InterGroup Upgraded to Neutral on Improving Operations and Liquidity

The InterGroup Corporation INTG has been upgraded to a Neutral rating from Underperform, reflecting improved operating momentum at its core hotel asset, stronger liquidity following a recent property sale and moderating investment-related volatility. However, balance sheet risks and earnings sensitivity to interest rates and refinancing conditions remain key constraints, keeping the overall risk-reward profile balanced despite recent operational progress.

Positives: Stronger Hotel Performance and Improved Liquidity

A primary driver of the rating upgrade is the rebound in hotel operations at the company’s majority-owned Hilton San Francisco Financial District. For the three months ended Dec. 31, 2025, hotel revenues increased 27% to $12.7 million from $10 million in the prior-year period. Average Daily Rate rose to $234 from $190, while occupancy improved to 92% from 88%. These gains translated into a narrowing of hotel-level losses, with net loss from hotel operations narrowing to $1.1 million from $2.8 million a year earlier. The improved metrics reflect stronger pricing power and higher demand, aided by the return of renovated rooms to service.

Liquidity also strengthened during the quarter following the sale of a non-core real estate asset. In December 2025, InterGroup completed the sale of a 12-unit Los Angeles apartment property for approximately $4.9 million. The transaction generated net cash proceeds of roughly $2.6 million and an estimated GAAP gain of about $3.5 million. This gain contributed to a swing in consolidated performance, as the company reported net income of $1 million for the quarter compared to a net loss of $3.7 million in the prior-year period. Beyond the accounting impact, the additional cash enhances financial flexibility and supports ongoing operating initiatives.

Investment-related volatility also moderated. Net loss from investment transactions declined to $0.3 million in the quarter from $0.9 million in the comparable period. At the same time, mortgage interest expense decreased to $3.2 million from $3.5 million, providing incremental support to bottom-line results. Together, these factors point to a more stable earnings profile relative to the prior year.

Challenges Persist

Despite the recent improvement, InterGroup’s balance sheet remains highly leveraged. As of Dec. 31, 2025, total liabilities were approximately $215.7 million, and total shareholders’ deficit stood at roughly $114.5 million. This capital structure limits financial flexibility and leaves the company exposed to operational volatility or shifts in credit conditions.

Another headwind is earnings sensitivity to interest rates and debt maturities. The company carries substantial mortgage obligations, including variable-rate exposure tied to Term SOFR, which can increase interest expense if rates rise. In addition, a meaningful portion of debt comes due in the next few years, creating refinancing risk in a potentially tight credit environment. Elevated borrowing costs or less favorable refinancing terms could pressure cash flows and constrain capital allocation. It is also important to recognize that the return to quarterly profitability was materially aided by the one-time $3.5 million gain on the property sale. While asset sales can unlock value and strengthen liquidity, they are not recurring sources of earnings.

Investment Takeaway

The upgrade to Neutral reflects tangible operational progress, improved liquidity and reduced earnings volatility. However, elevated leverage, ongoing hotel-level losses and dependence on a still-recovering San Francisco market temper upside potential. At current levels, the shares appear fairly balanced between improving fundamentals and persistent financial risk, supporting a Neutral stance.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Dave (DAVE) Stock Is Up Today

Black Diamond’s 2025 Achievements: Evaluating the Commodity Cycle Foundation for 2026

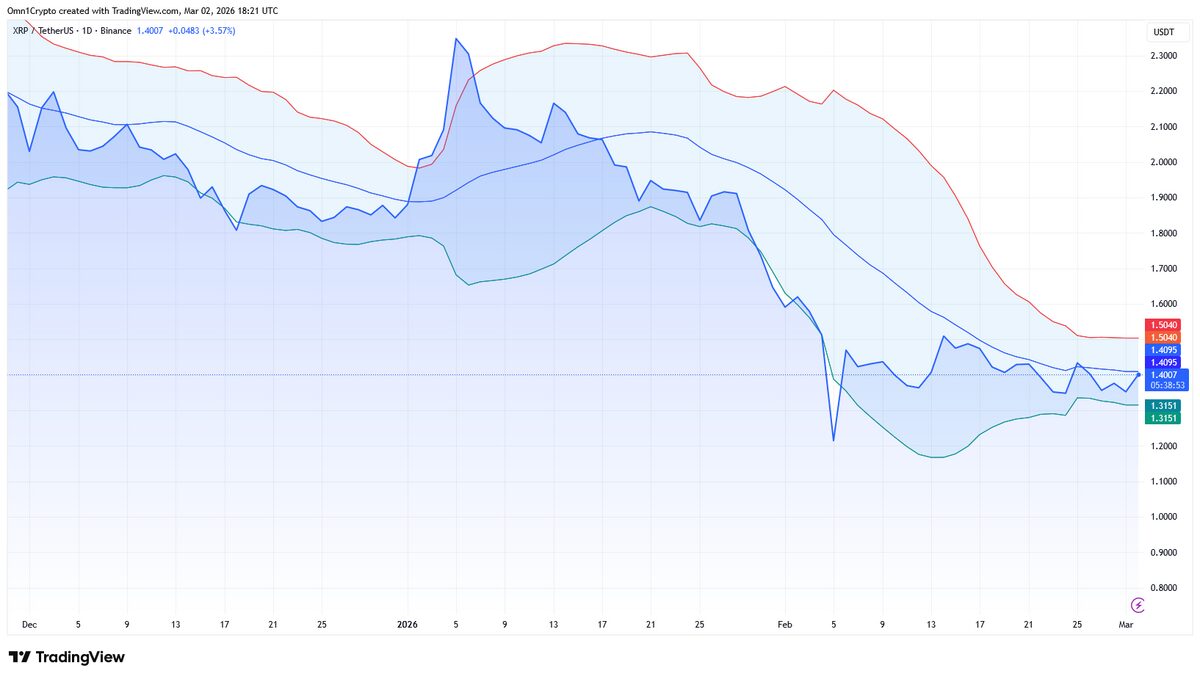

Is XRP Facing The Most Price Turbulence This Week?