Wheaton Precious Metals Surges 1.26% as Trading Volume Vaults to $0.43 Billion Rank 305 in Daily Activity

Market Snapshot

Wheaton Precious Metals (WPM) closed March 2, 2026, with a 1.26% increase in its stock price, marking a positive performance in a volatile market. Trading volume surged to $0.43 billion, a 49.24% rise from the previous day, placing it at rank 305 in daily trading activity. The stock’s strong volume and price appreciation suggest heightened investor interest, potentially driven by upcoming earnings expectations and strategic business developments.

Key Drivers

Earnings Expectations and Historical Performance

WPM is poised to release its fourth-quarter 2025 earnings on March 12, with the Zacks Consensus Estimate projecting earnings of $0.92 per share—a 109% increase compared to the same period in 2024. This follows a trailing four-quarter average earnings surprise of 5.9%, indicating consistent outperformance relative to analyst expectations. For context, the company’s third-quarter 2025 results showed revenue of $476 million and net earnings of $367 million, driven by robust silver prices and production efficiency. While Q3 earnings slightly missed forecasts (EPS of $0.618 vs. $0.6182), the stock rose 2.65% post-release, reflecting investor confidence in management’s ability to navigate market conditions.

Analyst Optimism and Price Targets

Analyst sentiment remains overwhelmingly bullish, with multiple institutions maintaining or upgrading their recommendations. TD Securities and BofA Securities both reaffirmed “Buy” ratings in recent months, with TD setting a $164 price target (up 0.21% from the current level). RBC Capital upgraded its stance to “Outperform” in December 2025, raising its price target to $130. While UBS has been more cautious, maintaining a “Hold” rating, its $118–$122 price range still reflects confidence in WPM’s long-term potential. The average analyst price target of $177.22, as of February 2026, suggests a potential upside of 7.2% from the current $165.72 price.

Strategic Transactions and Cash Flow Projections

A critical catalyst for WPM’s recent momentum is its aggressive expansion through streaming agreements. The company secured two major deals in late 2025: a $300 million gold-equivalent stream from the Hemlo mine and a $670 million stream from the Spring Valley project. These transactions, totaling nearly $1 billion, are expected to bolster operating cash flows, which management forecasts will average $2.5 billion annually over the next five years. CEO Randy Smallwood emphasized the company’s pioneering role in the streaming model, which allows WPMWPM+1.26% to secure low-cost production while mitigating operational risks. CFO Vincent Lau highlighted the strategic advantage of its silver exposure, a commodity that has historically outperformed gold in 2025 due to industrial demand and macroeconomic tailwinds.

Production Guidance and Market Position

WPM’s 2025 production guidance of 600,000–670,000 gold-equivalent ounces underscores its capacity to capitalize on favorable commodity prices. This aligns with broader industry trends, as gold and silver prices reached multi-year highs in early 2026 amid inflationary pressures and geopolitical uncertainty. The company’s trailing performance, including a 138% year-over-year increase in net earnings to $367 million in Q3 2025, further validates its ability to convert higher commodity prices into profitability. With a market cap of $75.34 billion and a P/E ratio of 74.99, WPM trades at a premium to peers, reflecting its unique business model and growth trajectory.

Risks and Market Dynamics

Despite the optimism, WPM faces headwinds, including macroeconomic volatility and potential regulatory scrutiny of streaming agreements. A decline in silver prices, which accounted for a significant portion of its revenue in 2025, could pressure margins. Additionally, while analyst price targets remain elevated, the average of $177.22 implies a 7.2% upside, which is modest compared to the stock’s 140% return over the past year. Investors will closely watch the March 12 earnings report for clues on whether the company can sustain its momentum in a tightening monetary policy environment.

Conclusion

WPM’s recent performance reflects a confluence of strong earnings expectations, strategic capital allocation, and favorable market conditions. The combination of analyst optimism, production growth, and innovative financing through streaming agreements positions the company to outperform in the gold and silver sector. However, investors must remain cognizant of macroeconomic risks and commodity price volatility, which could impact its trajectory in the coming quarters.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Analysis-Investors make a dash for cash as Iran crisis upends markets

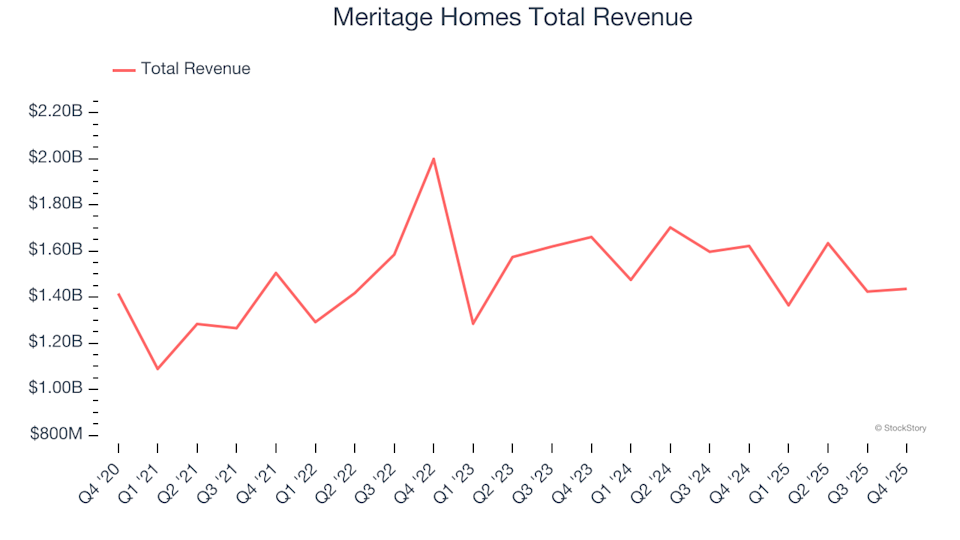

Home Construction Stocks Q4 Overview: Comparing Meritage Homes (NYSE:MTH)

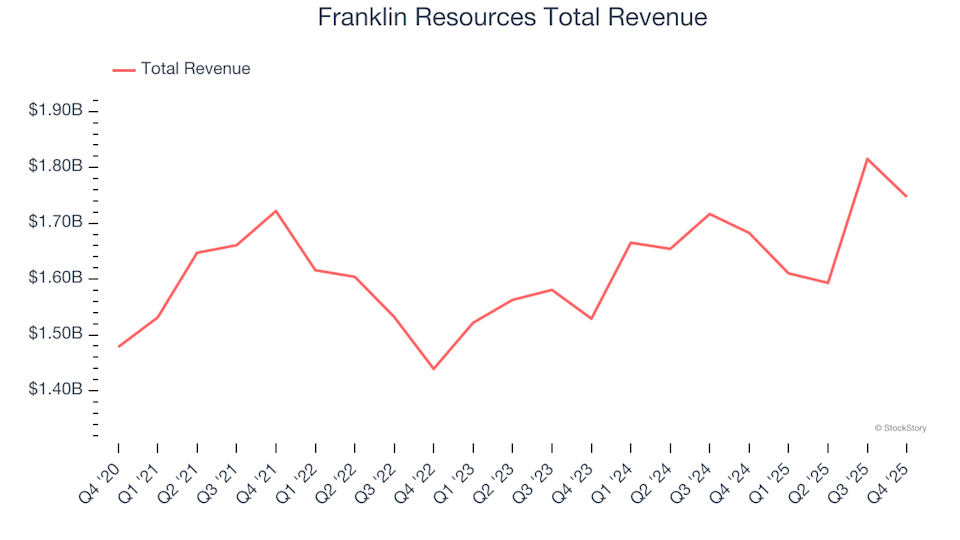

Reflecting on the fourth quarter financial results of custody banks: Franklin Resources (NYSE:BEN)

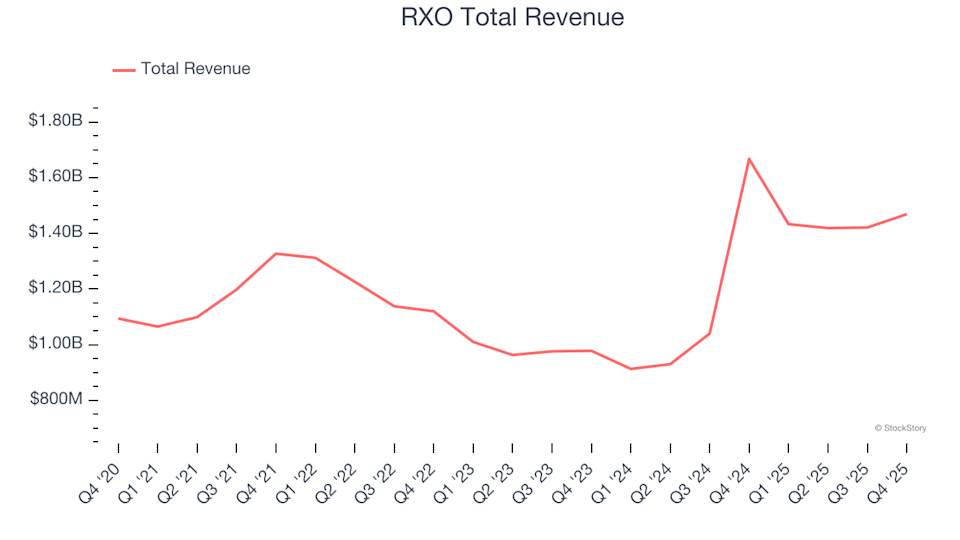

Ground Transportation Shares Q4 Overview: Comparing RXO (NYSE:RXO) Performance