Canadian Natural to Report Q4 Earnings: What's in the Offing?

Canadian Natural Resources Limited CNQ is set to release fourth-quarter 2025 results on March 5. The Zacks Consensus Estimate for earnings is pegged at 53 cents per share on revenues of $6.6 billion.

Let us delve into the factors that might have influenced CNQ’s performance in the to-be-reported quarter. Before that, it is worth taking a look at the company’s performance in the last reported quarter.

Highlights of CNQ’s Q3 Earnings & Surprise History

In the last reported quarter, the Calgary-based oil and gas equipment and services company’s earnings beat the consensus mark, but decreased from 71 cents per share in the year-ago quarter due to lower realized oil and natural gas liquid prices and rising expenses. CNQ reported adjusted earnings per share of 62 cents, beating the Zacks Consensus Estimate of 54 cents. Total revenues of $6.9 billion beat the Zacks Consensus Estimate of $6.7 billion. The company’s earnings beat the Zacks Consensus Estimate thrice in the trailing four quarters and missed in one, delivering an average surprise of 9.3%. This is depicted in the chart below:

Canadian Natural Resources Limited Price and EPS Surprise

Canadian Natural Resources Limited price-eps-surprise | Canadian Natural Resources Limited Quote

Trend in CNQ’s Estimate Revision

The Zacks Consensus Estimate for fourth-quarter 2025 earnings has not witnessed any movement in the past 30 days. The estimated figure indicates a 19.7% year-over-year decrease. The Zacks Consensus Estimate for revenues implies a 2.2% decrease from the year-ago period.

Factors to Consider Ahead of CNQ’s Q4 Results

Canadian Natural is one of the largest independent energy companies with strong operational momentum. Record production of about 1.6 million BOE/d in the third quarter, up 19% year over year, combined with industry-leading oil sands mining costs near $21/bbl and thermal costs near $10/bbl, positions the company to generate resilient cash flow even in a moderate price environment. Recent accretive acquisitions, including additional oil sands interests and liquids-rich Duvernay and Montney assets, are already contributing incremental volumes and free cash flow. Earlier management had indicated that the company’s fourth quarter operations are tracking as expected with strong utilization, suggesting stable production into the upcoming quarter. A strong balance sheet and significant liquidity also reduce financial risk and support continued shareholder returns.

On the bearish side, earnings remain sensitive to commodity prices and heavy oil differentials, which management expects in the $10-$13/bbl range but could widen if refinery turnarounds or macro weakness emerge. AECO gas pricing remains soft, and higher 2026 turnaround activity, particularly at Horizon, could weigh on near-term volumes and costs. While production growth is robust, integration of acquisitions and sustaining higher capital spending may limit incremental margin expansion.

What Does Our Model Predict for CNQ?

Our proven Zacks model does not conclusively predict an earnings beat for CNQ this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. However, this is not the case here.

Earnings ESP of CNQ: Earnings ESP, which represents the difference between the Most Accurate Estimate and the Zacks Consensus Estimate, for this company is 0.00%.

CNQ’s Zacks Rank: CNQ currently carries a Zacks Rank #3.

Stocks to Consider

Here are some firms from the other space that you may want to consider, as these have the right combination of elements to post an earnings beat this season.

ARS Pharmaceuticals, Inc. SPRY currently has an Earnings ESP of +39.90% and a Zacks Rank of 3. SPRY is scheduled to release earnings on March 9

The Zacks Consensus Estimate for ARS Pharmaceuticals’ 2025 revenues and earnings indicates a year-over-year decline. Valued at around $917.3 million, the company’s shares have lost 8.9% in a year.

Auna SA AUNA has an Earnings ESP of +44.00% and a Zacks Rank of 2 at present. AUNA is slated to release earnings on March 10.

The Zacks Consensus Estimate for Auna’s 2025 earnings per share indicates 41.5% year-over-year growth. Valued at around $395.2 million, the company’s shares have declined 30.6% in a year.

Heritage Insurance Holdings, Inc. HRTG currently has an Earnings ESP of +24.61% and a Zacks Rank of 3. It is scheduled to release earnings on March 9.

The Zacks Consensus Estimate for Heritage Insurance Holding’s 2025 earnings per share indicates 183.1% year-over-year growth. Valued at around $861.5 million, the company’s shares have soared 138.7% in a year.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Palantir's War-Led Bounce Could Be Just The Start For These ETFs

If you separate, who will keep the gold?

Ethereum Extends Losing Streak as Technical Pressure Intensifies

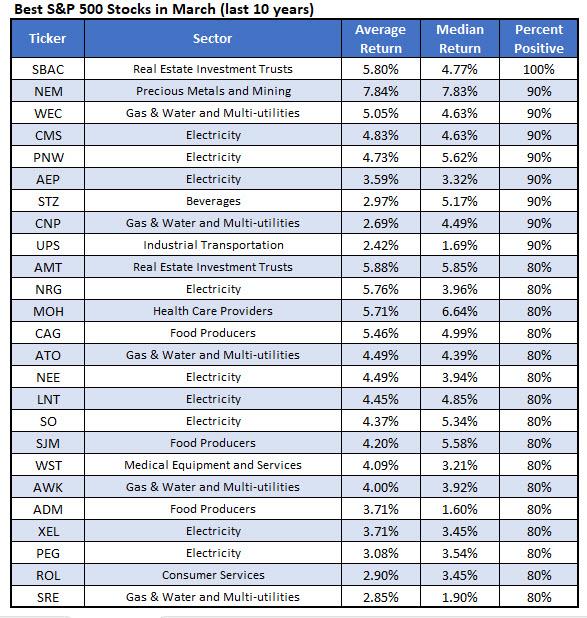

History Says Buy These 25 Stocks in March