medmix AG 2025: The Margin Surprise That Investors Had Anticipated

Market Response: High Expectations and Revenue Challenges

medmix's annual results were met with a subdued market reaction, illustrating how elevated expectations can temper investor enthusiasm. Although the company outperformed on margins—delivering a "beat and raise"—the share price remained stagnant, as this positive outcome had already been anticipated. The ongoing decline in revenue, however, reinforced the market's primary concern and overshadowed the margin improvements.

Examining the figures, medmix reported CHF 448.0 million in revenue for the year, marking a 4.8% organic decrease compared to the previous year. While this result matched the company's updated guidance, it fell short of the organic growth investors had hoped for. The standout achievement was in profitability: medmix surpassed its EBITDA margin target, reaching 20%, a year-over-year improvement of 90 basis points. Additionally, the gross profit margin rose by 310 basis points to 36.1%, highlighting operational gains.

Despite these margin successes, investor attention shifted to the updated outlook for 2026, which projected flat to modest organic growth. The margin improvements were seen as the expected outcome of the company's Growth and Efficiency program, which management noted was progressing ahead of schedule. As a result, the market viewed strong profitability as the new standard, while persistent revenue weakness remained a concern. Since the margin beat was anticipated, there was little incentive for investors to act, and the stock's performance reflected this sentiment.

Resetting Expectations: Focus on Profitability and Returns

medmix's revised guidance signals a shift in market priorities—from revenue expansion to consistent profitability and shareholder value. The 2026 forecast maintains expectations of flat to low single-digit organic revenue growth, with an adjusted EBITDA margin around 20%. Rather than raising expectations, management is establishing a new baseline. The midterm target for an adjusted EBITDA margin above 21% represents a fundamental change in long-term outlook, emphasizing ongoing margin improvement. This commitment suggests that the Growth and Efficiency program will continue to drive profitability, not just deliver a one-off benefit. The market is now recalibrating its consensus toward higher margins, even if revenue growth remains subdued.

Additionally, the proposed dividend of CHF 0.10 per share underscores medmix's intention to return capital to shareholders. Following a year of robust profit gains and a return to net income, this dividend provides a tangible reward and helps stabilize the balance sheet as the company navigates ongoing revenue challenges. This approach to capital allocation aligns with the new, more predictable profit profile.

Ultimately, management is redefining the playing field. The focus for 2026 is no longer on exceeding margin guidance, but on achieving the higher midterm margin target amid flat revenue growth. The dividend offers a baseline for shareholder returns, enhancing the stock's appeal as the market adjusts to a margin-centric environment.

Key Drivers and Risks: Bridging the Valuation Gap

Closing the gap between medmix's improved profitability and its share price depends on two main factors: validating growth guidance and demonstrating that strategic initiatives can reverse revenue declines.

- Revenue Trends: Investors will closely monitor first-quarter 2026 results to assess whether the company can achieve its guidance of flat to low single-digit organic growth. The 2025 results showed a slight sequential improvement, with second-half revenue up 0.1% over the first. A stronger performance in early 2026 would signal that the new growth baseline is attainable, potentially easing concerns about ongoing revenue weakness.

- Strategic Projects: Progress in the Atlanta-based Surgery and Drug Delivery development initiatives is crucial. Management highlighted advancements in these areas as part of its shift toward healthcare. Success here could diversify medmix's revenue streams beyond the underperforming Beauty and Drug Delivery segments. Tracking milestones and early commercial results will help determine if these projects can offset organic declines.

The main risk remains persistent revenue contraction. While the gross profit margin expanded by 310 basis points to 36.1% in 2025, continued top-line weakness will keep investor focus on this challenge. The stock's valuation is unlikely to reflect improved profitability until medmix demonstrates it can both meet margin targets and stabilize or grow revenue. For now, the gap between expectations and reality persists.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

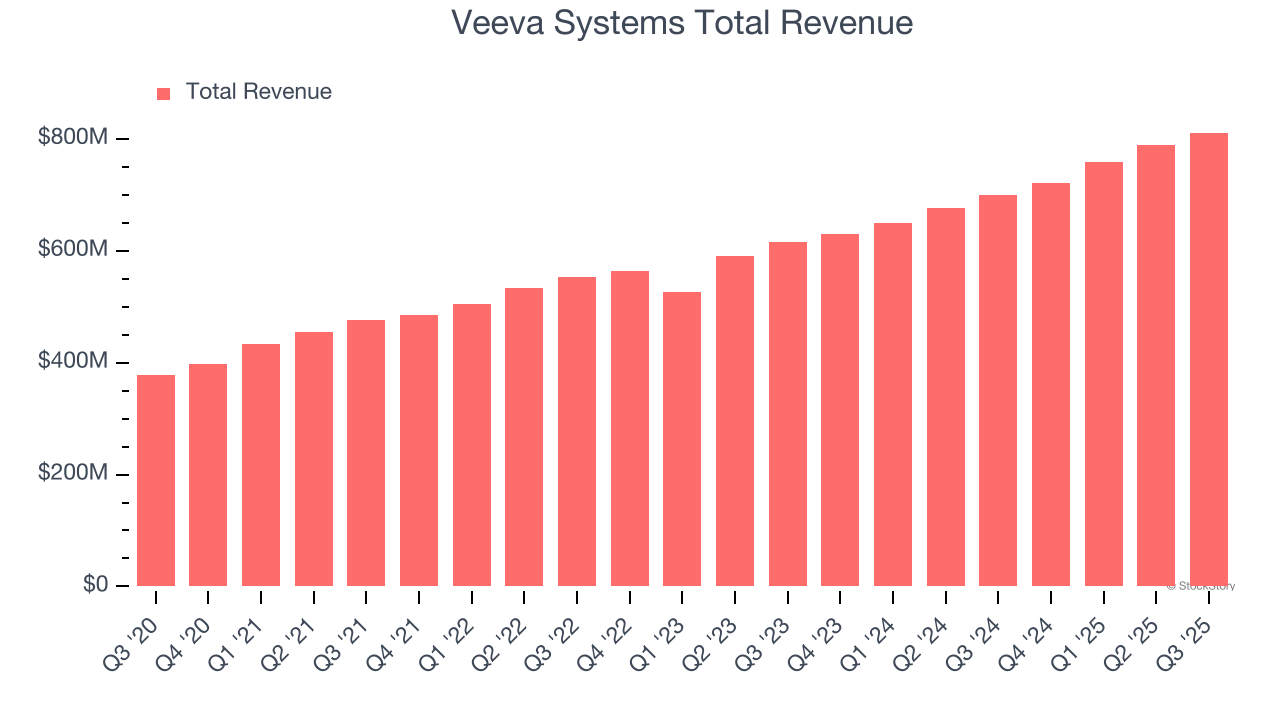

Veeva Systems (VEEV) Reports Q4: Everything You Need To Know Ahead Of Earnings

Bath and Body Works Earnings: What To Look For From BBWI

Earnings To Watch: The Real Brokerage (REAX) Reports Q4 Results Tomorrow

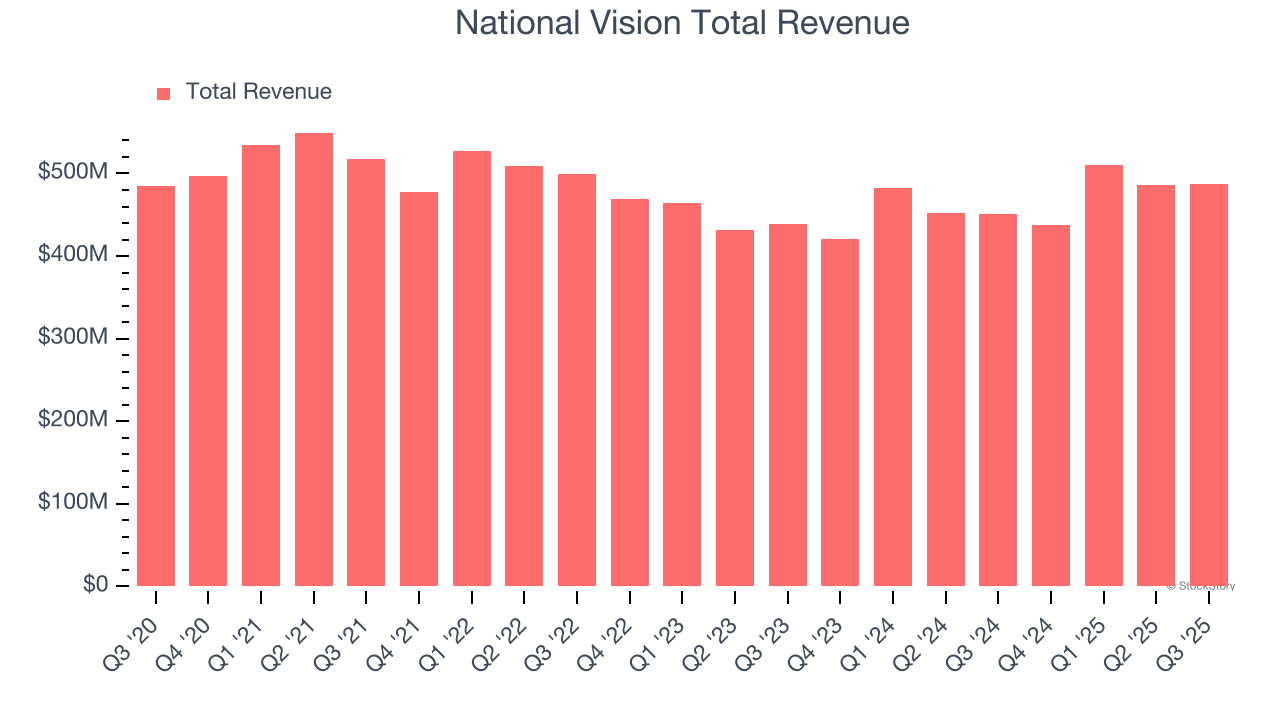

National Vision (EYE) Reports Q4: Everything You Need To Know Ahead Of Earnings