Dimon’s ‘No Surprise’: Market Had Already Factored in the Iran Shock

Market Adjusts Quickly After Initial Shock

After an initial jolt, markets quickly regained their footing, with Jamie Dimon’s appearance on CNBC providing a dose of perspective. The CEO of JPMorgan Chase, whose opinions on global risks are highly regarded, reassured investors that a significant inflation surge is unlikely unless the conflict drags on. This comment helped set the tone for market expectations.

Dimon emphasized that the current tensions with Iran are not expected to cause major inflation in the U.S. unless the situation escalates and persists. Essentially, investors were already doubtful about a worst-case scenario. Dimon’s assessment—that the day’s market moves were “not dramatic”—suggested that the initial reaction had already been factored in. The moderate decline in stocks and a contained rise in oil prices reflected a cautious but measured response, which Dimon’s calm demeanor reinforced.

From the perspective of market psychology, this was a textbook example of “sell the news.” Since investors had already anticipated a limited conflict, the actual developments didn’t alter the market’s trajectory. Dimon’s remarks didn’t introduce new risks; instead, they confirmed the prevailing belief that a brief conflict would not derail the economic outlook. As a result, the gap between expectations and reality has narrowed. The initial volatility was a reaction to the headlines, but Dimon’s comments have shifted the outlook to one of cautious observation rather than alarm.

Comparing Expectations to Reality: The Market’s Response

The main gap in expectations is clear. Fears of a prolonged supply disruption pushing Brent crude above $100 per barrel have not come to pass. Instead, oil prices are hovering in the upper $70s—a sharp but controlled increase compared to pre-conflict levels. This serves as a reality check against more extreme predictions.

On the day of the initial shock, Brent crude reached the high $77s after tanker movements through the Strait of Hormuz were effectively halted. Some analysts warned that a prolonged closure could send prices soaring above $100 per barrel. However, current prices remain about 20% below that scenario. The market’s reaction has therefore been one of controlled volatility, not panic.

This restrained response was also seen in equities. Global stock markets experienced a mild downturn, with futures dropping by 1.1% that day. This is far less severe than the kind of sustained selloff that would follow a major inflation shock. The Dow’s initial 600-point drop was quickly reversed, indicating that the market had already priced in the risk.

Ultimately, the expectation gap is defined by the contrast between the current, manageable volatility and the risk of a prolonged supply shock if tanker disruptions persist. For now, markets are operating under the assumption that the conflict will be brief, in line with Dimon’s outlook. The main risk is if this assumption proves incorrect. Should the Strait remain closed for an extended period, markets would have to adjust to a more stressful scenario that they had previously discounted.

Potential Triggers for Market Repricing

The current market stability is precarious, relying on the belief that the conflict will be short-lived and contained. The most immediate factor that could force a rapid market reassessment is the length of the Strait of Hormuz’s closure. Investors have accounted for a temporary disruption, but if it lasts longer than expected, concerns about oil supply could escalate quickly. As experts have cautioned, oil prices could surpass $100 per barrel if trade is disrupted for an extended period. The prevailing calm is based on the expectation that the halt is only temporary, not indefinite.

An even more serious catalyst would be a direct strike on oil infrastructure in countries like Saudi Arabia or the UAE. While such sites have been targeted in the past, there have been no recent reports of damage or disruption to oil facilities in the region. If that were to change, the risk premium would rise sharply. The muted initial market reaction was due to uncertainty about the immediate threat to supply. A confirmed attack on major production or export sites would remove that uncertainty and likely trigger a sustained selloff in energy stocks and a broader move away from risk.

Looking beyond the immediate crisis, markets are also wary of complacency. Jamie Dimon has pointed out that while the current bull market is fueled by optimism around artificial intelligence, he anticipates a shift in the credit cycle. Geopolitical tensions are just one of several macroeconomic challenges—including rising global deficits and increased military spending—that could prompt a broader market reassessment. The current stability in energy markets is only a temporary pause. Investors are waiting for clear signs that the conflict has ended or that oil supplies are secure. Until then, the expectation gap remains, with the duration of the Strait’s closure as the most critical factor.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

XRP Price Analysis: XRP Coin Targets $2 as Middle East Conflict Intensifies

US Stock Market Volatility: Will Crypto Prices Crash Next?

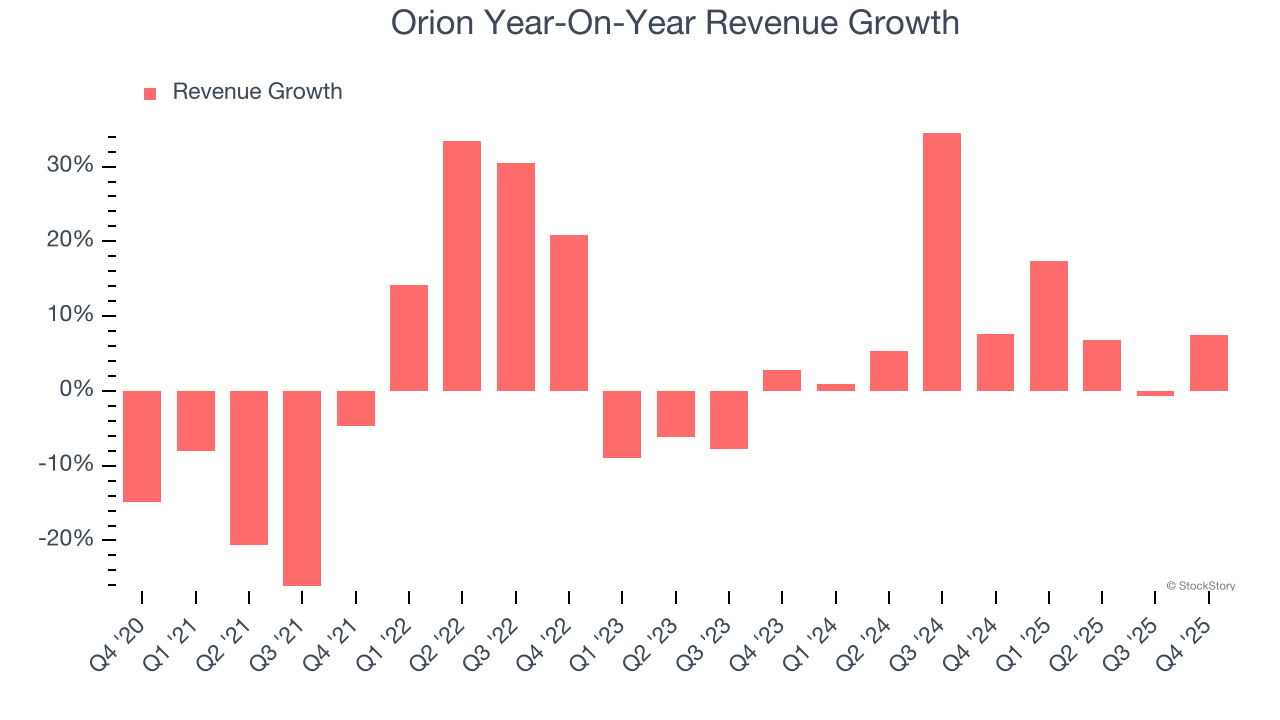

Orion (NYSE:ORN) Reports Upbeat Q4 CY2025 But Stock Drops

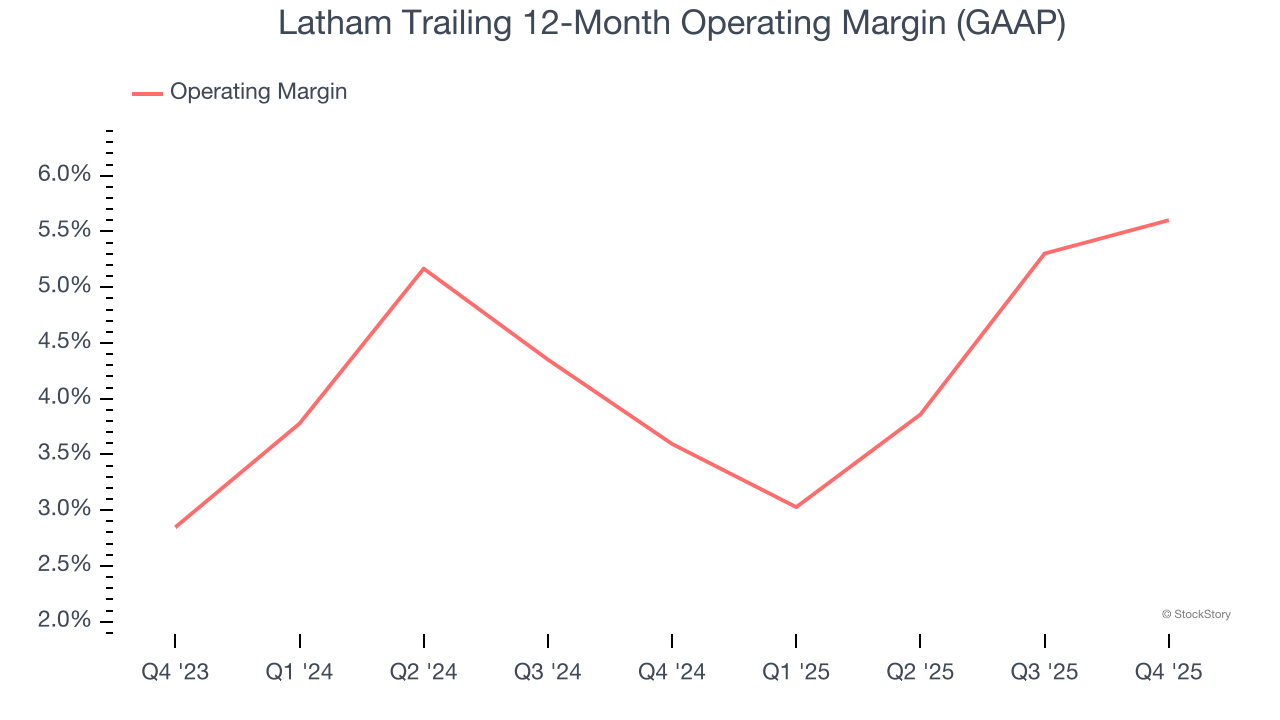

Latham (NASDAQ:SWIM) Delivers Impressive Q4 CY2025, Stock Jumps 14.9%