The Walt Disney Company (DIS) Is Gaining Attention: Key Information to Consider Before Investing

Walt Disney (DIS): Key Insights for Investors

Walt Disney (DIS) has recently garnered significant attention among investors. To better understand its short-term prospects, let's examine several important factors that could influence its stock performance.

Recent Stock Performance

In the past month, Disney's shares have declined by 6%. This compares to a 1.3% drop in the Zacks S&P 500 composite index and a 2% decrease in the broader media conglomerates sector, which includes Disney. The main question for investors is: where might Disney's stock head next?

Market Trends vs. Fundamentals

While news or speculation about major changes in a company's outlook can cause immediate price swings, long-term investment decisions are ultimately shaped by fundamental factors.

Earnings Forecast Adjustments

At Zacks, the primary focus is on changes in earnings forecasts, as these projections help determine a stock's intrinsic value. Analysts frequently update their earnings estimates to reflect new business developments. When these estimates rise, the stock's fair value increases, often attracting buyers and pushing the price higher. Research consistently shows a strong link between earnings estimate revisions and short-term stock price movements.

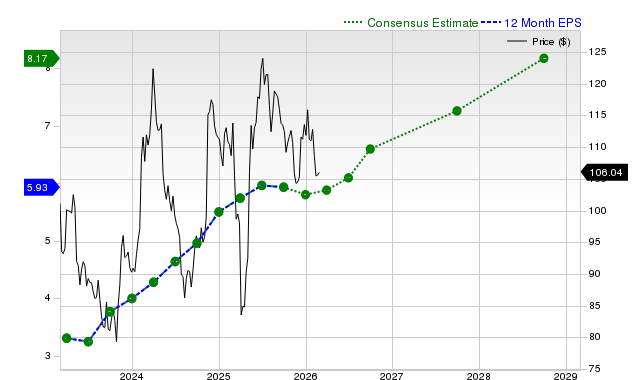

- For the current quarter, Disney is expected to earn $1.53 per share, up 5.5% from the same period last year. However, the consensus estimate has decreased by 6.1% in the past month.

- The full-year earnings estimate stands at $6.59 per share, representing an 11.1% increase year-over-year, with a slight 0.2% uptick in the last 30 days.

- Looking ahead to next fiscal year, the estimate is $7.25 per share, up 10.1% from the prior year, though this forecast has dipped by 0.8% over the past month.

Zacks Rank, a proprietary rating system with a proven track record, leverages these earnings estimate changes to predict near-term stock direction. Based on recent estimate shifts and other related factors, Disney currently holds a Zacks Rank #3 (Hold).

Forward EPS Estimate Trend

Revenue Growth Outlook

While earnings growth is a strong indicator of financial health, sustained revenue increases are essential for long-term profitability. Understanding Disney's revenue projections provides valuable context:

- Current quarter sales are expected to reach $25.07 billion, up 6.2% year-over-year.

- For the current fiscal year, projected revenue is $101.04 billion, a 7% increase.

- Next fiscal year estimates are $106 billion, up 4.9% from the previous year.

Recent Results and Earnings Surprises

In its most recent quarter, Disney reported $25.98 billion in revenue, a 5.2% increase from the prior year. Earnings per share came in at $1.63, compared to $1.76 a year earlier.

- Revenue was slightly below the consensus estimate by 0.03%.

- EPS exceeded expectations by 3.82%.

- Disney has outperformed consensus EPS estimates in each of the last four quarters, but has only surpassed revenue forecasts once during this period.

Stock Valuation

Evaluating a stock's valuation is crucial for making informed investment choices. Comparing Disney's current valuation metrics—such as price-to-earnings, price-to-sales, and price-to-cash flow—to its historical averages and those of its peers helps determine whether the stock is fairly priced.

The Zacks Value Style Score, which assesses both traditional and alternative valuation measures, ranks stocks from A to F. Disney currently receives a B, suggesting it trades at a discount relative to similar companies.

Summary

The information presented here, along with additional resources on Zacks.com, can help investors decide whether to pay attention to the current market buzz surrounding Disney. With a Zacks Rank #3, Disney is expected to perform in line with the broader market in the near term.

5 Stocks Poised to Double

Zacks experts have identified five stocks with the potential to gain 100% or more in the coming months:

- Stock #1: A disruptive company showing strong growth and resilience

- Stock #2: Bullish signals suggest buying on recent dips

- Stock #3: One of the most attractive investment opportunities available

- Stock #4: Leading a rapidly expanding industry

- Stock #5: An innovative omni-channel platform ready for expansion

Many of these picks are not widely followed by Wall Street, offering unique opportunities for early investors. Previous recommendations have achieved gains of 171%, 209%, and 232%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

MU Falls 8% While PLTR Rises 1.4%: Different Drivers, Distinct Outcomes

Asian markets decline as South Korea’s KOSPI drops more than 10%

DXY: Caution near 100 as rally looks stretched – DBS