BJ's Wholesale Set to Report Q4 Results: Will They Surpass Expectations Again?

BJ's Wholesale Club Holdings: Q4 Earnings Preview

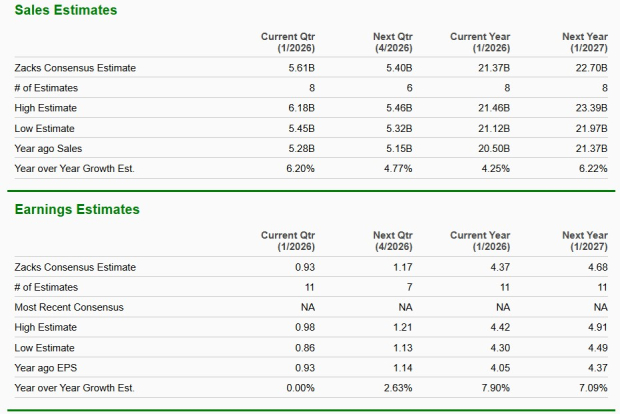

BJ's Wholesale Club Holdings, Inc. is expected to report higher revenue for its fiscal fourth quarter of 2025, with results scheduled for March 5 before the market opens. Current analyst projections suggest revenues will reach $5.61 billion, representing a 6.2% increase compared to the same period last year.

Over the past week, the consensus estimate for quarterly earnings per share has edged up to $0.93, indicating performance in line with the previous year. Historically, BJ's has outperformed expectations, delivering an average earnings surprise of 10.3% over the last four quarters. In the most recent quarter, the company exceeded analyst forecasts by 5.5%.

Image Source: Zacks Investment Research

Key Drivers for BJ’s Upcoming Results

BJ's Wholesale Club continues to benefit from its membership-based approach, which fosters steady revenue through strong member engagement, growth in premium memberships, and high renewal rates. These factors help support both store traffic and merchandise sales, especially as consumers become more value-conscious in uncertain economic times.

The company’s focus on value, expansion through new locations, and improvements in product selection and inventory levels are expected to keep demand robust in essential categories like groceries and perishables. Initiatives such as Fresh 2.0, along with competitive pricing and enhanced merchandising, have strengthened BJ’s position in fresh food segments. Comparable club sales for merchandise are projected to rise by 2% for the quarter.

Digital innovation has also played a role in driving growth, with increased adoption of same-day services, in-store fulfillment, and mobile shopping options. Members who engage digitally tend to spend more and visit more often. BJ’s efforts to improve convenience—through pickup, delivery, and app-based checkout—are likely to have further boosted traffic and comparable sales.

However, higher selling, general, and administrative (SG&A) expenses, particularly those related to labor, marketing, and costs from opening new clubs, may have put some pressure on profit margins. SG&A expenses are expected to rise by 5.6% year over year, which could result in a slight decline in operating margin by 0.1 percentage points.

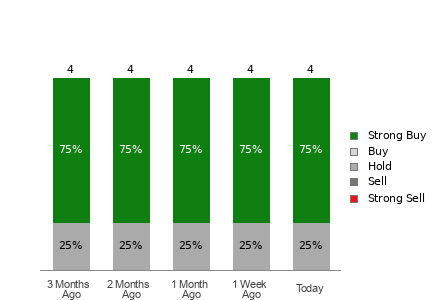

Analyst Outlook: Will BJ Beat Expectations?

As the earnings announcement approaches, investors are watching to see if BJ’s will once again surpass analyst estimates. The combination of a positive Earnings ESP (Expected Surprise Prediction) and a favorable Zacks Rank (currently #2, Buy) suggests a strong likelihood of an earnings beat this quarter. BJ’s currently holds an Earnings ESP of +5.69%.

For those interested in identifying stocks with the potential to outperform, Zacks provides tools such as the Earnings ESP Filter and regularly updates its list of top-ranked stocks.

BJ's Wholesale Club Holdings: Price, Consensus, and EPS Surprise

BJ Stock Performance Compared to Peers

Over the past three months, BJ’s Wholesale Club shares have gained 7.3%, trailing the broader food and natural foods products industry, which rose 13.4% during the same period. While BJ’s has outperformed Albertsons Companies, Inc., it has lagged behind Walmart Inc. and Costco Wholesale Corporation. Specifically, Walmart and Costco shares increased by 11.8% and 9.6%, respectively, while Albertsons saw a slight decline of 0.2%.

Image Source: Zacks Investment Research

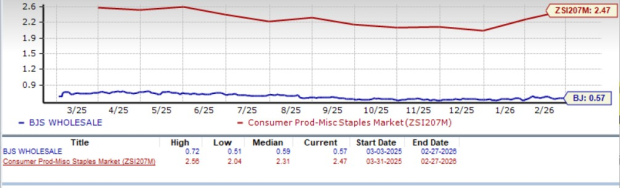

Is BJ a Value Opportunity?

Despite its recent share price gains, BJ’s Wholesale Club remains attractively valued compared to its industry peers. The company is trading at a forward 12-month price-to-sales (P/S) ratio of 0.57, well below the industry average of 2.47 and slightly under its own 12-month median P/S of 0.59. While BJ’s trades at a premium to Albertsons (P/S of 0.11), it is still at a discount relative to Walmart (1.36) and Costco (1.46).

Image Source: Zacks Investment Research

Conclusion: BJ’s Outlook Ahead of Earnings

Heading into its fourth-quarter report, BJ’s Wholesale Club appears to be on solid footing, supported by strong membership trends, consistent sales growth, and ongoing digital initiatives. While rising operating costs could impact margins, the company’s focus on value and effective execution position it well against competitors. Current shareholders may consider holding their positions, while new investors might look for opportunities around the earnings release.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Company Updates on March 2, 2026

Wall Street Investors Show Confidence in Broadwind Energy (BWEN): Is It Time to Invest?

United Therapeutics' Trial Shows 55% Drop in Lung Disease Worsening

War Premium Is Back: Energy & Oil ETFs Rip Higher On Middle East Supply Shock