Global profits indicate a move away from the US as the S&P 500 declined

Key Takeaways from the Latest Earnings Season

As the most recent round of corporate earnings comes to a close, investors may have found it easy to overlook some notable developments amid the ongoing dominance of artificial intelligence in market discussions, global tensions, and renewed trade worries.

Despite these distractions, the quarterly reports revealed several important trends that could influence equity markets for the remainder of the year. While US companies posted impressive profit growth, strong performances were also seen internationally, reinforcing the case for diversifying beyond American equities into major Asian and European firms. However, even with solid US results, market reactions were mixed, with some companies facing skepticism over whether their growth has already peaked.

Top Stories from Bloomberg

Asian tech giants continued to thrive thanks to their central role in the AI revolution, while European consumer-focused companies faced ongoing challenges. Meanwhile, industrial and financial sectors in Europe benefited from increased government spending.

Performance Highlights and Key Figures

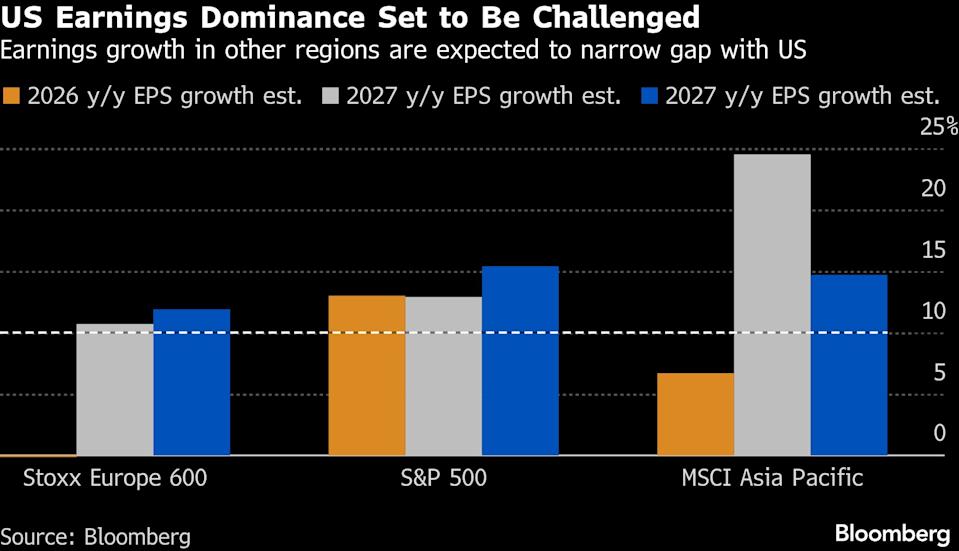

Here’s a summary of the main trends and standout performers. US and European profit growth exceeded expectations: S&P 500 companies saw earnings climb 13%, outpacing forecasts by five percentage points. Major European firms increased profits by 4.5%, triple the predicted rate.

However, fewer companies contributed to these positive surprises. Only about 75% of S&P 500 firms beat estimates—the lowest proportion in three years and a drop from 82% in the previous quarter. In Europe, just 47% of MSCI Europe constituents outperformed, below the five-year average of 54%.

Market Reactions and Outlook

Expectations for the remainder of the year were generally subdued, resulting in sharp declines for some companies despite meeting profit targets. US stocks were relatively flat during the period, while European and Asian markets saw gains.

The season was also marked by concerns over AI-driven disruption, particularly affecting software companies. Over the six-week period, the S&P 500 declined, whereas Europe’s Stoxx 600 rose nearly 4% and the MSCI Asia Pacific surged 11%.

Geopolitical risks, such as US actions against Iran, add another layer of uncertainty. Energy markets could experience price volatility, potentially impacting companies and economies in the near term and raising the stakes for investors.

“High expectations for earnings this season led to increased volatility around results,” observed Louise Dudley, Portfolio Manager for Global Equities at Federated Hermes. “Many companies were priced for perfection, so when growth or future guidance fell short, the market reacted strongly.”

Asia’s Valuation Upswing

Asia’s strong presence in the semiconductor industry has been a significant advantage. Companies like Taiwan Semiconductor Manufacturing Co., Korea’s SK Hynix, and Chinese foundries have positioned the region as a critical supplier for the chips powering global AI expansion. Additional energy capacity is also expected to support further profit growth.

Although US earnings are currently growing faster, the rest of the world is expected to catch up, narrowing the valuation gap and providing more reasons for international diversification.

“Investors can pay 16 times forward earnings in Europe or 23 times in the US for similar growth by 2027,” said Adrian Helfert, Chief Investment Officer at Westwood Management. “I’m most confident in the euro zone, especially European industrials, defense, and banks. This is a long-term structural shift, not just a defensive move.”

Mixed Signals from US Markets

Some major US tech firms, including Nvidia, Amazon, and Microsoft, saw their earnings met with disappointment due to lofty expectations and high valuations. Nvidia’s shares fell despite strong sales and optimistic forecasts. While tech companies drove S&P 500 earnings growth, much of this was already reflected in stock prices, and the so-called ‘Magnificent Seven’ have declined since the start of the year.

“There’s been a rise in disappointment during the US earnings season,” commented Tim Hayes, Chief Global Strategist at Ned Davis Research.

On the upside, profit growth outside of Big Tech is expected to catch up by 2026, according to Bloomberg Intelligence. This could justify a rebound in share prices for the rest of the S&P 500, without signaling a collapse for the leading tech firms.

Some investors believe the shift away from tech is overdone. “There are now attractive opportunities,” said Jay Hatfield, CEO of Infrastructure Capital Management, noting that Amazon trades at a lower price-to-earnings ratio than Walmart, despite stronger growth prospects.

Is Growth Peaking?

Gina Martin Adams, Chief Market Strategist at HB Wealth Management, noted that this robust US earnings season failed to spark a rally, possibly because companies have already reached their peak growth rates.

“Typically, earnings season is uplifting, but that wasn’t the case this time,” she remarked.

She suggests investors are adjusting to expectations of slower profit increases, with consensus pointing to 2026 growth merely matching 2025, rather than surpassing it. S&P 500 revenue growth may have peaked in the fourth quarter of last year at 8.1% year-over-year, the fastest since 2022.

“This slowdown in fundamentals could explain the broader market’s loss of momentum,” she added. “We need to see analysts revising forecasts upward.”

Europe’s AI Divide

Recent European earnings have reinforced ongoing trends: consumer-focused stocks continue to struggle, while financial, technology, and industrial companies show strength.

AI developments have overshadowed earnings for companies potentially threatened by new technologies, with sentiment often outweighing fundamentals. For example, Cap Gemini SE reported solid results, but its shares remain depressed after a sharp drop due to AI concerns.

Divergence is also emerging between software and hardware firms. ASML Holdings, a chip equipment maker, reported record orders and a positive outlook, while SAP SE, a German software leader, disappointed with slow cloud business growth.

Consumer stocks remain a weak spot. Stellantis NV tumbled after a significant writedown tied to its electric vehicle strategy, and Diageo Plc suffered its biggest-ever drop after cutting sales guidance and reducing its dividend due to US market weakness.

Asia’s Growing Appeal

Asian companies have demonstrated resilience, with gains in technology and AI-related sectors offsetting challenges from tariffs, sluggish global demand, and China’s uneven recovery.

Forward earnings estimates for MSCI Asia Pacific Index members have risen over 20% since September, according to Bloomberg data. Analyst forecasts for corporate profits in the region are at their highest relative to global peers since early 2023.

Optimism was fueled by Taiwan Semiconductor Manufacturing Co.’s strong results and guidance, with the company planning up to $56 billion in capital spending for 2026 and projecting nearly 30% revenue growth, signaling confidence in the ongoing AI boom.

“Robust earnings suggest more upside for the region,” wrote Goldman Sachs strategists led by Timothy Moe. “The outlook is especially bright in technology, and Japan’s election results support higher valuations.”

While the region performed better than expected, growth was uneven. North Asia, driven by semiconductor and AI demand, saw strong profits in Taiwan and parts of Japan, offsetting persistent weakness in China’s property and consumer sectors.

Japan’s earnings season delivered positive surprises, indicating stronger fundamentals than anticipated. In contrast, Chinese companies faced challenges, with Morgan Stanley noting a significant deterioration in profit forecasts for late 2025 due to weak consumer demand and deflationary pressures.

With contributions from Lin Zhu.

(This article has been updated to reflect the latest developments in the Middle East and corrects price levels in an earlier version.)

Most Popular from Bloomberg Businessweek

©2026 Bloomberg L.P.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

dogwifhat at $0.20: Reversal or further drop, what’s next for WIF?

"A sharp divide": Wall Street assesses the gains and losses as AI-fueled tech stocks tumble

How to Identify an Effective CEO: A Practical Guide

Bitcoin traders eye Iran reactions as oil sparks US 5% inflation forecast