Should you consider purchasing, keeping, or selling Macy's shares ahead of the Q4 earnings report?

Macy's Q4 2025 Earnings Preview: What Investors Need to Know

Macy's, Inc. is set to announce its fourth-quarter fiscal 2025 results on March 5, before the market opens. Investors are weighing whether now is the right time to buy shares or maintain their current holdings ahead of this key report.

While Macy's continues to push forward with its Bold New Chapter initiative—emphasizing luxury offerings, optimizing its store footprint, and maintaining strict cost controls—the company still faces headwinds. These include tariff-related pressures, store closures, softness in certain product categories, and broader economic challenges. Given these dynamics, it's important to assess the main factors that could impact Macy's upcoming results and whether the stock presents a compelling opportunity at this juncture.

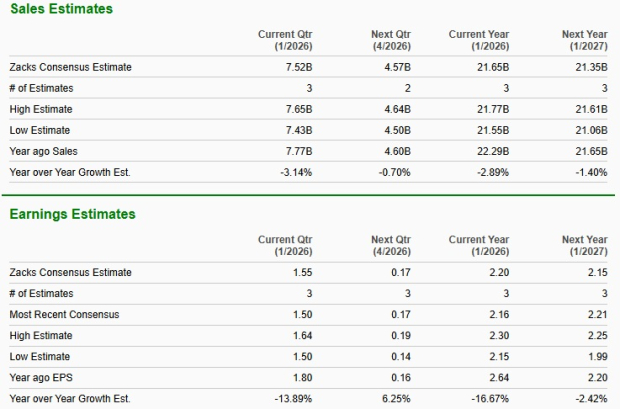

Analysts currently expect Macy's to report fourth-quarter revenue of $7.52 billion, which would represent a 3.1% decrease compared to the same period last year. Earnings per share are projected to come in at $1.55, unchanged over the past month, but down 13.9% year over year.

Historically, Macy's has delivered significant earnings surprises, with an average beat of 78.9% over the last four quarters. In the most recent quarter, the company exceeded expectations by a remarkable 169.2%.

Image Source: Zacks Investment Research

Will Macy's Beat Q4 Earnings Expectations?

As the earnings release approaches, investors are eager to know if Macy's will surpass estimates. According to predictive models, there is no clear indication that Macy's will deliver an earnings beat this quarter. Typically, a positive Earnings ESP combined with a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) increases the likelihood of an earnings beat. However, Macy's currently holds a Zacks Rank #4 (Sell) and an Earnings ESP of 0.00%, which does not suggest an outperformance this time.

For those seeking top stock picks ahead of earnings, tools like the Earnings ESP Filter can help identify potential winners.

Macy's, Inc. Price, Consensus, and EPS Surprise

Key Drivers and Challenges for Macy's Q4 Results

Macy’s fourth-quarter performance is expected to reflect continued momentum from its Bold New Chapter strategy, especially in its core store network and digital operations. In the previous quarter, the company saw improved comparable sales thanks to better omnichannel execution, enhanced brand selection, and more focused product assortments. Management noted strong customer engagement with these changes.

The company’s Reimagine 125 locations outperformed the rest of the store fleet, benefiting from improved presentation, a better in-store experience, and tailored merchandising. These operational upgrades likely helped boost store traffic, conversion rates, and average transaction size during the crucial holiday period.

Luxury divisions also played a significant role. Bloomingdale’s posted robust comparable sales growth, driven by brand expansion and strong demand in categories like ready-to-wear, men’s apparel, and fine jewelry. Bluemercury continued its positive trend, supported by strong performance in skincare and premium beauty partnerships. If these trends persisted through the holiday season, Macy’s higher-end formats may have helped offset weaker demand in value-focused categories and captured more gifting-related sales.

Operational enhancements, such as the opening of the China Grove distribution center with advanced automation and robotics, likely improved supply chain efficiency, delivery speed, and cost management. Better fulfillment capabilities, disciplined inventory management, and a well-balanced product mix for the holidays may have reduced the risk of markdowns and improved stock availability.

Additionally, a more stable credit card portfolio and increased applications in the third quarter signaled healthier customer engagement, which could have supported holiday spending.

However, several challenges likely weighed on year-over-year results. Tariffs continued to pressure merchandise margins, despite mitigation efforts. Elevated promotional activity and ongoing store closures also created headwinds for revenue growth. As a result, comparable sales are expected to decline by 1.6% on an owned basis and 1.5% when including licensed and marketplace sales. Gross margin is projected to fall by 90 basis points to 34.8% for the quarter.

How Does Macy's Valuation Stack Up?

From a valuation perspective, Macy's shares are trading at a notable discount compared to the broader Retail - Regional Department Stores industry. With a forward 12-month price-to-earnings (P/E) ratio of 9.23, Macy's is well below the industry average of 13.57, suggesting the stock may be undervalued at current prices.

Image Source: Zacks Investment Research

When compared to major retail peers, Macy's valuation appears even more attractive. Costco trades at a forward P/E of 47.73, Walmart at 44.10, and Ross Stores at 28.58—all significantly higher than Macy's multiple.

Macy's Stock Performance in Context

Over the last six months, Macy's stock has climbed 23.7%, outpacing the industry average growth of 15.2%. In contrast, the broader Retail-Wholesale sector declined by 0.6%, while the S&P 500 returned 8.8% during the same period.

Image Source: Zacks Investment Research

Despite this strong performance, Macy's lagged behind some key competitors: Walmart gained 28.9%, Ross Stores surged 37.1%, and Costco returned 6.7% over the same timeframe.

Image Source: Zacks Investment Research

Should You Consider Macy's Before Q4 Earnings?

As Macy’s prepares to release its fourth-quarter results, the company continues to face more challenges than tailwinds. While the Bold New Chapter strategy has driven some operational improvements, persistent macroeconomic headwinds, aggressive promotions, and ongoing store closures have likely limited the benefits. Margin pressure from tariffs and discounting is expected to remain a concern, potentially weighing on profitability despite strategic progress.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Altcoins Facing Major Liquidation Risks in the First Week of March

Solana Price Sets Up for a 5% Bounce — Here Is How It Could Turn Into a Rally

World War III Scenario: Which Crypto Would Suffer the Most? (4 AIs Respond)

American Eagle Set to Report Q4 Earnings: What's in the Offing?