Qantas H1 2026: The Trigger for Margin Squeeze

Qantas Shares Tumble Despite Profit Beat

Investors reacted sharply to Qantas' latest financial results. Although the airline posted an underlying pre-tax profit of $1.46 billion, surpassing expectations by 5%, its share price dropped 9.2% in a single day, erasing $1.5 billion from its market value. This dramatic response highlights a shift in market priorities: rather than focusing solely on headline profit growth, investors are scrutinizing the costs behind that growth.

International Segment Under Pressure

The main reason for the sell-off was a noticeable decline in Qantas' international operations. While domestic results remained solid, international operating margins narrowed by 90 basis points to 6.2%. This drop, largely attributed to higher wages and increased investment, has led the market to anticipate ongoing margin challenges. Despite Qantas announcing a 20% dividend boost and a $150 million share buyback, concerns remain about whether these cost pressures are temporary or signal a longer-term issue. If the margin squeeze proves short-lived, the current market reaction could be an overcorrection to weakness in just one part of the business.

Understanding Margin Compression

The margin decline is rooted in rising expenses within the international division, while domestic operations continue to perform well. International earnings before interest and tax (EBIT) came in at $300 million, falling short of the $344 million consensus. Analysts attribute this miss to escalating costs, particularly in wages and investments, even as revenue per available seat kilometer remained stable. This situation exemplifies negative operating leverage, where expenses outpace revenue growth.

Specifically, while revenue per seat held steady, operating margins slipped by 90 basis points to 6.2%, directly impacting profits. Qantas noted that cost increases reduced international EBIT by 6%, with higher engineering and operational wages playing a significant role. These are ongoing costs, not one-off charges, and reflect a 4% increase in frontline staff during the period.

Domestic Operations Remain Robust

In contrast, Qantas' domestic business continues to deliver strong results. Domestic EBIT matched expectations at $676 million, marking a 14% year-on-year rise and maintaining a healthy 14% margin. The domestic segment is scaling efficiently, with revenue per seat up 2% and capacity expanding by 4%. This divergence between strong domestic performance and international cost challenges is at the heart of investor concerns. While overall profit exceeded forecasts thanks to domestic strength, the market's reaction was driven by the international segment's cost issues.

Investment and Future Outlook

Qantas is making significant investments, with net capital expenditure reaching $1.8 billion and a major fleet renewal underway. These investments are currently weighing on international results, while the domestic business benefits from operational discipline. For the share price to recover, investors will need reassurance that international cost pressures can be brought under control.

Capital Management and Upcoming Triggers

Qantas' management has demonstrated confidence in its financial position by announcing a substantial shareholder payout of up to $450 million. This includes a $300 million fully franked dividend—a 20% increase from the previous half—and a $150 million share buyback. Despite ongoing cost inflation, the company’s net debt stands at $5.6 billion, at the lower end of its annual target, indicating sufficient liquidity to fund fleet upgrades and manage short-term challenges.

Project Sunrise and Key Risks

The most immediate potential catalyst for a turnaround is the progress of Project Sunrise. CEO Vanessa Hudson remains optimistic, highlighting strong demand for ultra-long-haul routes such as Perth to London. The project’s success depends on achieving higher yields through a premium cabin mix, rather than simply raising fares. The introduction of A350 ULR aircraft is expected to enhance premium offerings and support earnings growth. If Project Sunrise delivers as planned in the second half, it could help offset current international margin pressures and reinforce Qantas’ long-term growth story.

However, persistent cost inflation—especially in the corporate travel sector—remains a significant risk. Analysts have noted that Qantas has scaled back domestic capacity growth due to weaker corporate demand. Since corporate travel typically generates higher margins, any prolonged weakness in this area could further squeeze group margins, which currently stand at 12.3%. The recent share price decline reflects these concerns, and further softness in corporate demand could intensify pressure, making the success of Project Sunrise a crucial factor for Qantas’ near-term outlook.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Planet Labs Stock Plummets 4.02% Despite $151B Defense Contract Ranks 493rd in Trading Volume

QSR Shares See Modest Rise Following Strategic Shift and Analyst Upgrades, Even as Trading Volume Ranks 463rd

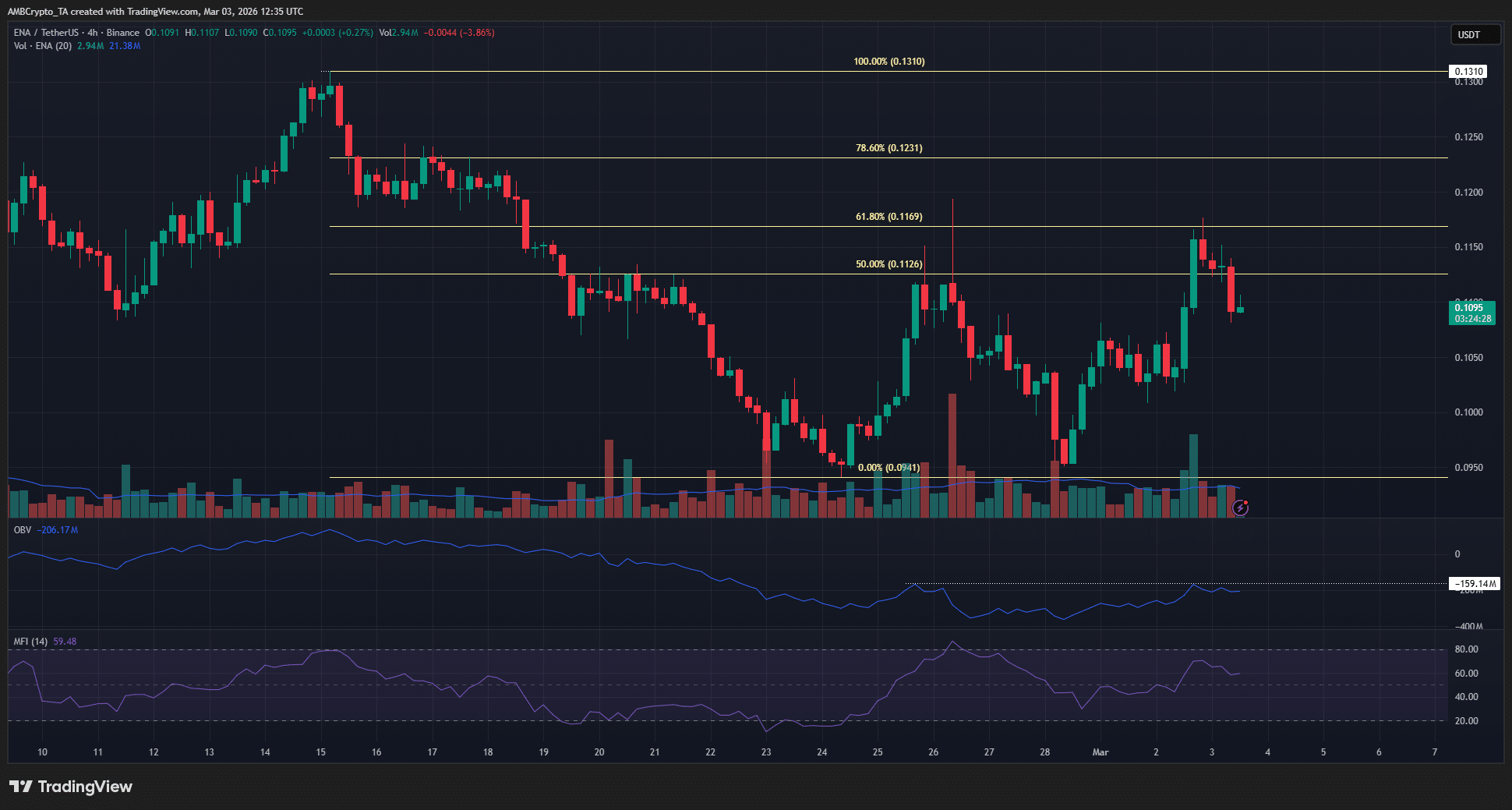

Ethena’s retracement rally, explained: Heavy volume, light conviction

DTE Energy Experiences 56% Jump in Volume, Moving Its Stock to 490th Place in Daily Trading Rankings