Can Advancements in AI and Robust R&D Propel VEEV Forward Before Q4 Results?

Veeva Systems Set to Announce Q4 Fiscal 2026 Results

Veeva Systems (VEEV) will release its financial results for the fourth quarter of fiscal 2026 on March 4, following the market close.

In the previous quarter, Veeva reported earnings per share (EPS) of $2.04, surpassing the Zacks Consensus Estimate by 4.62%. Over the last four quarters, the company has consistently exceeded consensus EPS projections, averaging an 8.18% positive surprise.

This overview examines the main factors influencing Veeva’s performance ahead of its upcoming earnings report.

Key Considerations Before Veeva’s Earnings Release

Investors should pay close attention to trends within Veeva’s Subscription and Professional Services segments. Subscription revenue, which forms the backbone of Veeva’s business and drives its margins, continues to benefit from robust demand for R&D, Quality, and Crossix solutions. Sustained double-digit growth in this area would reinforce the strength of Veeva’s recurring revenue model. Meanwhile, Professional Services revenue, which is more variable and tied to implementation projects, is expected to reflect ongoing migrations to Vault CRM and the rollout of Development Cloud. Stable demand and improved utilization rates would signal healthy platform expansion, even if short-term hiring slightly impacts margins.

The ongoing transition to Vault CRM remains a central theme for this quarter. In the third quarter, management noted that most of the top 20 biopharma clients are moving to Vault CRM, though a few are pursuing other options. CRM now accounts for about 20% of total revenue, indicating that Veeva’s business is more diversified than in the past. Investors should watch for updates on additional migration commitments, competitive landscape, and the pace of customer transitions. Insights into revenue retention, customer win-backs, or increased cross-selling within the CRM suite will be important for evaluating the resilience of Veeva’s commercial operations.

Another area of focus is Veeva’s progress in integrating artificial intelligence across its product lines. The company has accelerated the deployment of AI agents in Commercial, Safety, Quality, and Clinical applications, aiming to boost productivity and create new revenue streams. In commercial settings, AI is expected to enhance field insights and marketing effectiveness, while in Safety and Clinical, it could streamline labor-intensive tasks like adverse event management and document review. Investors should look for early signs of customer adoption, pricing strategies, and whether AI is beginning to impact deal sizes or sales pipeline momentum. Any tangible progress here could support the view that AI will expand Veeva’s addressable market.

Growth drivers outside of CRM, such as Crossix and Development Cloud, also warrant attention. Crossix has performed strongly, benefiting from increased digital marketing spend in the pharmaceutical sector and rising demand for audience measurement and optimization tools. Continued momentum would highlight the expanding reach of Veeva’s Commercial Cloud beyond CRM.

On the R&D front, updates on Safety, eTMF leadership, and adoption of newer modules like RTSM, eCOA, and LIMS will be important. Since R&D and Quality together make up the majority of Veeva’s revenue and are generally more predictable, ongoing strength in these segments would underscore the company’s diversified growth profile as it moves into fiscal 2027.

Veeva Systems: Price and EPS Surprises

Analyst Estimates for Veeva

Analysts project that Veeva will report fourth-quarter fiscal 2026 revenue of $808.9 million, representing a 12.2% increase compared to the same period last year.

The consensus estimate for EPS stands at $1.92, which would mark a 10.3% year-over-year improvement.

What Do Analyst Models Indicate?

According to the Zacks model, stocks with a Zacks Rank of #1 (Strong Buy), #2 (Buy), or #3 (Hold) and a positive Earnings ESP are more likely to beat earnings estimates. However, this does not apply to Veeva this quarter.

- Earnings ESP: Veeva’s Earnings ESP is 0.00%.

- Zacks Rank: Veeva currently holds a Zacks Rank #4 (Sell).

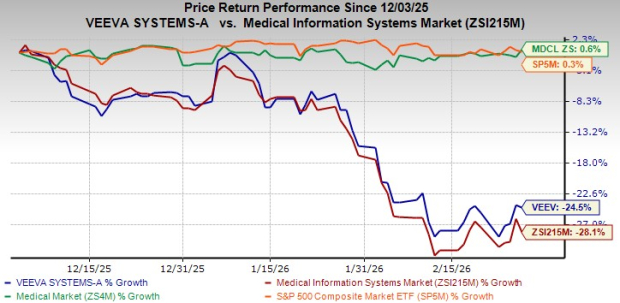

Veeva’s Recent Share Performance

In the past three months, Veeva’s stock has dropped 24.5%, underperforming the Medical Info Systems industry, which declined 28.1% during the same period.

By comparison, the S&P 500 rose 0.3% and the broader Zacks Medical sector increased 0.6% over this timeframe.

Image Source: Zacks Investment Research

Other industry peers, including IQVIA, Salesforce, and Schrodinger, have also experienced declines. IQVIA shares fell 21.4%, Salesforce lost 18.4%, and Schrodinger dropped 32.1% over the same period.

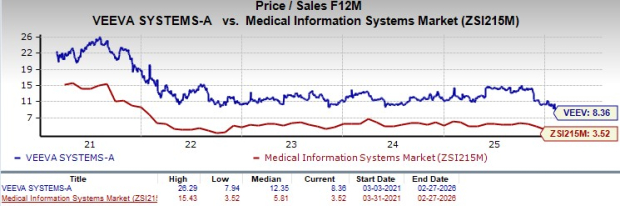

Valuation Overview

Veeva’s forward 12-month price-to-sales (P/S) ratio is 8.4, which is higher than the industry average of 3.5 but below its five-year median of 12.4.

Image Source: Zacks Investment Research

Compared to its peers, Veeva trades at a premium. IQVIA and Salesforce have P/S ratios of 1.8 and 3.9, respectively, while Schrodinger’s stands at 2.8. This suggests investors are paying a higher price for Veeva relative to its projected sales growth.

Long-Term Outlook for Veeva Systems

Veeva’s long-term prospects are underpinned by its expanding Industry Cloud strategy and a diversified revenue base. While CRM migration has attracted attention, CRM now makes up only about 20% of total revenue, with R&D, Safety, and Quality forming a larger, more stable foundation. Widespread adoption of essential products like eTMF among leading biopharma clients, along with newer offerings such as RTSM, eCOA, and LIMS, positions Veeva to capture additional market share throughout the drug development and manufacturing process. This diversification reduces dependence on any single segment and supports management’s confidence in achieving long-term goals.

Veeva’s integrated approach—combining software, data, and consulting—also provides a competitive edge. By offering a unified platform across Commercial and R&D Clouds and operating independently from Salesforce infrastructure, Veeva gains greater product control, cross-selling opportunities, and margin leverage. As life sciences companies increasingly seek comprehensive, standardized solutions, Veeva’s platform depth enhances customer loyalty and strengthens its market position.

Artificial intelligence is another significant growth driver. Veeva is embedding industry-specific AI agents into Safety, Clinical, and Commercial applications to boost efficiency, automate complex processes, and generate deeper insights. As adoption grows, AI could increase wallet share, support premium pricing, and further differentiate Veeva in regulated markets. Together, the company’s broad platform, resilient recurring revenue, and AI-driven innovation provide a solid foundation for sustained growth and profitability.

5 Stocks Poised for Significant Gains

- Stock #1: A disruptive company demonstrating strong growth and resilience

- Stock #2: Positive signals suggesting a buying opportunity

- Stock #3: Among the most attractive investments currently available

- Stock #4: A leader in a rapidly expanding industry

- Stock #5: A modern omni-channel platform ready for rapid expansion

Many of these stocks remain under the radar, offering early investors a chance to benefit from future growth. While not every pick will be a winner, previous recommendations have achieved gains of +171%, +209%, and +232%.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

NVIDIA’s Rapid S-Curve Growth: Constructing the Foundation for AI Infrastructure

How Changes in Policy and Global Geopolitical Strains Are Transforming Bitcoin Trading

Nvidia's $300 Price Target: Does Analyst Arbitrage Outweigh the Recent Stock Decline?

AERO rallies 12% as capital inflows surge: Is $0.40 within reach?