Disney (DIS): Should You Purchase, Sell, or Retain After Q4 Results?

Disney’s Recent Stock Performance: A Closer Look

In the past half-year, Disney’s stock price has dropped to $105.50, resulting in a 10.8% decline. This stands in sharp contrast to the S&P 500, which saw a 7.7% increase during the same period. Such results may leave investors questioning their next move.

Should you consider investing in Disney, or is it a potential threat to your portfolio?

Reasons We Expect Disney to Underperform

Despite the lower share price, we remain wary of Disney’s prospects. Here are three key factors behind our lack of enthusiasm for DIS, along with a stock we prefer.

1. Lackluster Long-Term Sales Growth

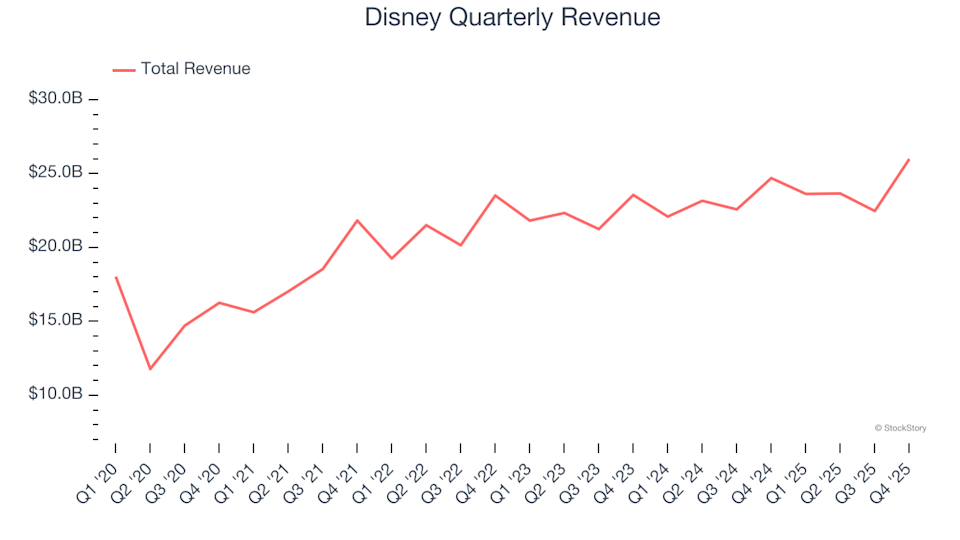

Consistent revenue growth is a hallmark of high-quality companies. While any business can have a strong quarter, sustained expansion is what sets leaders apart. Over the past five years, Disney’s annualized revenue growth was just 9.5%, falling short of industry standards for consumer discretionary stocks.

Disney Quarterly Revenue

2. Subpar Operating Margin Raises Concerns

Operating margin reflects how much profit remains after covering core expenses, such as production costs, marketing, and salaries. It’s a useful metric for comparing profitability across companies, as it excludes interest and taxes. Disney’s operating margin has hovered around 14.8% over the past two years, showing little improvement. This figure is below expectations for consumer discretionary firms and points to inefficiencies in its cost structure.

Disney Trailing 12-Month Operating Margin (GAAP)

3. Unimpressive Free Cash Flow Margin Limits Growth

Free cash flow is a valuable indicator because it accounts for all operational and capital expenditures, making it difficult to manipulate. Over the last two years, Disney’s free cash flow margin averaged only 8.2%, which is considered weak for its sector. This limits the company’s ability to reinvest or return capital to shareholders.

Disney Trailing 12-Month Free Cash Flow Margin

Our Verdict

While we support businesses that serve everyday consumers, Disney’s recent performance leaves us unconvinced. The stock currently trades at a forward P/E of 15.1 (or $105.50 per share), which is reasonable, but we see stronger opportunities elsewhere. For those seeking alternatives, consider one of our top digital advertising recommendations.

Better Investment Options Than Disney

Don’t Miss: Our Top 6 Stocks This Week

The market is quickly distinguishing between high-quality and overpriced stocks. With AI reshaping entire industries overnight, you need more than just a list of solid companies to stay ahead.

Our AI-driven system identified Palantir before its 1,662% surge, AppLovin before its 753% rise, and Nvidia ahead of its 1,178% jump. Every week, it highlights six new stocks that meet rigorous criteria.

Past selections include well-known names like Nvidia (+1,326% from June 2020 to June 2025) and lesser-known companies such as Tecnoglass, which delivered a 1,754% five-year return. Find your next standout investment with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Freshworks Unifies Global Sales Organization to Accelerate Growth

Vizsla confirms two more deaths in Mexico kidnappings