ADT (NYSE:ADT) Announces Q4 CY2025 Earnings With Revenue Falling Short of Analyst Expectations

ADT Q4 2025 Earnings Overview

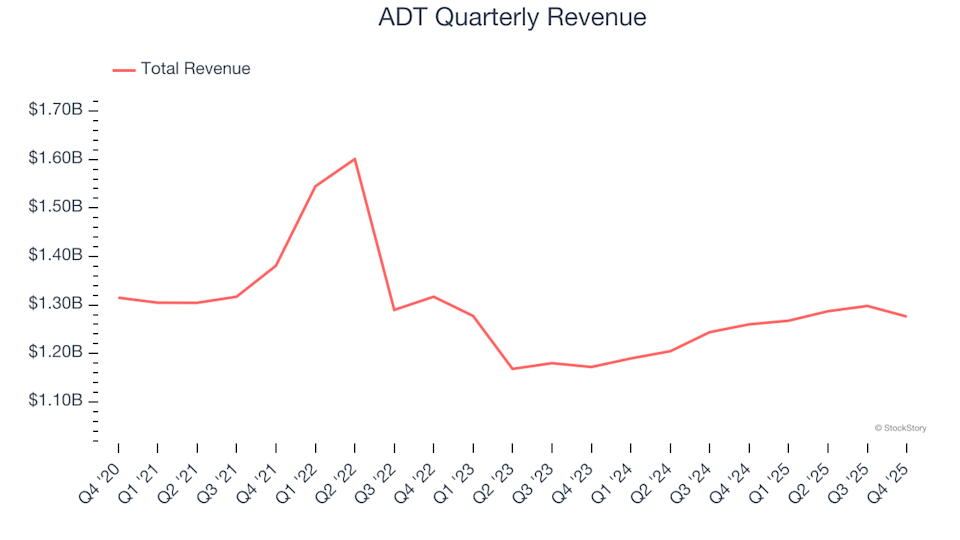

ADT (NYSE:ADT), a leader in security technology and services, reported fourth-quarter 2025 revenues of $1.28 billion, reflecting a modest 1.3% increase compared to the previous year. This figure fell short of market expectations. However, the company’s adjusted earnings per share came in at $0.23, matching analyst forecasts.

Highlights from ADT’s Q4 2025 Results

- Revenue: $1.28 billion, missing analyst expectations of $1.29 billion (1.3% annual growth, 1.2% below estimates)

- Adjusted EPS: $0.23, in line with projections of $0.22

- Adjusted EBITDA: $670 million, compared to the anticipated $682.4 million (52.5% margin, 1.8% below estimates)

- Operating Margin: 26.1%, an improvement from 24.2% in the same period last year

- Free Cash Flow Margin: 25.4%, up from 16.3% a year ago

- Market Cap: $6.52 billion

Jim DeVries, ADT’s Chairman, President, and CEO, commented, “ADT delivered another year of strong financial results in 2025, generating significant cash flow and reinforcing our financial position. As we move into 2026, we’re preparing to lead the next generation of smart home technology with our ADT+ platform and advanced ambient sensing features.”

About ADT

Established in 1874 and based in Boca Raton, Florida, ADT provides security, automation, and smart home solutions, serving both residential and commercial customers with a wide range of protection services.

Revenue Performance

Long-term growth is a key indicator of a company’s strength. While any business can have a few strong quarters, sustainable growth over years is more telling. ADT’s sales over the past year reached $5.13 billion, which is nearly unchanged from five years ago—an indication of stagnant performance and underlying business challenges.

Although the consumer discretionary sector often experiences short product cycles and volatile demand, ADT’s annualized revenue growth of 3.4% over the past two years outpaced its five-year average, which is a positive sign.

For the latest quarter, revenue increased by 1.3% year over year to $1.28 billion, but this was below Wall Street’s expectations.

Looking forward, analysts anticipate ADT’s revenue will rise by 3.6% over the next year, a rate similar to its recent trend. This suggests that new offerings are not expected to significantly boost sales in the near term.

Operating Margin Trends

ADT’s operating margin has remained relatively stable, averaging 25.1% over the past two years. This level of profitability is considered weak for a consumer discretionary company, largely due to an inefficient cost structure.

In the fourth quarter, the operating margin improved to 26.1%, up 1.9 percentage points from the previous year, indicating better operational efficiency.

Earnings Per Share (EPS)

While revenue growth shows how a company expands, changes in earnings per share (EPS) reveal how profitable that growth is. Over the past five years, ADT has transitioned from negative to positive full-year EPS, marking a significant milestone for the company.

For Q4, adjusted EPS reached $0.23, up from $0.20 a year earlier, surpassing analyst estimates by 3.4%. Wall Street expects ADT’s full-year EPS to climb to $0.90 over the next 12 months, representing a 5.5% increase.

Summary and Investment Perspective

ADT matched analyst expectations for EPS this quarter, but revenue came in slightly below forecasts, making for a somewhat disappointing period. Following the results, ADT’s share price declined by 1.7% to $7.89.

Is now the right time to invest in ADT? While quarterly results are important, evaluating the company’s long-term quality and valuation is crucial for investment decisions.

Bonus Insight: The Next Big Opportunity?

Did you know? There’s a satellite company capturing daily images of every spot on Earth—an asset coveted by the Pentagon and hedge funds alike. This could be the next Palantir.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

DEX volumes post best February performance since 2020

5 High-Growth Stocks Worth Considering in March Following a Turbulent February

Kozicki: Canada’s approach to monetary policy amid supply-related trade-offs on a global scale