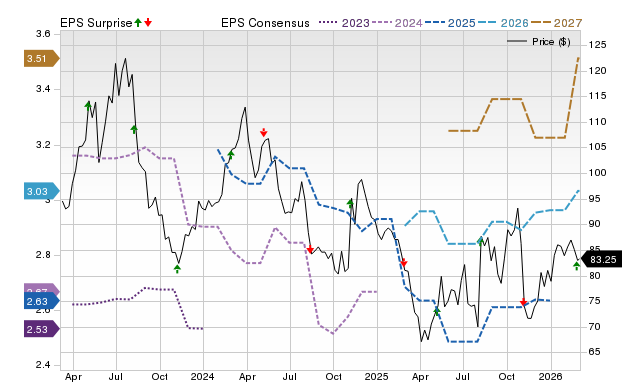

WBD Q4 Results Fall Short Due to Drop in Linear TV and Underperforming Studios

Warner Bros. Discovery Q4 2025 Financial Overview

Warner Bros. Discovery (WBD) posted a net loss of $0.10 per share for the fourth quarter of 2025, falling short of the Zacks Consensus Estimate, which anticipated earnings of $0.02 per share. However, this loss was an improvement compared to the $0.20 per share deficit reported in the same quarter last year.

Total revenue for the quarter reached $9.46 billion, representing a 6% decrease from the previous year and missing analyst expectations by 0.04%. The company closed the quarter with 131.6 million streaming subscribers worldwide, marking an increase of 3.5 million from the third quarter and a significant rise from 116.9 million subscribers a year earlier.

Streaming Segment Delivers Subscriber and Revenue Growth

The streaming division saw notable progress, with global subscribers climbing to 131.6 million—up by 3.5 million compared to the prior quarter. Streaming revenue grew 4% (excluding currency effects) to $2.79 billion, surpassing the consensus estimate by 2.55%.

Distribution revenue advanced 2% (ex-FX), fueled by a 13% jump in subscribers, largely due to HBO Max's ongoing global expansion and new distribution partnerships. This growth was partially offset by a renewed domestic distribution agreement with a former affiliate, previously disclosed in Q2 2025.

Advertising revenue surged 17% (ex-FX) to $278 million, driven by an increase in ad-lite subscribers. However, the absence of NBA content reduced year-over-year growth by 3% (ex-FX).

Adjusted EBITDA for streaming dropped 7% (ex-FX) to $393 million, but still exceeded expectations by 9.56%. Despite higher content and marketing expenses to support HBO Max's global rollout, the company managed to outperform profitability forecasts.

Challenges in Linear Networks and Studios

Traditional business segments faced considerable obstacles during the quarter. Global Linear Networks revenue declined 13% (ex-FX) to $4.20 billion, though this was 4.34% above analyst projections.

Distribution revenue fell 8% (ex-FX), mainly due to a 10% reduction in domestic linear pay TV subscribers, offset slightly by a 3% increase in affiliate rates. Advertising revenue dropped 14% (ex-FX) to $1.44 billion, impacted by a 22% decrease in domestic viewership and the lack of NBA programming, which alone contributed to a 4% decline (ex-FX).

Adjusted EBITDA for Global Linear Networks plunged 27% (ex-FX) to $1.41 billion, still beating estimates by 3.92%. This sharp drop highlights the ongoing structural challenges facing traditional linear television.

Studio revenues decreased 14% (ex-FX) to $3.18 billion, missing consensus by 6.9%. Content revenue fell 16% (ex-FX), with theatrical revenue down 11% (ex-FX) due to no new releases, TV revenue declined 18% (ex-FX) because of timing in content renewals, and games revenue dropped 34% (ex-FX).

Studios Adjusted EBITDA fell 27% (ex-FX) to $728 million, missing analyst expectations by 0.67%.

Stock Ratings and Alternatives

Warner Bros. Discovery currently holds a Zacks Rank #3 (Hold).

Within the broader Consumer Discretionary sector, several stocks have stronger ratings:

- Sonos (SONO) – Zacks Rank #1 (Strong Buy)

- Carter’s (CRI) – Zacks Rank #1 (Strong Buy)

- Roku (ROKU) – Zacks Rank #1 (Strong Buy)

- Sonos shares have risen 9.4% over the past six months. The consensus estimate for the upcoming quarter is a loss of $0.04 per share, reflecting a 77.78% improvement year-over-year.

- Carter’s shares are up 17.2% in the last six months. The expected EPS for the next quarter is $1.70, indicating a 28.87% decrease compared to last year.

- Roku shares have dipped 0.1% over the past six months. The consensus estimate for the next quarter’s EPS is $0.34 per share, representing a 278.95% year-over-year increase.

Top 5 Stocks with Potential to Double

Zacks analysts have identified five stocks with the potential to gain 100% or more in the coming months:

- Stock #1: A disruptive company showing strong growth and resilience

- Stock #2: Bullish signals suggest buying during market dips

- Stock #3: Among the most attractive investment opportunities currently available

- Stock #4: Leading player in a rapidly expanding industry

- Stock #5: Innovative omni-channel platform ready for expansion

Many of these picks are not widely followed on Wall Street, offering early investors a unique opportunity. Previous recommendations have achieved gains of +171%, +209%, and +232%.

Additional Resources and Reports

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

CI&T Inc. (CINT) Anticipates Earnings Increase: Key Information Before Next Week’s Report

Wall Street experts predict that Globale Online (GLBE) may surge by 41.22%: Strategies for Trading

Wall Street experts predict that U.S. Physical Therapy (USPH) may surge by 26.52%: Strategies for Trading