Asana (NYSE:ASAN) Reports Q4 CY2025 In Line With Expectations But Stock Drops

Work management platform Asana (NYSE:ASAN)

Is now the time to buy Asana?

Asana (ASAN) Q4 CY2025 Highlights:

- Revenue: $205.6 million vs analyst estimates of $205.2 million (9.2% year-on-year growth, in line)

- Adjusted EPS: $0.08 vs analyst estimates of $0.07 (in line)

- Adjusted Operating Income: $18.17 million vs analyst estimates of $15.34 million (8.8% margin, 18.5% beat)

- Revenue Guidance for Q1 CY2026 is $203.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2027 is $0.37 at the midpoint, beating analyst estimates by 2.7%

- Operating Margin: -16.5%, up from -33.8% in the same quarter last year

- Free Cash Flow Margin: 11.8%, up from 6.7% in the previous quarter

- Customers: 25,928 customers paying more than $5,000 annually

- Billings: $234.3 million at quarter end, up 12.1% year on year

- Market Capitalization: $1.68 billion

“FY26 was a year of meaningful progress as we advanced Asana into a multi-product platform and strengthened our position as the foundational system of action layer for the Agentic Enterprise,” said Dan Rogers, Chief Executive Officer of Asana.

Company Overview

Born from the founders' frustration with the inefficiencies of email-based collaboration at Facebook, Asana (NYSE:ASAN) provides a work management platform that helps organizations track projects, set goals, and manage workflows in a centralized digital workspace.

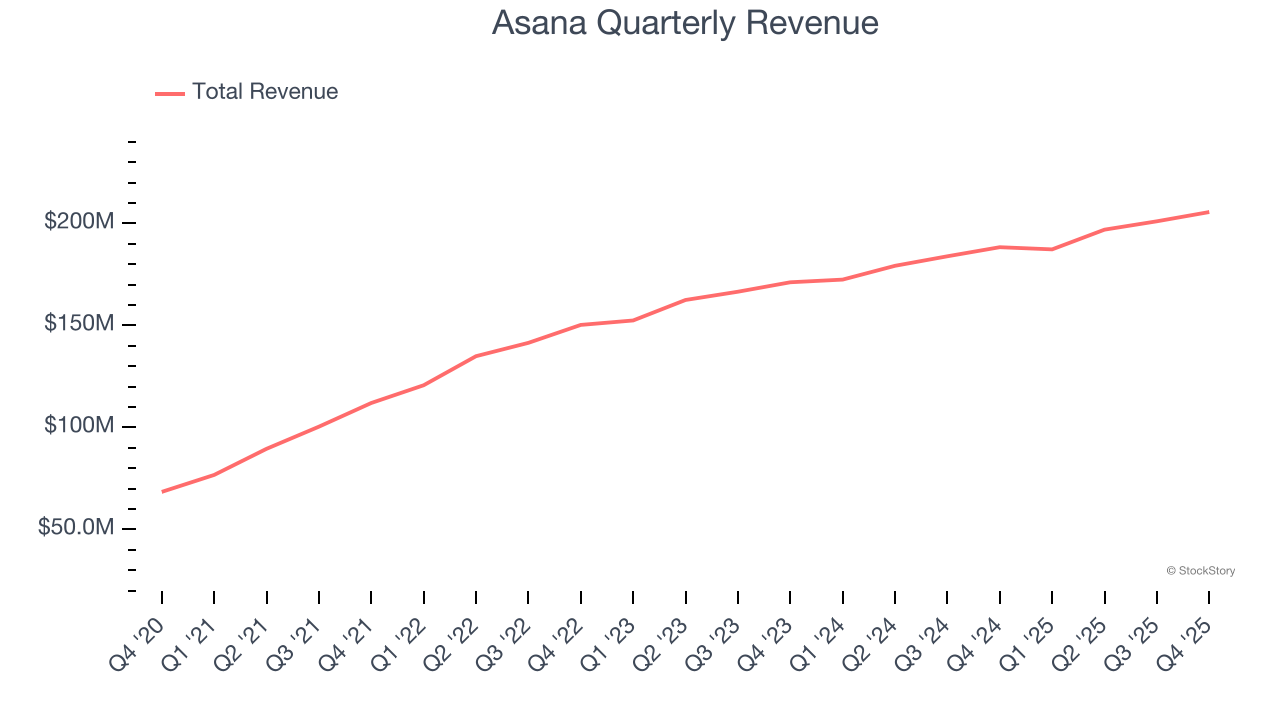

Revenue Growth

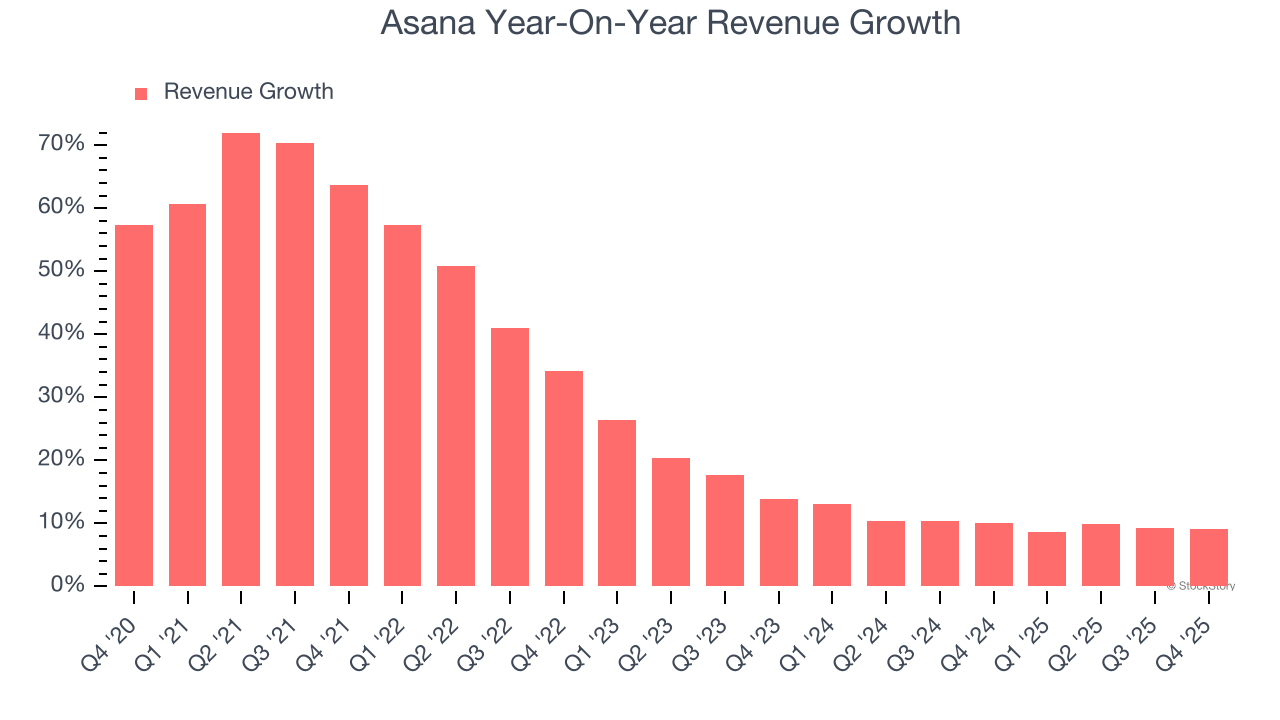

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Asana’s 28.4% annualized revenue growth over the last five years was impressive. Its growth beat the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Asana’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 10.1% over the last two years was well below its five-year trend.

This quarter, Asana grew its revenue by 9.2% year on year, and its $205.6 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 8.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first.

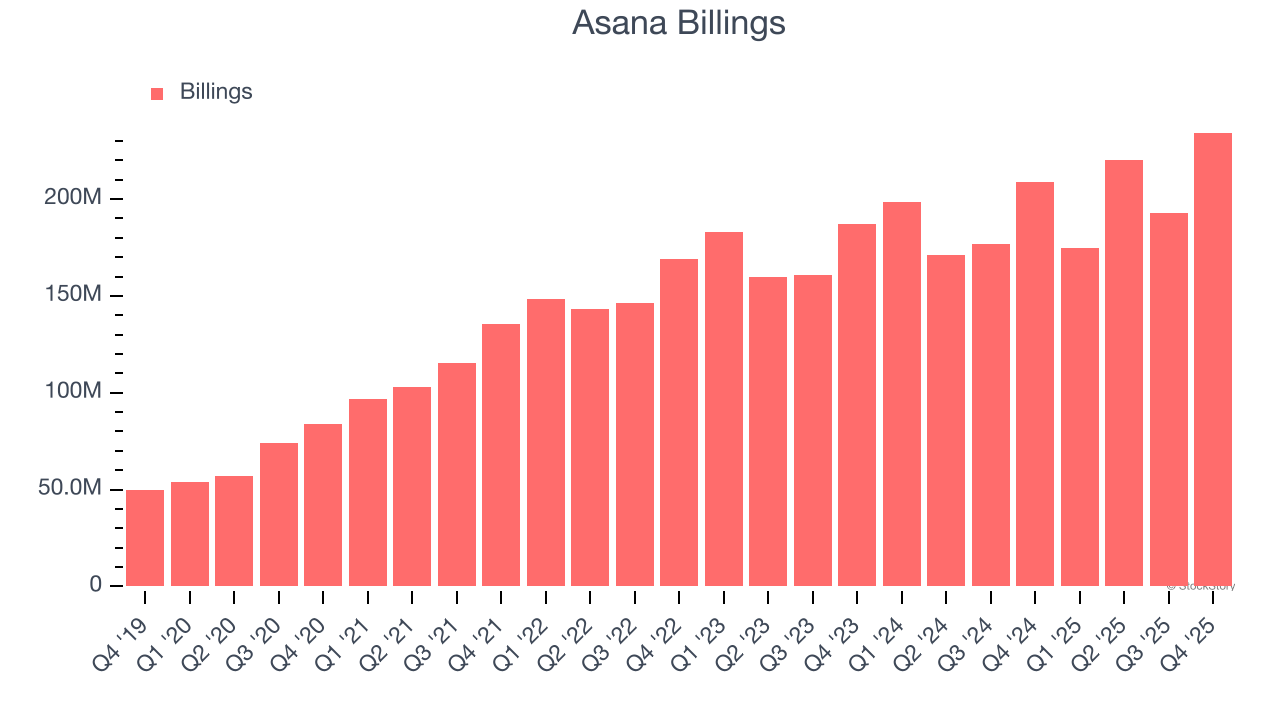

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Asana’s billings came in at $234.3 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 9.4% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

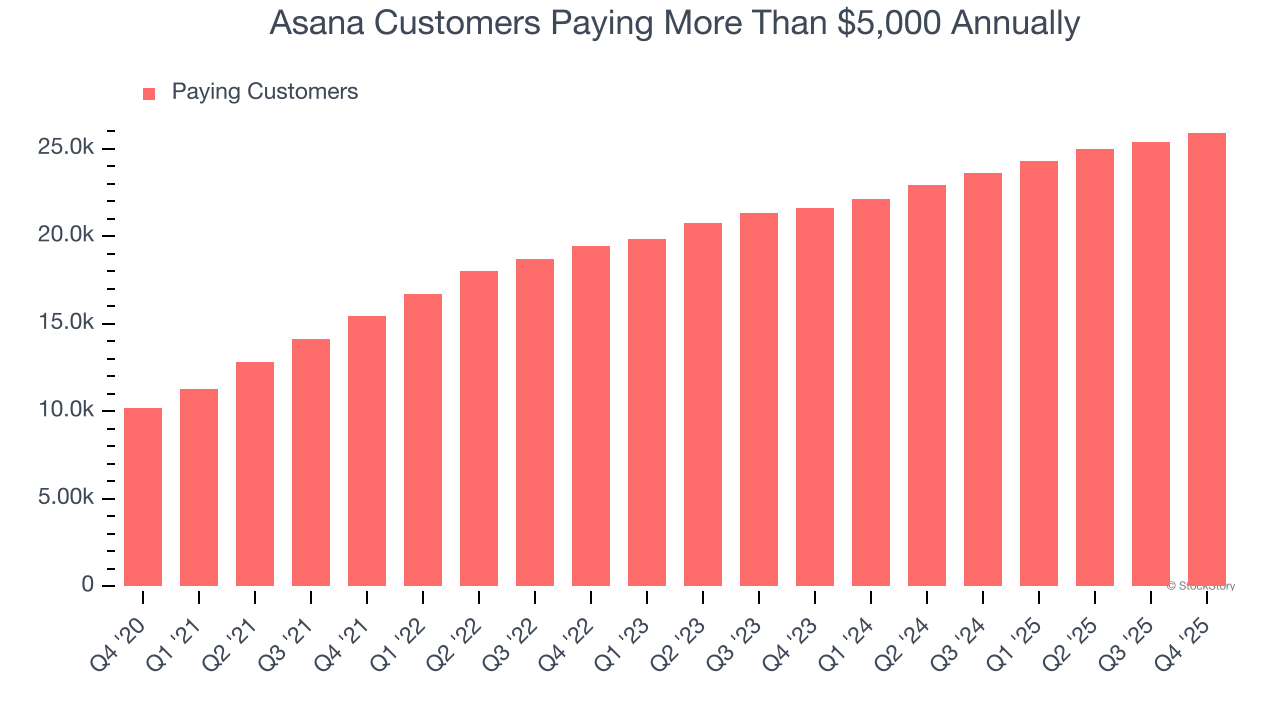

Enterprise Customer Base

This quarter, Asana reported 25,928 enterprise customers paying more than $5,000 annually, an increase of 515 from the previous quarter. That’s quite a bit more contract wins than last quarter but also quite a bit below what we’ve observed over the previous year. This indicates the company is optimizing its go-to-market strategy to reinvigorate growth.

Key Takeaways from Asana’s Q4 Results

It was great to see Asana’s EPS guidance for next quarter top analysts’ expectations. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was in line and its full-year revenue guidance was in line with Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The market seemed to be hoping for more, and the stock traded down 6.2% to $6.85 immediately following the results.

So should you invest in Asana right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

ECB’s Lane: Prolonged conflict could lead to a substantial spike in inflation

Bitcoin’s Next Targets: Why $65K and $58K Matter Right Now

Patterson-UTI Energy, Inc. (PTEN) Reports Fourth Quarter 2025 Financial Results

Seadrill Limited (SDRL) Reports Fourth Quarter and Full Year 2025 Results