3 Lucrative Stocks We Choose Not to Monitor

Profitable Companies That May Not Stand the Test of Time

While some businesses are currently generating profits, their long-term prospects may be questionable if they depend on outdated strategies or temporary advantages. A positive bottom line today doesn’t guarantee future success.

At StockStory, we evaluate companies from multiple perspectives because profitability alone doesn’t make a company a strong investment. Below, we highlight three profitable firms that fall short of our standards, along with alternative opportunities worth considering.

Utz (UTZ)

Recent GAAP Operating Margin (TTM): 1.4%

Utz Brands (NYSE:UTZ), which began as a family potato chip business in 1921, now produces a variety of salty snacks including chips, pretzels, cheese snacks, and popcorn.

Reasons We’re Cautious About UTZ

- Over the past two years, organic sales growth has been sluggish, suggesting the company may need to pursue strategic changes or acquisitions to accelerate expansion.

- With annual revenue of $1.44 billion, Utz has less leverage over fixed costs and fewer distribution options compared to larger competitors.

- Returns on capital are low, indicating challenges in effective capital allocation by management.

Utz shares are priced at $9.57, reflecting a forward P/E of 12.1.

Vulcan Materials (VMC)

Recent GAAP Operating Margin (TTM): 20.4%

Established in 1909, Vulcan Materials (NYSE:VMC) is a leading supplier of construction aggregates such as crushed stone, sand, and gravel.

Why We’re Wary of VMC

- Shipment volumes have grown slowly, indicating that customers are not adopting Vulcan’s products as quickly as anticipated.

- Analyst forecasts suggest demand will remain soft, with only 1.4% growth expected over the next year.

- The company’s gross margin of 25.2% points to significant production expenses.

Vulcan Materials trades at $310 per share, equating to a forward P/E of 33.2.

Atmus Filtration Technologies (ATMU)

Recent GAAP Operating Margin (TTM): 16.9%

After operating under Cummins for 65 years, Atmus Filtration Technologies (NYSE:ATMU) became an independent company in 2023. It specializes in manufacturing filters for trucks, construction, and agricultural equipment, focusing on reducing emissions and protecting engines.

Concerns About ATMU

- Annual revenue growth has averaged just 4.1% over the past two years, lagging behind other industrial companies.

- Gross margin stands at 26.3%, reflecting elevated production costs.

- Free cash flow margin has declined by 3.4 percentage points over the past five years, suggesting the business has become more capital intensive amid rising competition.

Atmus Filtration Technologies is currently valued at $64.53 per share, with a forward P/E of 21.8.

Top-Quality Stocks for Any Market Environment

WHILE YOU’RE HERE: Discover 9 Elite Market-Beating Stocks. The best-performing stocks consistently outperform the market, driven by robust sales growth, expanding free cash flow, and exceptional returns on capital. These companies have already been recognized by the market for their excellence.

Our AI-driven platform believes these winning streaks aren’t over yet. See which nine stocks made our list this week—absolutely free.

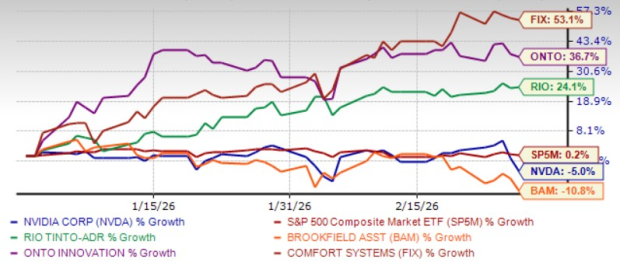

Past selections include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, and lesser-known companies such as Comfort Systems, which delivered a 782% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

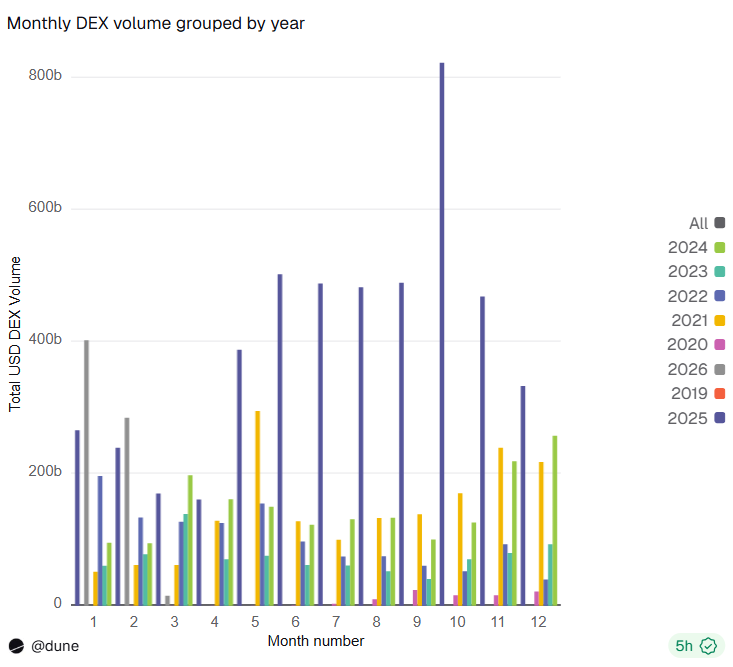

DEX volumes post best February performance since 2020

5 High-Growth Stocks Worth Considering in March Following a Turbulent February