Nvidia Shares Could Be Undervalued - Which NVDA Strategy Offers the Most Potential?

Nvidia (NVDA) Stock: Oversold Opportunity and Strategic Options Plays

Following its recent earnings announcement, Nvidia (NVDA) shares appear to be significantly oversold. Based on a free cash flow (FCF) analysis, the stock could have over 50% upside, as detailed in a February 27 Barchart article. Investors might consider two strategies: selling short out-of-the-money (OTM) puts for a potential 3% monthly yield, or purchasing in-the-money (ITM) call options with a six-month expiration.

On Friday, February 27, NVDA closed at $177.19, a decline from its pre-earnings high of $195.56 on February 25. Despite this drop, the price remains above the recent low of $171.88, with the six-month bottom at $167.02 recorded on September 5.

Related Insights from Barchart

- The Saturday Spread: Using an Overlooked Indicator to Assess True Market Risk

- Get the Barchart Brief newsletter for midday updates on stocks, sectors, and market sentiment—delivered when you need it most. Sign up for free!

The recent decline in NVDA may be excessive, especially considering the company’s robust free cash flow and strong FCF margins.

In the February 27 Barchart article, “Nvidia's Massive Free Cash Flow Margins Could Push NVDA Stock 45% Higher,” it was estimated that NVDA could reach a value of $263 per share.

Setting a Higher Price Target for NVDA

Here’s a breakdown of the price target calculation:

- Nvidia achieved a 44.7% FCF margin in 2025.

- Projected 2026 revenue is approximately $365 billion, which, at a 44% FCF margin, results in about $161 billion in FCF.

- Calculation: $364.38 billion x 0.44 = $160.3 billion

- Applying a 2.5% FCF yield, the company’s valuation could reach $6.41 trillion ($160.3 billion / 0.025).

- This is 49% above the current market cap of $4.307 trillion (per Yahoo! Finance), suggesting a price target nearly 49% higher than the current price.

- Price target calculation: $177.19 x 1.488 = $263

If Nvidia maintains these strong FCF margins through 2026, as management guidance suggests, the stock appears significantly undervalued. However, it may remain at these levels for some time, so investors should consider the best approach.

Strategy 1: Selling Out-of-the-Money NVDA Puts

Value-oriented investors seeking a lower entry point might consider selling short OTM puts with a one-month expiration. This approach allows investors to earn a premium while waiting for a potential dip in the stock price.

For instance, the April 2, 2026, $165 put—about 6.8% below the latest close—offers a premium of $5.15. Selling this contract yields an immediate one-month return of 3.12% ($5.15/$165.00).

How This Works in Practice

- The investor sets aside $16,500 as collateral (100 shares x $165 per contract).

- They “Sell to Open” one put contract at $165.00, allowing the brokerage to lend the contract for short sale.

- If NVDA stays above $165.00 by expiration, the contract expires and the collateral is released.

- The investor immediately receives $515 ($5.15 x 100 shares) as premium, equating to a 3.12% monthly yield.

- If assigned, the breakeven price is $159.85 ($165.00 - $5.15), nearly 10% below the current price.

For those seeking more downside protection, selling the $160.00 put (9.7% below the current price) yields 2.35% monthly ($3.90/$160.00) and lowers the breakeven to $156.10.

Strategy 2: Buying In-the-Money Calls

If NVDA’s price rises or never drops to $165.00, short put sellers miss out on upside gains. To capture potential appreciation, investors can also buy a six-month ITM call at the $165.00 strike.

For example, the September 18, 2026, $165 call has a midpoint premium of $32.80, costing $3,280 per contract. Its intrinsic value is $12.19 ($177.19 - $165.00), so the extrinsic value paid is $20.61 ($32.80 - $12.19), or $2,061 per contract.

Combining Both Strategies

- If an investor earns $515 per month selling OTM puts for six months, they accumulate $3,090—more than covering the extrinsic value of the call.

- Assuming $3,000 in total put premiums, the net cost for the call is $280 ($3,280 - $3,000).

- The effective cost per share if the call is exercised is $16,780 ($16,500 collateral + $280 / 100 shares = $167.80 per share).

- If NVDA closes at $220 on September 19, the profit would be $5,220 ($22,000 - $16,780).

- This results in a six-month ROI of 31.6% ($5,220 / $16,500).

- By comparison, a buy-and-hold investor would earn 24.16% ($220 / $177.19), or $4,281 for 100 shares, but without the benefit of the returned collateral.

By combining short OTM puts with ITM calls, investors can potentially enhance returns, benefit from downside protection, and accumulate income while waiting for a favorable entry point.

Conclusion

For value investors, the combination of selling OTM puts and buying ITM calls in NVDA at current prices offers an attractive way to generate income and participate in potential upside, all while managing risk.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Israel strikes Beirut after Hezbollah launches rocket attack

The Small-Cap Resurgence: Why the Russell 2000 is Outpacing the Giants in 2026

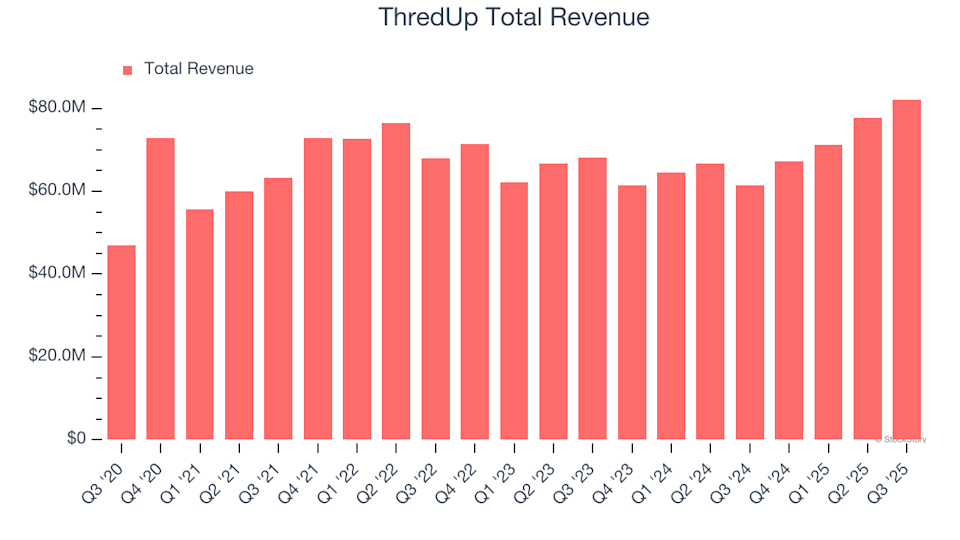

ThredUp (TDUP) Set to Announce Earnings Tomorrow: What You Should Know

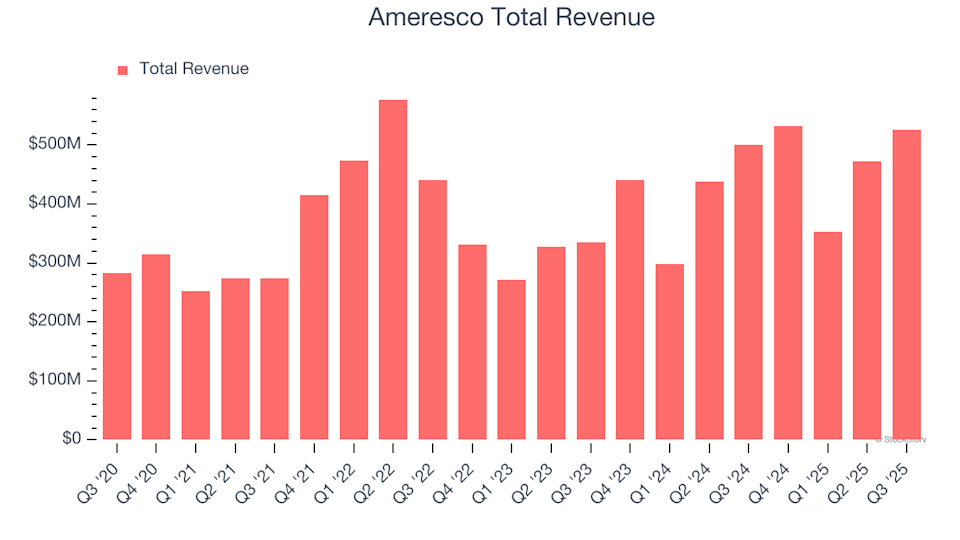

Ameresco (AMRC) Will Announce Earnings Tomorrow: What You Should Know