3 Factors That Make PVH a Risky Choice and One Alternative Stock Worth Considering

Painful Six Months for PVH Investors

PVH shareholders have endured a challenging half-year, with the stock tumbling 20.4% to its current price of $68.41. This sharp decline has left many investors unsettled and questioning their next move.

Is PVH now a bargain worth considering, or does it pose a threat to your investment portfolio?

Why We Expect PVH to Lag Behind

Despite the recent drop in share price, we remain cautious about PVH. Here are three key reasons we believe there are more attractive alternatives in the market, along with a stock we prefer.

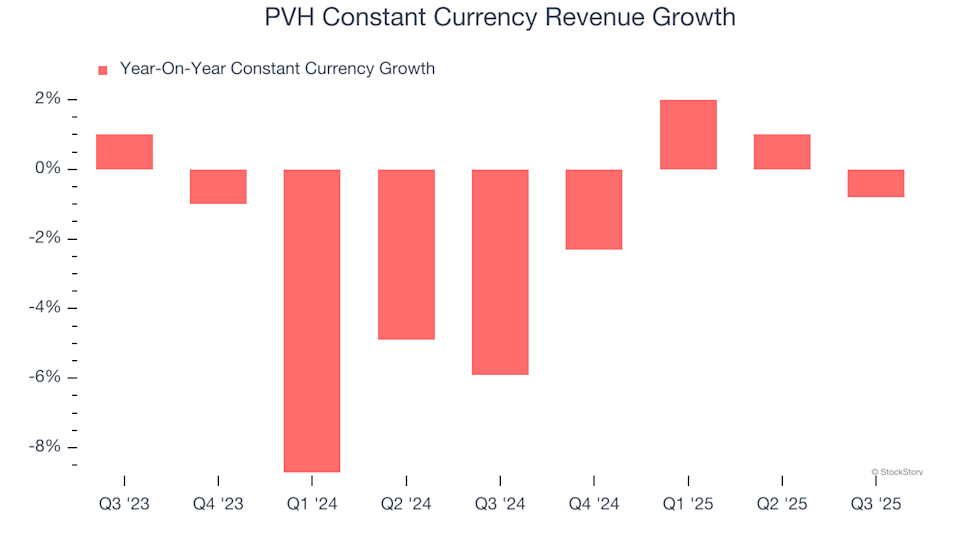

1. Weak Constant Currency Revenue Signals Softening Demand

To truly gauge the performance of companies in the apparel and accessories sector, it's important to look at constant currency revenue, which strips out the effects of currency fluctuations and reveals genuine demand trends.

PVH’s constant currency revenue has declined by an average of 2.6% annually over the past two years. This lackluster performance hints at intensifying competition or a saturated market. It also indicates that PVH may need to cut prices or invest more in product innovation to reignite growth—moves that could pressure short-term profits.

2. Subpar Free Cash Flow Margin Restricts Growth Options

Free cash flow, though often overlooked in earnings reports, is a crucial measure because it accounts for all operating and capital expenditures, making it a reliable indicator of financial health. Ultimately, cash flow is what matters most.

Over the last two years, PVH has struggled to generate strong cash profits, with an average free cash flow margin of just 6.6%—a disappointing figure for a consumer discretionary company. This limits the company’s ability to reinvest or reward shareholders.

3. Declining ROIC Shows Investments Aren’t Paying Off

We favor companies that consistently deliver high returns on invested capital (ROIC), but the direction of this metric is just as important as the level. PVH’s ROIC has dropped by an average of 1.2 percentage points each year recently, compounding its already modest returns. This trend suggests that lucrative growth opportunities are scarce for the company.

Our Verdict

While we appreciate businesses that serve consumers, PVH doesn’t make the cut for us. After its recent slide, the stock trades at a seemingly low 6× forward P/E (or $68.41 per share), but the underlying fundamentals remain shaky, exposing investors to significant downside risk. There are better opportunities available. For example, consider one of our top picks in software and edge computing.

Stocks We Prefer Over PVH

ALSO RECOMMENDED: Top 5 Momentum Stocks. The ideal time to invest in a standout stock is when the market starts to recognize its potential. These companies not only boast strong fundamentals but are also experiencing positive momentum right now.

Discover which stocks our AI-driven platform is highlighting this week. Explore the latest Strong Momentum stocks—completely free.

Our list features well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known success stories such as Kadant, which delivered a 351% return over five years. Start your search for the next big winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

APPLE formed the worst Bearish Cross that can crash it to $205

Surpassing FTX-Era Lows: 38% Of Altcoins Hit Record Lows As Liquidity Abandons The Crypto Fringe

ICB Network and Mokoko AI Entail Strategic Partnership to Transform Web3 Gaming Infrastructure