Intel's Value Doubles in a Year: Is Now the Right Time to Buy?

Intel's Stock Performance Surges Past Industry Peers

Over the last year, Intel Corporation (INTC) has seen its share price climb by 100.6%, outpacing the broader semiconductor industry, which posted a 51.6% increase. Intel’s gains have also exceeded those of the Zacks Computer & Technology sector and the S&P 500.

Image Source: Zacks Investment Research

Comparing Intel with NVIDIA and AMD

While Intel has delivered stronger returns than NVIDIA Corporation (NVDA), it has lagged behind Advanced Micro Devices (AMD). During the same period, AMD’s stock soared by 103.8%, whereas NVIDIA achieved a 55.3% gain.

Growth Driven by AI and Product Development

Intel’s robust performance is fueled by strong demand in its Data Center and AI division. The company reported its fastest quarter-over-quarter growth in this segment, with revenues reaching $4.7 billion—a 15% sequential increase—and an operating margin of 26.4%. This momentum is largely attributed to the popularity of its Xeon server processors, including Granite Rapids, Emerald Rapids, and Sapphire Rapids.

According to Grand View Research, the AI infrastructure market was valued at $223.45 billion in 2024 and is projected to expand at a compound annual growth rate of 30.4% through 2030. Intel’s comprehensive product lineup positions it to benefit from this rapid market expansion.

The surge in AI clusters has heightened the need for high-bandwidth interconnects, boosting Intel’s custom ASIC business. The company’s ASIC segment experienced over 50% growth in 2025, with a 26% sequential rise, and surpassed an annualized revenue run rate of $1 billion in the fourth quarter. This diversification beyond Xeon processors is a positive sign for Intel’s future.

Intel’s Client Computing Group is also seeing positive momentum, thanks to increased demand for AI-powered PCs. Shipments of AI PCs rose 16% year-over-year in the fourth quarter, and Intel’s AI chips now power more than 200 notebook models. The AI PC market is expected to expand further, driven by accelerated digital transformation across industries. Intel’s advanced Core Ultra Series 3 processors are well-positioned to capture this growth.

Additionally, Intel has entered a multi-year strategic partnership with SambaNova, a leader in AI inference platforms and hardware. This collaboration aims to deliver high-performance, cost-effective AI inference solutions built on Intel Xeon infrastructure.

Cost management and organizational streamlining have also contributed to improved profitability and cash flow. In 2025, Intel generated $9.7 billion in operating cash flow, up from $8.29 billion the previous year, and reported $2.2 billion in adjusted free cash flow for the fourth quarter.

Challenges: Intense Competition and Trade Headwinds

Intel’s Foundry division continues to weigh on overall revenue growth, with 18A ramp-up costs impacting operating margins. Despite government support, investments from NVIDIA, and management’s efforts to turn the segment around, achieving profitability remains a significant challenge.

In the AI inference space, Intel faces fierce competition from both NVIDIA and AMD. NVIDIA’s Blackwell, H200, L40S, and RTX products deliver impressive speed and efficiency for AI workloads across cloud, workstation, and data center environments. AMD’s Instinct MI350 Series GPU has set new standards for generative AI and high-performance computing in data centers. With NVIDIA’s market dominance and AMD’s strong momentum, Intel faces tough competition in both AI and commercial PC markets.

China represents more than 24% of Intel’s total revenue in 2025, making it the company’s largest market outside the United States. However, China’s efforts to replace U.S.-made chips with domestic alternatives have negatively impacted Intel’s revenue prospects in the region.

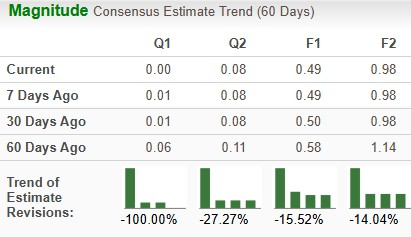

Recent Trends in Earnings Estimates

Analyst earnings forecasts for Intel in 2025 have been revised downward by 15.52% to $0.49 per share over the past two months. Projections for 2026 have also dropped by 14.04% to $0.98 per share.

Image Source: Zacks Investment Research

Intel’s Valuation Compared to Industry Peers

From a valuation perspective, Intel’s shares are trading at a price-to-book ratio of 1.8, which is significantly lower than the industry average of 26.56. This suggests that Intel is currently valued below both its peers and its historical average.

Image Source: Zacks Investment Research

Conclusion: Outlook for Intel

Intel’s growth is being propelled by strong performance in the data center sector and rising shipments of AI-enabled PCs. The expansion of AI infrastructure and increasing AI workloads are expected to drive further adoption of Xeon server processors. The company’s commitment to innovation and effective capital management should support profitability and cash flow. However, Intel continues to face stiff competition in servers, storage, commercial PCs, and networking, while downward earnings revisions reflect cautious investor sentiment. Ongoing geopolitical tensions and tariff uncertainties also pose risks. With a Zacks Rank #3 (Hold), Intel appears to be in a neutral position, and new investors may want to proceed carefully.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

PDD Shares Dip 0.88% Amid Q3 Revenue Miss $0.5B Volume Ranks 266th in Trading Activity

Best Buy's 0.61% Drop on $530M Surge in Volume (Ranked 257th) Amid Earnings Jitters and Retail Rivalry

Investment Banking and Brokerage Stocks Q4 Analysis: Comparing Raymond James (NYSE:RJF) to Competitors