3 Reasons Why SNDR Carries Risks and One Alternative Stock Worth Considering

Schneider’s Recent Performance: A Closer Look

In the last half-year, Schneider’s stock has delivered strong returns, outpacing the S&P 500 by 8.4%. The share price has reached $28.35, marking a robust 16.1% gain. With this impressive rally, investors may be wondering what their next step should be.

Is it wise to add Schneider to your holdings now, or is caution warranted?

Why We’re Hesitant on Schneider

Despite recent gains, we remain reserved about Schneider’s prospects. Below are three key reasons we believe SNDR may not be the best choice right now, along with an alternative we prefer.

1. Weak Long-Term Revenue Growth

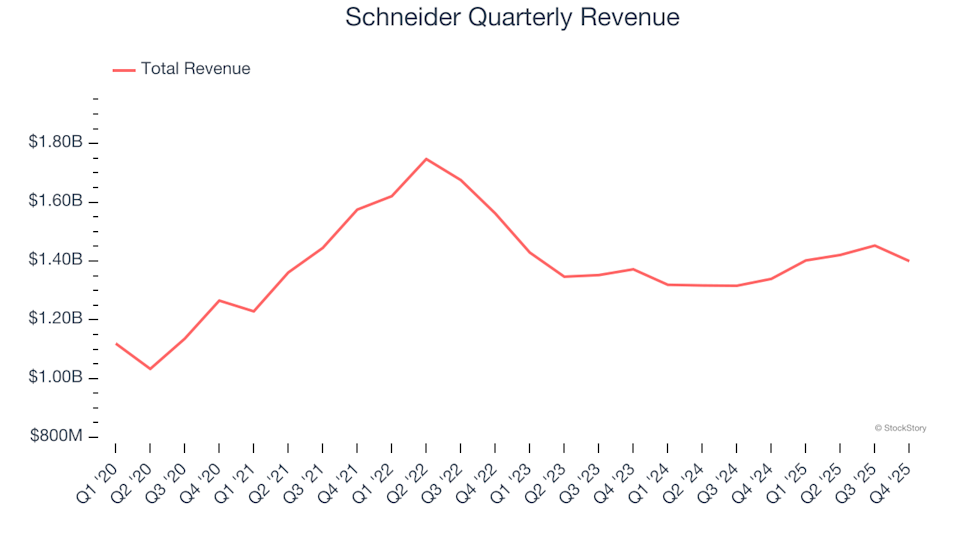

Evaluating a company’s sales trajectory over several years can reveal its true strength. While short-term spikes are possible for any business, sustained growth is a hallmark of quality. Unfortunately, Schneider’s revenue has only grown at a modest 4.5% compound annual rate over the past five years, falling short of what we expect from leaders in the industrial sector.

2. Declining Earnings Per Share

Long-term trends in earnings per share (EPS) indicate whether a company’s additional sales are translating into real profits. Sometimes, revenue growth is driven by heavy spending rather than operational efficiency.

For Schneider, EPS has dropped by an average of 13.1% annually over the last five years, even as revenue increased by 4.5%. This suggests that the company’s profitability per share has eroded during its expansion.

3. Diminishing Returns on New Investments

Return on invested capital (ROIC) measures how effectively a company turns its funding—both debt and equity—into operating profit.

We favor companies that consistently generate high returns, but the direction of ROIC is just as important. Schneider’s ROIC has fallen sharply in recent years. While management has made solid decisions in the past, this downward trend could signal a lack of lucrative growth opportunities going forward.

Our Verdict

Schneider does not meet our standards for quality at this time. Although the stock has recently outperformed the market, it now trades at a forward price-to-earnings ratio of 33.3 (or $28.35 per share), reflecting high expectations. We believe there are other companies with stronger fundamentals right now. For example, consider the world’s leading software company.

Better Opportunities Than Schneider

Don’t Miss: This Week’s Top 6 Stocks. The current market environment is quickly distinguishing high-quality stocks from overpriced ones. With AI rapidly reshaping entire industries, you need more than just a list of solid companies to stay ahead.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Each week, it highlights six new stocks that meet our rigorous criteria.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which delivered a 351% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

W.W. Grainger (GWW) Reports 2025 Sales of $17.9B, Adjusted EPS of $39.48

Sezzle (SEZL) Reports 2025 Revenue Growth of 66.1%, Record $133.1M Net Income

On Holding (ONON) Reports 2025 Net Sales of CHF 3.0B and 30% YoY Growth