Lennox’s Volume Dives to 472nd Rank as Shares Slide 1.15% on Missed Earnings and Weak Market Outlook

Market Snapshot

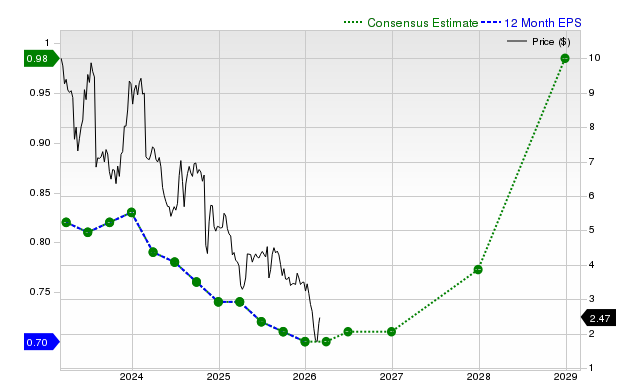

On March 2, 2026, Lennox International Inc.LII-1.15% (LII) traded with a volume of $0.28 billion, a 46.21% decline from the previous day’s volume, ranking it 472nd in trading activity. The stock closed down 1.15%, reflecting continued investor caution following mixed earnings results and broader market conditions. Despite a record 20.4% full-year segment margin, the company’s Q4 2025 earnings and revenue both missed estimates, contributing to the downward pressure on its shares.

Key Drivers

Earnings and Revenue Misses in Q4 2025

Lennox reported Q4 2025 earnings of $4.45 per share, below the $4.77 forecast, and revenue of $1.2 billion, shy of the $1.27 billion estimate. The 6.71% EPS shortfall and 5.51% revenue shortfall led to a 0.54% stock decline immediately following the report. These results highlighted the company’s struggle with weak residential and commercial markets, which contributed to an 11% year-over-year revenue decline. While the company managed to maintain a record segment margin of 20.4%, the earnings miss underscored challenges in translating operational efficiency into top-line growth.

Operational Efficiency and Cash Flow Strength

Despite the revenue decline, LennoxLII-1.15% demonstrated resilience in cash flow generation, producing $406 million in Q4 and $758 million for the full year. This operational efficiency was attributed to cost controls and margin expansion, particularly in its core HVAC segments. The company’s ability to generate robust cash flow amid market headwinds reinforced its financial flexibility, though investors remained skeptical about the sustainability of these gains in a volatile market. Management emphasized that the cash flow strength would support strategic investments and shareholder returns, but the lack of immediate visibility on market recovery kept equity valuations under pressure.

2026 Guidance and Market Outlook

For 2026, Lennox projected 6-7% revenue growth, adjusted EPS of $23.50–$25.00, and free cash flow of $750–$850 million. These forecasts reflect cautious optimism about a market recovery, particularly in residential and commercial heating, ventilation, and air conditioning (HVAC) sectors. CEO Alok Maskara highlighted the significance of achieving a 20% segment margin for the first time, while CFO Michael Quenzer reiterated a focus on EBIT margin expansion and revenue growth. However, the guidance fell short of some analysts’ expectations, with the projected 6-7% revenue growth seen as conservative given the company’s historical performance in stronger markets.

Leadership and Strategic Priorities

The earnings report underscored a strategic pivot toward margin preservation and disciplined growth. Lennox’s leadership emphasized that the company’s focus on operational efficiency and cost management would remain central to its strategy, even as it navigates a challenging macroeconomic environment. The 20.4% segment margin marked a milestone, but analysts noted that maintaining this level would require continued execution in cost controls and pricing power. Additionally, the company’s 2026 guidance included a target for free cash flow, signaling its intent to balance reinvestment in growth opportunities with returns to shareholders.

Broader Market Context

Lennox’s stock performance on March 2, 2026, was also influenced by broader market trends. The HVAC sector, which includes competitors like Honeywell and Carrier, faced headwinds from slowing construction activity and inventory adjustments. While Lennox’s margin expansion outperformed industry averages, the overall sector’s underperformance limited investor enthusiasm. The 1.15% drop in Lennox’s stock mirrored a broader selloff in industrial and manufacturing equities, as investors weighed concerns about economic growth and interest rate volatility.

Conclusion

The interplay of earnings misses, margin strength, and cautious guidance created a mixed outlook for Lennox. While the company’s cash flow generation and margin expansion demonstrated operational resilience, the revenue decline and weak market conditions tempered investor sentiment. The 2026 guidance, though conservative, provided a framework for potential recovery, but execution risks remain high. As the company navigates a challenging market, its ability to maintain margin discipline and capitalize on sector-specific growth opportunities will be critical to regaining investor confidence.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AI disruption will challenge lending decisions in coming years, Goldman exec says

U.S. and Japan Consider Nuclear Power Collaboration in Monumental $550 Billion Agreement

Surging Earnings Estimates Signal Upside for Clarivate (CLVT) Stock