3 Key Motives to Offload WOOF and One Alternative Stock Worth Purchasing

Petco’s Recent Stock Performance: A Closer Look

Over the past half-year, Petco’s share price has dropped significantly, losing nearly 30% of its value and now trading at $2.54 per share. This sharp decline may leave investors questioning their next steps.

Should you consider adding Petco to your portfolio, or does it pose unnecessary risk?

Why We’re Cautious About Petco

Although Petco’s shares are now more affordable, we remain wary. Below are three reasons we’re steering clear of WOOF, along with a stock we prefer instead.

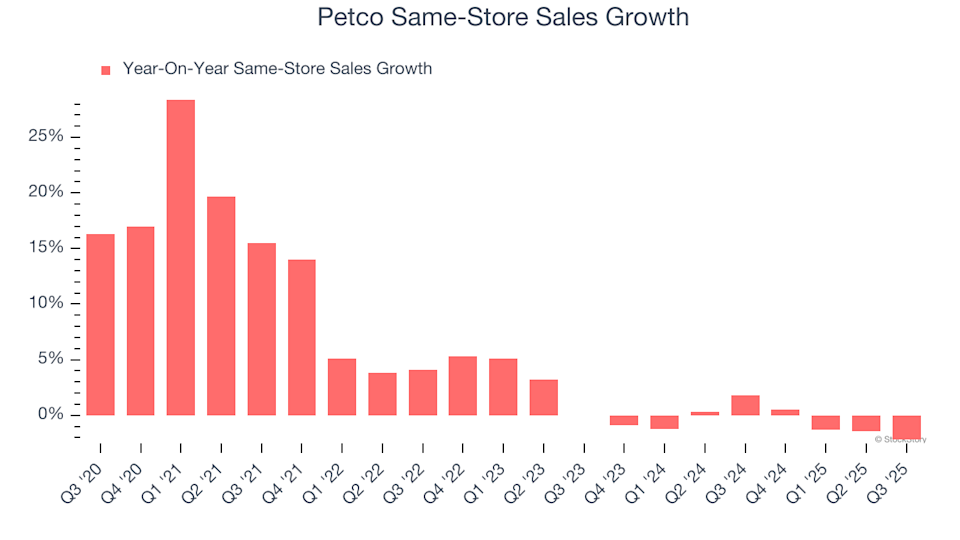

1. Stagnant Same-Store Sales Reflect Weak Consumer Interest

Same-store sales are a crucial metric for assessing organic growth in established retail locations. Over the past two years, Petco’s same-store sales have shown little to no growth, signaling tepid demand at its existing stores.

Petco Same-Store Sales Growth

2. Declining Earnings Per Share

Tracking long-term trends in earnings per share (EPS) helps determine if a company’s additional sales are translating into real profit. Sometimes, revenue can be artificially boosted by heavy spending on marketing or promotions.

Unfortunately for Petco, its EPS has fallen by an average of 42% each year over the past three years, while revenue has remained flat. This suggests the company’s fixed costs have made it difficult to adapt to inconsistent demand, hurting profitability.

Petco Trailing 12-Month EPS (Non-GAAP)

3. Elevated Debt Poses Financial Risk

While debt can enhance returns, excessive borrowing increases vulnerability. As long-term investors, we prefer to avoid companies that are highly leveraged, as this can lead to financial distress.

Petco currently holds $2.97 billion in debt, far outweighing its $237.4 million in cash. Its net-debt-to-EBITDA ratio stands at 7× (based on $398 million in EBITDA over the past year), indicating a heavy debt burden.

Petco Net Debt Position

With this level of debt, borrowing further becomes more costly, and credit ratings could be downgraded if profits decline. Should market conditions deteriorate, Petco could find itself in a precarious position—something we aim to avoid when investing in quality businesses.

We remain hopeful that Petco can strengthen its balance sheet, but we advise caution until the company either boosts profitability or reduces its debt load.

Our Verdict

Petco does not meet our standards for a high-quality investment. After its recent drop, the stock is valued at 11.2× forward P/E (or $2.54 per share). This price suggests that much optimism is already factored in, and better opportunities exist elsewhere. We suggest considering a reliable industrials company benefiting from ongoing upgrades instead.

Top Stocks for Any Market Environment

Don’t Miss: This Week’s Top 6 Stock Picks. The current market is quickly distinguishing quality companies from overpriced ones, with AI-driven shifts impacting entire sectors. In such a fast-moving environment, you need more than just a list of solid businesses.

Our AI system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Each week, it highlights six new stocks that meet our rigorous criteria.

Our selections have included well-known names like Nvidia (+1,326% from June 2020 to June 2025) and lesser-known companies such as Comfort Systems, which delivered a 782% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold price to accelerate and hit new record highs after this event – technical analyst

Crypto Market Sees Slight Recovery Amid Growing War-Led Tensions

Gold price to accelerate and hit new record highs after this event – technical analyst