The Impact of Artificial Intelligence on the Natural Rate of Interest and Monetary Policy

Show original

By:丹湖渔翁

I. The Natural Rate of Interest Throughout History

My book will be published in March. Not to be immodest, but it will be one of the most important economics books in the next 10-20 years, and it has the potential to profoundly influence or even completely change the way many people analyze economic operations.

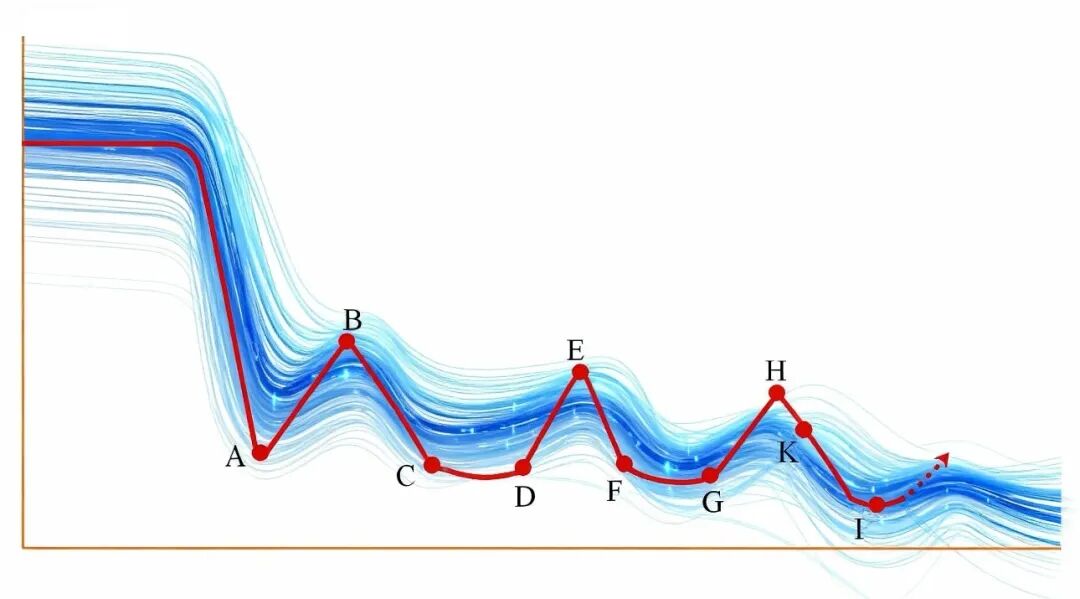

On the cover of the book, I have placed a figure similar to this:

Figure 1 The Natural Rate of Interest in the River of Time

The red line in the chart represents the changing trend of the natural rate of interest (neutral rate) throughout human history. It has three features: [1] It was very high in ancient societies but then declined rapidly as capitalism developed. [2] Each time a technological revolution arrived, it would rise; after the climax of a technological revolution, it would decline again. [3] Over centuries of history, its long-term trend is downward—the next wave always lower than the previous one. For a detailed demonstration of these three features, see my book; I won’t elaborate here.

The blue wave curves in the chart were added using AI software. They [1] imply that, no matter what econometric method is used, the estimated natural rate always resembles a wavy decline; [2] suggest that the natural rate of various economies is roughly the same shape; [3] look attractive.

Where are we now?

Except for a very few lagging countries, over the past few decades, the natural rate of almost all countries has already dropped from a high (Point H or K) to the trough represented by Point I. In this low valley, the economy exhibits many features: sluggish growth in investment and consumption; declining GDP growth; slower growth in the money supply; persistent deflationary pressures; balance sheet recessions occurring repeatedly; rising income inequality; a rightward shift in social ideology; intensified domestic conflicts; increasing social stratification; increasingly acute international tensions, and so forth.

Under such circumstances, fiscal and monetary policies must remain accommodative; otherwise, there will be serious consequences (in fact, we are currently experiencing these consequences).

All these issues, after I published a 30,000-word article on July 6, 2024, I have mentioned fragmentarily in many pieces, but only scratched the surface. In this soon-to-be-published monograph, I have provided detailed and systematic arguments.

II. Predicting the Impact of AI on the Natural Rate of Interest

Once an economy falls into low valleys or “traps” like Points D, G, I, the natural rate cannot escape the trough unless a technological revolution or large-scale system reform occurs. Otherwise, the economy will remain depressed for a long time.

Fortunately, the fourth technological revolution represented by artificial intelligence is arriving. In the short term, it will cause the natural unemployment rate to rise and exacerbate income inequality, but it will also raise productivity, thus increasing the natural rate. As the natural rate rises, it can improve the growth rates of investment, consumption, money demand, and GDP (click), energizing the economy.

But, what happens next? After the peak of the technological revolution, the speed of technological progress will quickly decline, and thus the natural rate will also plummet, just like the prior troughs in the figure. What follows is a decline in GDP growth and the return of deflationary pressure, income inequality worsening again—a repeat of previous episodes of “stagnation.”

Rising income inequality and other factors, in turn, will suppress the natural rate of interest. In the long run, the natural rate will be lower in each successive wave.

III. The Impact on Monetary Policy: Two Views

This has been discussed previously: the natural (neutral) rate is crucial for monetary policy—it is the anchor for rate policy. Among major central banks worldwide, all except a few pay serious attention to it (click, click).

According to my view above, it’s easy to conclude: if AI boosts the natural rate, it will undoubtedly bring more room for interest rate policy. Only after the climax of the technological revolution subsides, and the natural rate falls from a high point, will the space for rate policy be compressed.

However, not everyone agrees with this viewpoint.

In the long article "The Intelligence Crisis of 2028", the author argues that in the “intelligent substitution spiral” in which AI replaces “human intelligence,” white-collar unemployment rises, the residential mortgage market collapses, the economy falls into recession, and financial markets become turbulent. Traditional monetary policy tools (rate cuts, QE) can fix the financial engine but cannot solve problems in the real economy. This is because the real economy fails not due to tight financial conditions, but because AI reduces the value of human intelligence. Even if the central bank cuts rates to zero and launches QE, it cannot change the fact that AI is replacing human labor and that human intelligence is being devalued. In this scenario, easing monetary policy cannot rescue the unemployed, nor the mortgage market, or prevent a financial crisis.

This section may sound convoluted—in more straightforward terms:

AI replaces humans → white-collar unemployment → inability to consume → even if the central bank cuts rates to zero or implements QE, AI will still replace human intelligence, so unemployment persists, consumption continues to shrink, and rate cuts/QE can’t stimulate consumption.

This is exactly the opposite of my own view.

IV. Where is the Core Disagreement?

These two views are diametrically opposed. The reason is that, as previously mentioned, the long article "The Intelligence Crisis of 2028" implies two assumptions:

[1] AI can completely replace human intelligence. Human intellect loses its value. Economic operation no longer needs so many humans involved; just a small number of people plus AI suffices for economic operation and growth. AI is both capital and labor. Most humans become redundant and useless.

[2] When the price of human intellect drops and acquiring knowledge becomes cheap, the demand for such knowledge does not increase, or increases only slightly, and few new jobs are created. Or, any new jobs created can still be performed entirely by AI. Therefore, white-collar workers laid off cannot find work, and thus lose their consumption power.

I have already stated that I do not agree with these two assumptions, and therefore do not agree with its conclusions. In terms of the impact of AI on monetary policy, I also disagree with the view that “monetary policy will become ineffective.” I believe monetary policy will continue to function—see the explanations in the third section of this article.

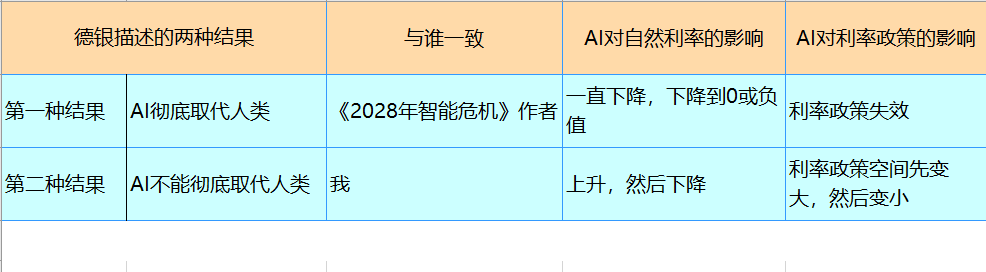

V. Deutsche Bank's View

On February 27, George Saravelos, Global Head of FX Research at Deutsche Bank, released a report exploring two possible outcomes of AI development. The first outcome is that AI completely replaces human labor, with income and wealth concentrated in the hands of a few, material production greatly enriched, but unemployment extremely high and few able to afford things—requiring government intervention. This is similar to the viewpoint of the long article "The Intelligence Crisis of 2028" . The underlying assumptions are clearly similar. In this scenario, rate policy is definitely ineffective.

The second outcome, however, is closer to my viewpoint: like previous innovations, AI is just an enabling technology and will eventually create new job positions. Macroeconomic indicators will rise, inflation levels, real interest rates, and the stock market will all increase. This obviously aligns with my view (see here, here and earlier in this article). In this case, there will be more room for rate policy. After the next tech revolution peaks and the natural rate falls again, the policy space will contract.

As stated at the beginning of this article, in the long run, over hundreds or even thousands of years, the natural rate will decline further and further—perhaps in decades or a century, it falls to extremely low levels (zero or negative), and rate policy becomes ineffective. But by then humanity may have entered a new stage of economic formation, so it is not necessary to worry about this now.

The second outcome, however, is closer to my viewpoint: like previous innovations, AI is just an enabling technology and will eventually create new job positions. Macroeconomic indicators will rise, inflation levels, real interest rates, and the stock market will all increase. This obviously aligns with my view (see here, here and earlier in this article). In this case, there will be more room for rate policy. After the next tech revolution peaks and the natural rate falls again, the policy space will contract.

As stated at the beginning of this article, in the long run, over hundreds or even thousands of years, the natural rate will decline further and further—perhaps in decades or a century, it falls to extremely low levels (zero or negative), and rate policy becomes ineffective. But by then humanity may have entered a new stage of economic formation, so it is not necessary to worry about this now.

0

0

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

PoolX: Earn new token airdrops

Lock your assets and earn 10%+ APR

Lock now!

You may also like

BlackRock under pressure: The finance giant limits withdrawals

Cointribune•2026/03/08 09:33

Ripple: We Use XRP to Generate Liquidity for Payment Flows

TimesTabloid•2026/03/08 09:03

Bitcoin ‘bull trap’ forming as bear market enters middle phase: Willy Woo

Cointelegraph•2026/03/08 08:09

US Treasury report acknowledges legitimate uses of crypto mixers

Cointelegraph•2026/03/08 08:06

Trending news

MoreCrypto prices

MoreBitcoin

BTC

$67,871.71

-0.32%

Ethereum

ETH

$1,966.47

-1.09%

Tether USDt

USDT

$1.0000

+0.00%

BNB

BNB

$620.84

-1.44%

XRP

XRP

$1.36

-0.36%

USDC

USDC

$1.0000

+0.01%

Solana

SOL

$83.36

-1.55%

TRON

TRX

$0.2868

+1.08%

Dogecoin

DOGE

$0.09029

-0.23%

Cardano

ADA

$0.2549

-1.34%

How to buy BTC

Bitget lists BTC – Buy or sell BTC quickly on Bitget!

Trade now

Become a trader now?A welcome pack worth 6200 USDT for new users!

Sign up now