A historic piece of legislation that could dramatically reshape the taxation of cryptocurrencies in Turkey was presented to the parliamentary committee today. First discussed in 2021 and shelved for a period, the bill is now poised to take effect, potentially bringing the country’s crypto markets under some of the world’s most comprehensive regulation. The new law introduces multiple tax rates—0.03%, 10%, and up to 40%—that have caused confusion among market participants, but a closer look clarifies how each will apply to investors and exchanges.

0.03% Transaction Tax

This nominal tax will be paid by cryptocurrency exchanges operating in Turkey, and it is expected that many platforms will absorb the cost, using it as a marketing or competitive advantage. For a transaction of 10,000 Turkish lira on a domestic exchange—whether buying, selling, or transferring cryptocurrencies—the associated transaction tax would amount to just 3 lira.

Individual investors will not need to take any additional steps concerning this transaction tax. With exchanges most likely handling the payments directly, the burden on users will likely be minimal to nonexistent, and some exchanges may even choose to highlight their coverage of the fee in their advertising.

10% Capital Gains Tax

A 10% tax will be levied on investment profits. For example, if you deposit 100,000 lira into a domestic crypto exchange, purchase Solana (SOL) with your funds, and after a quarterly assessment your portfolio has grown to 110,000 lira, you will owe tax on your 10,000 lira profit. That equates to a 1,000 lira tax bill.

This is regarded as the final taxation, after which investors are free to withdraw their funds to their bank accounts without further concern. However, questions arise when users trade on international exchanges. If you transfer funds from a Turkish exchange to an overseas platform, trade there, and then bring crypto back with gains, you will need to document and prove your original acquisition cost. In the draft bill:

The acquisition price shall be based on the asset owner’s declaration, provided it is supported by documentation, when transferring a crypto asset to the platform for the first time.

For purchases through decentralized finance (DeFi) platforms, the investor must submit transaction information, such as the transaction ID, to the local exchange. Similarly, if assets are acquired internationally, a detailed transaction history showing the date, currency pair, and amount must be submitted to the Turkish platform.

Local cryptocurrency exchanges in Turkey bear full responsibility for verifying this information, according to the draft:

Intermediaries in the buying and selling of crypto assets will be held liable for the required tax assessment, based on the information and documents in their possession or provided to them.

False or incomplete declarations may prompt exchanges to rapidly report suspicious cases to avoid facing penalties:

Incomplete or incorrect information causing under-reporting will result in requisite taxation and penalties on the reporter.

Notably, any quarters in which you report losses may only count as an offset against profits within the same tax year. For instance, a loss of 10,000 lira—if not recovered by year-end and properly documented—can be deducted from future gains earned in that fiscal period.

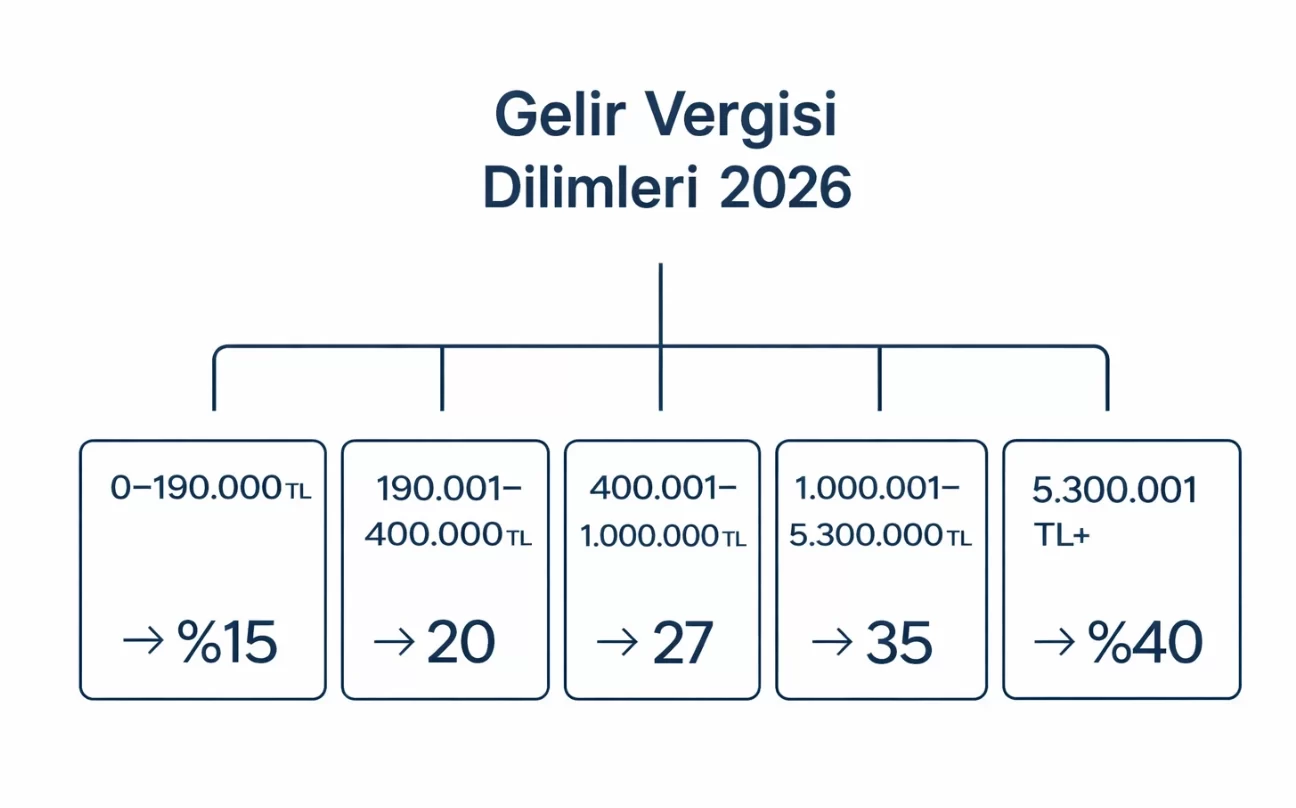

15% to 40% Income Tax Brackets

Perhaps the most critical aspect of the draft law is its treatment of various crypto income sources. While capital gains from trading are taxed a straightforward 10%, income from activities such as airdrops, staking, referral bonuses, and services paid in crypto may be taxed at much higher rates—ranging from 15% up to 40%—if acquisition costs cannot be substantiated.

Profits from airdrops, staking, payments received in crypto for services rendered, and referral incentives will be subject to income tax, calculated according to the cumulative brackets that will apply from 2026. Depending on your total annual crypto income, tax rates and fixed sum amounts will vary considerably.

For 2026, the tax rate reaches 35% for annual crypto income between 1,000,001 and 5,300,000 lira. For example, if you withdraw 100,000 lira from a global exchange, the first income bracket—at 15%—results in a tax of 15,000 lira, which increases as income grows, according to the corresponding tax bands.

Additionally, while gains subject to the 10% tax do not count toward pushing you into a higher bracket, other sources of crypto income, such as airdrops, might push you into steeper tax territory more quickly. In such cases, consulting with a tax advisor is recommended.

When Will the Law Take Effect?

The draft was presented today, but with the proximity of Ramadan and Eid al-Adha holidays, parliamentary proceedings could be delayed. Since the week of April 20-22 coincides with Ramadan Bayram, committee sessions are expected to be suspended, meaning the legislative process may not conclude in March.

The General Assembly is projected to review the proposal in April, but national holidays, including April 23, could introduce short-term delays. Although passage in the first week of May is possible, if the process is slower, the Eid al-Adha holidays between May 27-30 could push the deadline further.

The proposed law includes a clause stipulating that new crypto tax measures will come into force at the beginning of the second month following enactment.

If the legislation is passed by committee, parliament, and signed by the president in April and published in the Official Gazette, the tax regime would be implemented on June 1. Should it be finalized in May, taxes will start from July 1; if completed in June, from August 1. Accordingly, the earliest likely scenario sees enactment in June, while a more cautious estimate puts the effective date at August. Given that legislative processes in Turkey commonly take around 60 days, a July launch is also quite possible.