Subtle US Treasury Bonds

Show original

By:BFC汇谈

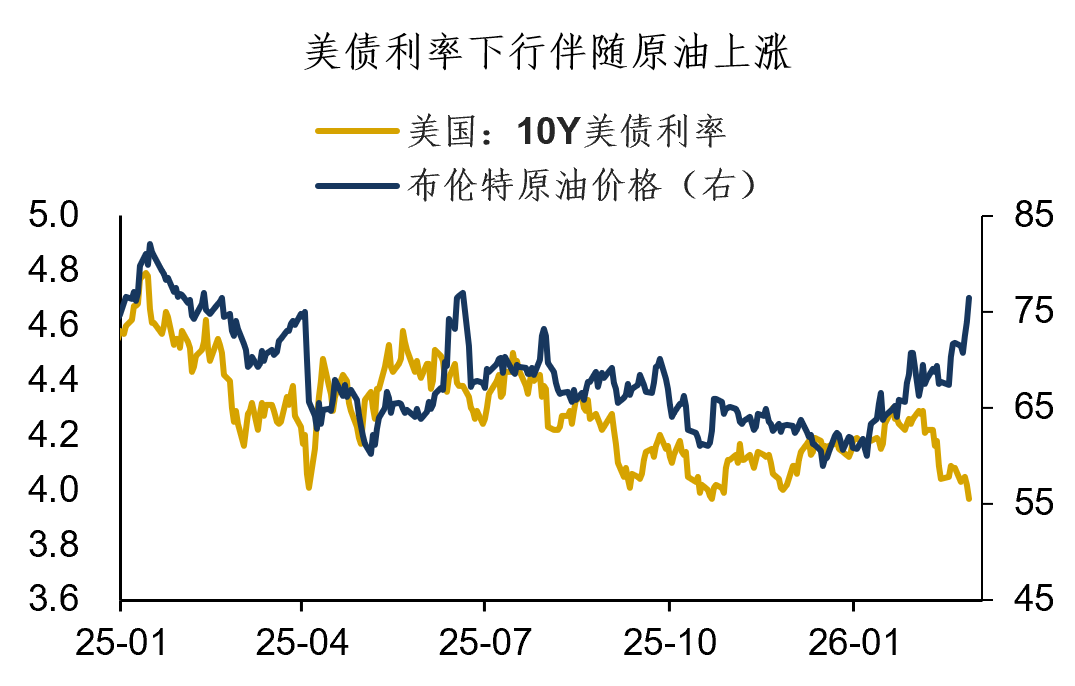

In the recent global financial markets, aside from those assets under the spotlight, there is one asset that quietly broke through a key level: US Treasury bonds. Since February, US Treasury yields have shown a downward trend, with the mid-to-long end (5-10Y) declining more significantly, and the 10Y Treasury yield dropping below 4.0%. This round of declining US Treasury yields is somewhat peculiar, with the strangeness lying in the fact that—throughout the entire decline, it was accompanied by rising oil prices.

Theoretically, rising oil prices influence inflation expectations and are generally bearish for Treasuries. However, the peculiarity of this round lies in that the increase in oil prices has not spurred inflation expectations, as both the Breakeven and Inflation Swap for Treasuries have remained stable. For example, the 5y5y Inflation Swap has fallen 10bps from its recent highs, and the Breakeven rate has also edged lower.

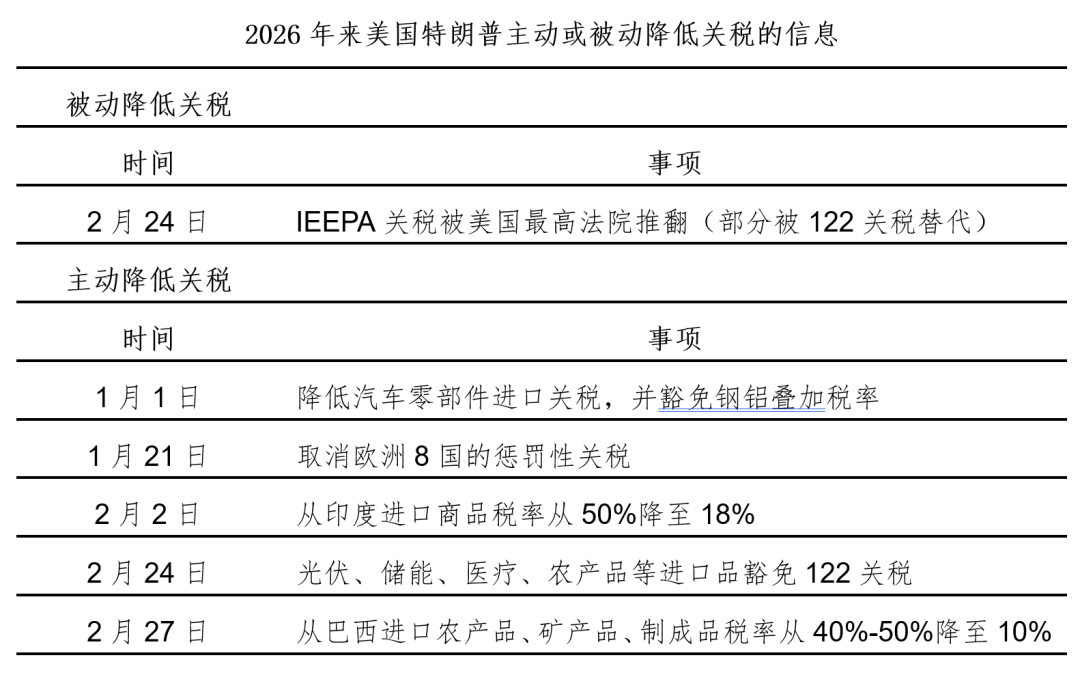

Theoretically, rising oil prices influence inflation expectations and are generally bearish for Treasuries. However, the peculiarity of this round lies in that the increase in oil prices has not spurred inflation expectations, as both the Breakeven and Inflation Swap for Treasuries have remained stable. For example, the 5y5y Inflation Swap has fallen 10bps from its recent highs, and the Breakeven rate has also edged lower.  Why have US Treasuries not priced in the inflationary impact of higher oil prices? In my view, there are several reasons: First, the Trump administration, either proactively or passively, rolled back many tariffs, reducing their inflationary impact. Since 2026, the Trump administration, considering Affordability, has proactively withdrawn many tariffs. The overturning of IEEPA tariffs has also functioned as a literal tax cut, helping to control inflation.

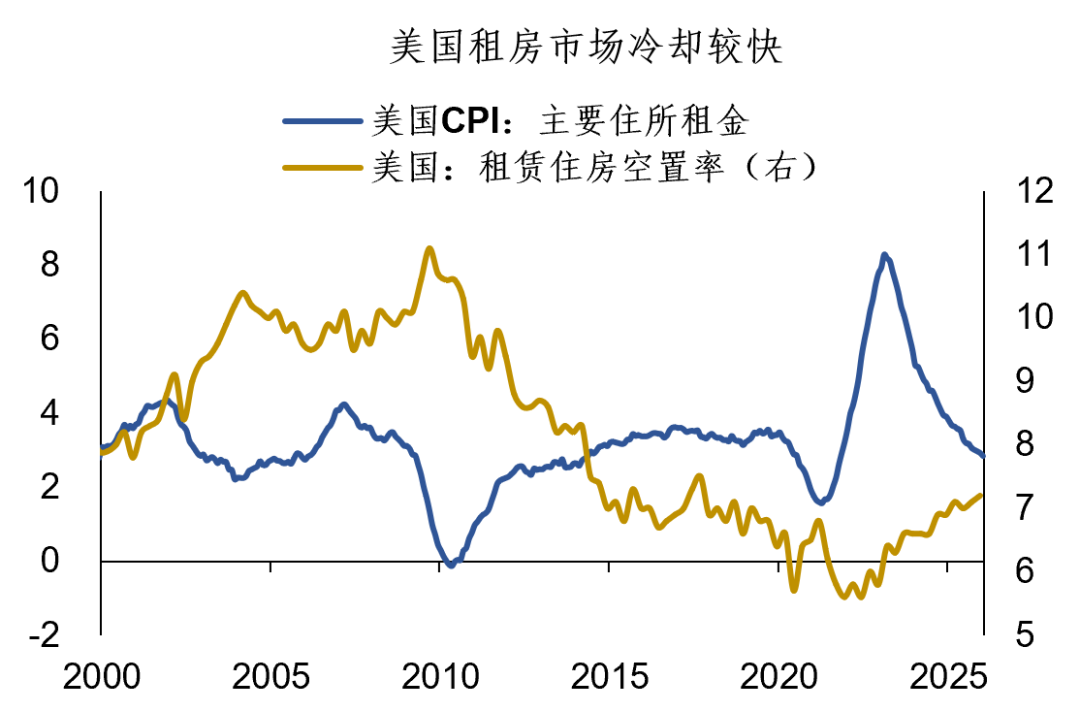

Why have US Treasuries not priced in the inflationary impact of higher oil prices? In my view, there are several reasons: First, the Trump administration, either proactively or passively, rolled back many tariffs, reducing their inflationary impact. Since 2026, the Trump administration, considering Affordability, has proactively withdrawn many tariffs. The overturning of IEEPA tariffs has also functioned as a literal tax cut, helping to control inflation.  Second, one important component of US inflation—rent inflation—is slowing. The US rental vacancy rate has risen to 7.2%, surpassing pre-pandemic levels. The rapid cooling of the rental market means that CPI-rent is trending lower, offsetting the impact of rising oil prices.

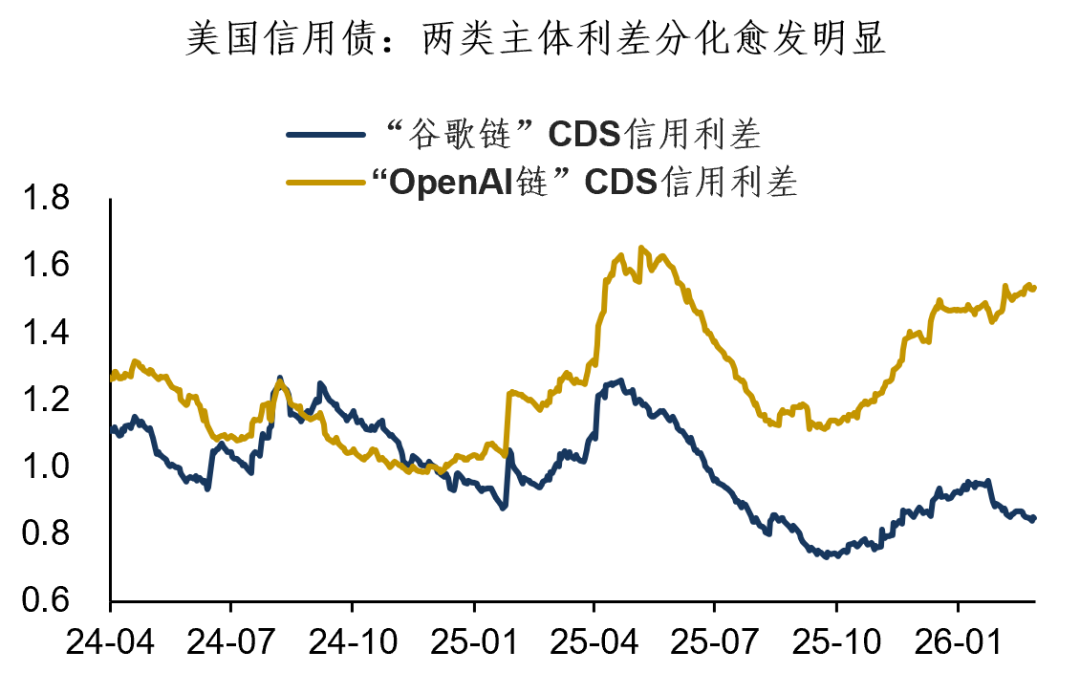

Second, one important component of US inflation—rent inflation—is slowing. The US rental vacancy rate has risen to 7.2%, surpassing pre-pandemic levels. The rapid cooling of the rental market means that CPI-rent is trending lower, offsetting the impact of rising oil prices.  Third, US equities continued their acceleration in divergence, and overall risk appetite has cooled significantly, leading the market to pay less attention to the inflation topic. As previously covered in our article "USD: US Stocks Show Signs of Change". More recently, the divergence between “Google Chain” stocks and “OpenAI Chain” stocks has intensified. Furthermore, this divergence is spreading into the credit market, with Oracle CDS rising to its highest level since 2009. The marked cooling of risk appetite in US equities indirectly benefits Treasuries.

Third, US equities continued their acceleration in divergence, and overall risk appetite has cooled significantly, leading the market to pay less attention to the inflation topic. As previously covered in our article "USD: US Stocks Show Signs of Change". More recently, the divergence between “Google Chain” stocks and “OpenAI Chain” stocks has intensified. Furthermore, this divergence is spreading into the credit market, with Oracle CDS rising to its highest level since 2009. The marked cooling of risk appetite in US equities indirectly benefits Treasuries.

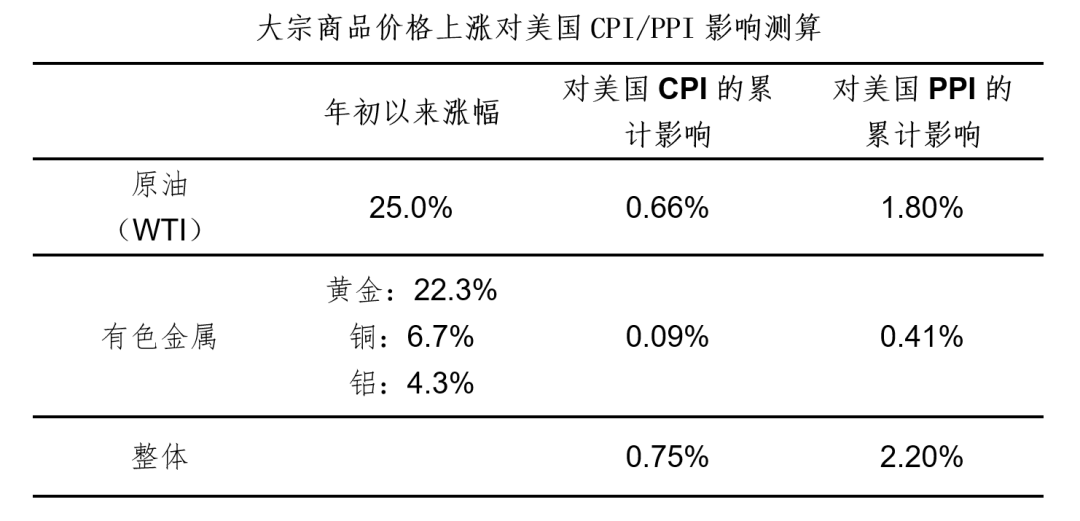

Although US Treasuries have not yet sufficiently priced in the impact of rising oil prices, in my view, the inflationary effect will gradually become apparent after March. This is because January’s US CPI corresponds to a short-term low point in oil prices. As subsequent monthly inflation data is released, the risk for a higher CPI could grow. Based on our calculations, the broad commodity price effect (including oil, copper, gold, etc.) could boost US CPI by about 0.7%, and US PPI by about 2.2%. This impact will gradually be reflected in the ensuing months.

Although US Treasuries have not yet sufficiently priced in the impact of rising oil prices, in my view, the inflationary effect will gradually become apparent after March. This is because January’s US CPI corresponds to a short-term low point in oil prices. As subsequent monthly inflation data is released, the risk for a higher CPI could grow. Based on our calculations, the broad commodity price effect (including oil, copper, gold, etc.) could boost US CPI by about 0.7%, and US PPI by about 2.2%. This impact will gradually be reflected in the ensuing months.  Overall, US inflation does face upside risks in the near future, but with a mix of bullish and bearish factors, it is hard to gauge exactly how high it could go. What is certain is that risks on the inflation front are sufficient to support a “more entangled” Federal Reserve. At the 4.0% level, US Treasuries present potential for disagreement—depending on whether you have an allocation or a trading perspective, conclusions may differ entirely. For the FX market, however, the impact of strong oil prices seems clearer: higher oil prices are always somewhat bearish for the euro and bullish for the USD… To summarize today’s discussion: 1. The 10Y US Treasury yield has broken below 4.0%. This round of yield decline is peculiar in that it coincided entirely with rising oil prices, yet Breakeven and Inflation Swap remain stable, and Treasuries have not sufficiently priced the inflationary effect of oil’s rise; 2. Some observations: the Trump administration proactively or passively rolled back many tariffs, reducing their inflation impact. Also, a major component of US inflation—rent inflation—is slowing. Third, the US equities’ accelerated divergence and cooled risk appetite have led to less market attention on the inflation topic. It’s worth noting that after March the inflationary impact of higher oil prices will gradually emerge; there are definitely inflation risks, enough to support a “more tangled” Federal Reserve; 3. In my view, the 4.0% mark for Treasuries is highly contentious—whether from an allocation or trading perspective, the conclusions may differ entirely. In the FX market, the logic seems clearer: high oil prices always tend to be more negative for the euro and more positive for the USD…

Overall, US inflation does face upside risks in the near future, but with a mix of bullish and bearish factors, it is hard to gauge exactly how high it could go. What is certain is that risks on the inflation front are sufficient to support a “more entangled” Federal Reserve. At the 4.0% level, US Treasuries present potential for disagreement—depending on whether you have an allocation or a trading perspective, conclusions may differ entirely. For the FX market, however, the impact of strong oil prices seems clearer: higher oil prices are always somewhat bearish for the euro and bullish for the USD… To summarize today’s discussion: 1. The 10Y US Treasury yield has broken below 4.0%. This round of yield decline is peculiar in that it coincided entirely with rising oil prices, yet Breakeven and Inflation Swap remain stable, and Treasuries have not sufficiently priced the inflationary effect of oil’s rise; 2. Some observations: the Trump administration proactively or passively rolled back many tariffs, reducing their inflation impact. Also, a major component of US inflation—rent inflation—is slowing. Third, the US equities’ accelerated divergence and cooled risk appetite have led to less market attention on the inflation topic. It’s worth noting that after March the inflationary impact of higher oil prices will gradually emerge; there are definitely inflation risks, enough to support a “more tangled” Federal Reserve; 3. In my view, the 4.0% mark for Treasuries is highly contentious—whether from an allocation or trading perspective, the conclusions may differ entirely. In the FX market, the logic seems clearer: high oil prices always tend to be more negative for the euro and more positive for the USD…

0

0

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

PoolX: Earn new token airdrops

Lock your assets and earn 10%+ APR

Lock now!

You may also like

Panic Grips Korean Stock Market in Largest Single-Day Plunge Ever Recorded

101 finance•2026/03/04 09:03

Bitcoin absorbs U.S. government transfer and Middle East FUD – Details

AMBCrypto•2026/03/04 09:00

JPY: Risk-off support and policy uncertainty – MUFG

101 finance•2026/03/04 08:57

Wall Street analysts caution against relying on Trump to stabilize markets shaken by the Iran conflict

101 finance•2026/03/04 08:54

Trending news

MoreCrypto prices

MoreBitcoin

BTC

$71,457.11

+7.42%

Ethereum

ETH

$2,073.83

+6.46%

Tether USDt

USDT

$1

+0.03%

BNB

BNB

$652.1

+4.80%

XRP

XRP

$1.41

+5.02%

USDC

USDC

$1

+0.01%

Solana

SOL

$90.57

+7.52%

TRON

TRX

$0.2842

+1.07%

Dogecoin

DOGE

$0.09304

+3.83%

Cardano

ADA

$0.2724

+2.92%

How to buy BTC

Bitget lists BTC – Buy or sell BTC quickly on Bitget!

Trade now

Become a trader now?A welcome pack worth 6200 USDT for new users!

Sign up now