the region.

What to Watch This Week

The highlight of the economic calendar is Friday’s jobs report for February. Economists anticipate that 60,000 new positions were added last month, a slowdown compared to the 130,000 jobs created in January—a figure that far exceeded expectations and helped ease concerns about a potential economic downturn.

Additional data releases include manufacturing updates from S&P Global and the Institute for Supply Management on Monday, as well as labor market figures from ADP and weekly jobless claims, due Wednesday and Thursday, respectively.

On the corporate front, attention will be divided between developments in artificial intelligence and trends in US consumer spending. Broadcom’s earnings on Wednesday will provide further insight into AI demand, following Nvidia’s report. Marvell Technology is set to report on Thursday.

Retailers will also be in focus, with Target and Costco releasing results on Tuesday and Thursday, respectively. Other notable reports will come from Ross Stores, Kroger, BJ’s Wholesale Club, and Macy’s.

AI: Increasingly Viewed as a Risk

Nvidia once again surpassed Wall Street’s expectations for both revenue and adjusted earnings, with CEO Jensen Huang emphasizing the surging demand for the company’s chips during the earnings call. However, this strong performance was not enough to reassure investors.

Nvidia’s stock dropped about 4.8% on Thursday following the report and fell another 4% on Friday, ending the week more than 6% lower. The broader market followed suit, with all three major indices closing in negative territory on Thursday and Friday.

According to Capital analyst Kyle Rodda, the challenge for Nvidia lies in shifting investor attitudes toward AI-related stocks. Despite concerns about supply constraints, Rodda noted that Nvidia’s quarterly results were essentially flawless. He observed that “AI is increasingly being seen as a source of risk rather than opportunity, with investors more intent on avoiding losses than seeking out winners in a market troubled by high valuations and excessive investment.”

This sentiment was amplified by the so-called “AI scare trade” earlier in the week, triggered by a report that envisioned widespread job losses among white-collar workers. Stocks identified as vulnerable in the report, such as IBM and Zscaler, suffered significant declines.

Bank of America strategists pushed back on the report’s conclusions, arguing that its scenario was inconsistent with established economic theory. They attributed the resulting sell-off to crowded trades and market psychology, likening it to a bank run sparked by unfounded rumors.

Labor Market Signals: Is There Cause for Concern?

During his State of the Union address, President Trump declared that more Americans are employed now than ever before. However, the current labor market tells a more nuanced story.

The most recent jobs report from the Bureau of Labor Statistics showed a surprising gain of 130,000 jobs in January, doubling consensus forecasts. This discrepancy between expectations and actual results makes the upcoming February report especially important.

Economists are again predicting a 60,000-job increase. Should the actual figure surpass expectations, it could help dispel fears that the labor market is deteriorating rapidly. Still, revisions to last year’s data indicate that employers added an average of just 15,000 jobs per month in 2025. Job openings have also declined for four consecutive months, according to the BLS Job Openings and Labor Turnover Survey.

“It’s a labor market characterized more by caution than strength,” said ADP chief economist Nela Richardson in a recent interview. The jobs report, along with any changes in the unemployment rate, could influence Federal Reserve policy decisions, as this week’s data will be among the last considered before the Fed’s March meeting.

BNP strategists noted that a strong February report could solidify expectations that the Fed will hold rates steady throughout 2026, or even consider a rate hike. However, they cautioned that the risk of a downturn may be underestimated. As of Friday, market participants were assigning a 94.2% probability that the Fed will maintain its current target range of 3.5%-3.75% at the March meeting.

Upcoming Economic and Earnings Highlights

Monday

- Economic Data: S&P Global manufacturing PMI (final February reading: 51.2 prior); ISM manufacturing (expected: 51.6, prior: 52.6); ISM prices paid (expected: 59.2, prior: 59.0); ISM new orders (prior: 57.1); ISM employment (prior: 48.1)

- Earnings: EchoStar Corporation, AST SpaceMobile, MongoDB, Venture Global, Norwegian Cruise Line Holdings, ADT, Riot Platforms, Life360

Tuesday

- Economic Data: Wards total vehicle sales (expected: 15.2 million, prior: 14.85 million)

- Earnings: Target Corporation, CrowdStrike Holdings, Ross Stores, AutoZone, Viking Holdings, On Holdings AG, Best Buy, New Gold, NextGen Energy, Versant Media Group

Wednesday

- Economic Data: MBA mortgage applications (week ending Feb. 27: +0.4% prior); ADP employment change (expected: +42,000, prior: +22,000); S&P Global US services PMI (final February: 52.3 prior); S&P Global US Composite PMI (final February: 52.3 prior); ISM services index (expected: 53.8, prior: 53.8); ISM services prices paid (expected: 67.0, prior: 66.6); ISM services new orders (expected: 53.6, prior: 53.1); ISM services employment (prior: 50.3); Federal Reserve Beige Book release

- Earnings: Broadcom, Veeva Systems, Ecopetrol, Brown-Forman Corporation, Okta, Dycom Industries, Rigetti Computing, Bath & Body Works, Abercrombie & Fitch, American Eagle Outfitters, Wix.com, StubHub Holdings, Firefly Aerospace, Webull Corporation

Thursday

- Economic Data: Initial jobless claims (week ending Feb. 28: 212,000 prior); Continuing claims (week ending Feb. 21: 1.83 million prior); Challenger job cuts (February YoY: +117.8% prior); Import price index (January MoM: +0.1% prior, YoY: +0.0% prior); Nonfarm productivity (Q4 preliminary: expected +1.6%, prior +4.9%); Unit labor costs (Q4 preliminary: expected +2.2%, prior -1.9%)

- Earnings: Costco, Alibaba Group, Marvell Technology, Ciena Corporation, The Kroger Co., Burlington Stores, BJ's Wholesale Club, The Gap, Macy's, Victoria's Secret

Friday

- Economic Data: Change in nonfarm payrolls (expected: +60,000, prior: +130,000); Unemployment rate (expected: 4.4%, prior: 4.3%); Average hourly earnings (February MoM: expected +0.3%, prior +0.4%; YoY: expected +3.7%, prior +3.7%); Retail sales (January MoM: expected -0.3%, prior +0.0%)

- Earnings: Algonquin Power & Utilities Corp.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Whale Trader pension-usdt.eth Secures $466K Profit After Surviving a $3.3M Bitcoin Drawdown

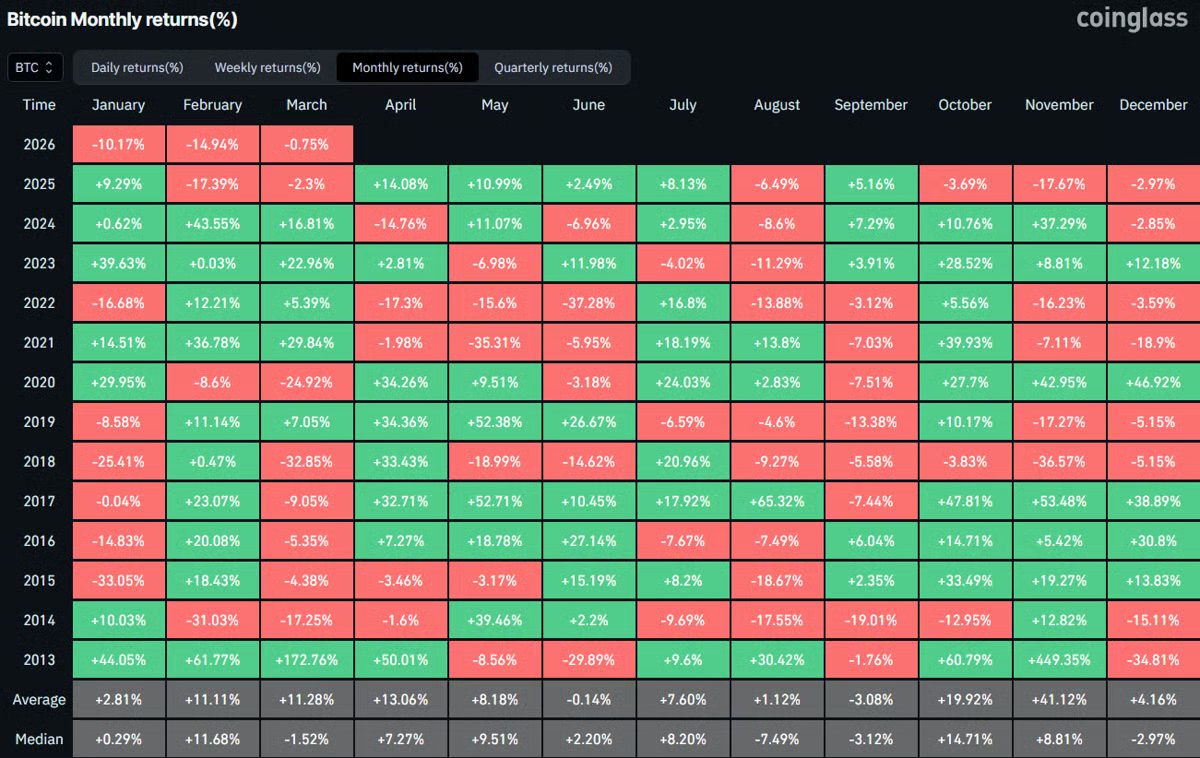

Bitcoin bulls defend $67 as BTC closes its 5th month down.

Bitcoin hard fork to recover $BTC from Mt Gox is rejected.

Goldman Sachs and Jefferies expand cryptocurrency research.