Is the European natural gas crisis just beginning? Morgan Stanley: Current pricing only reflects a 1-2 week interruption. If Qatar halts production for several months, prices could double again!

The European natural gas market is repricing due to geopolitical shocks in the Middle East.

According to Wind Trading Desk, Morgan Stanley’s latest report points out that European natural gas benchmark TTF surged under the combined influence of LNG transport disruptions in the Strait of Hormuz and shutdown news from Qatar’s Ras Laffan facility. However, the current price mainly reflects expectations for a one- to two-week interruption (baseline scenario). In extreme cases, if Ras Laffan’s shutdown extends to several months, TTF could spike to 100 euros, approaching the squeezed market environment of 2022.

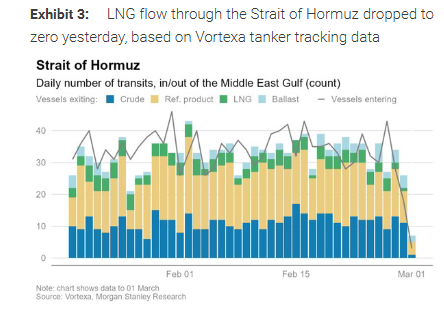

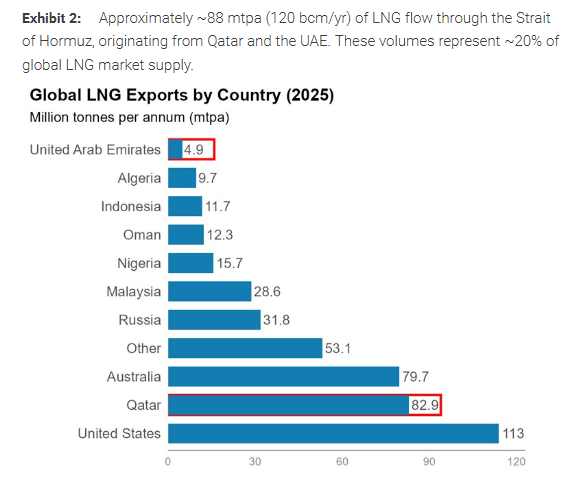

The latest turmoil results from the supply and logistics sides combined. Based on Vortexa tanker tracking data, LNG flow through the Strait of Hormuz once dropped to zero. Together with news about the world’s largest LNG infrastructure in Qatar shutting down, this caused TTF to soar 60% in two days.

In its baseline scenario, Morgan Stanley expects the market to be pricing in “one to two weeks of Gulf LNG export interruption.” The firm raised its short-term TTF estimate to around 45 euros/MWh and believes if Qatar’s output and strait passage recover rapidly, TTF may hover in the 45–50 euros/MWh range in the near term.

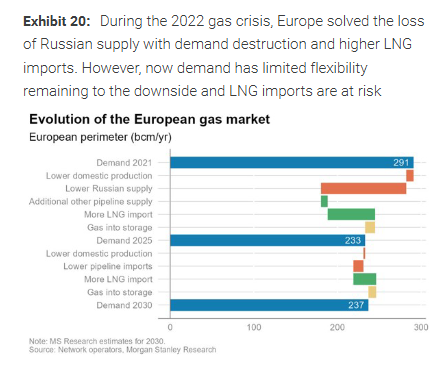

For Europe, Morgan Stanley believes the fundamental backdrop is more robust than in 2022, and Qatar’s LNG only makes up a small part of Europe’s total supply. If Middle East disruptions persist, even if Europe competes with Asia for supply, the supply-demand imbalance would be far less than in 2022.

Strait “standstill” plus Ras Laffan shutdown intensify supply concerns

In its March 3 report, Morgan Stanley stated that around 88 million tonnes (about 120 billion cubic meters/year) of LNG are shipped through the Strait of Hormuz each year, accounting for about 20% of global LNG supply, mainly from Qatar and the UAE. Unlike oil, Qatar and the UAE lack alternative gas export routes; once the strait is nearly impassable for tankers, supply shocks cannot easily be rerouted or mitigated.

What’s more sensitive for the market is the Ras Laffan shutdown itself. Morgan Stanley notes that Ras Laffan has 14 liquefaction trains with an annual capacity of 77 million tonnes, making it the largest LNG export facility in the world. Multiple media outlets reported the shutdown resulted from drone attacks, but energy consulting firm Energy Aspects proposed another explanation: that shipping disruptions combined with limited storage forced QatarEnergy to cut or halt output. Whatever the reason, such a large-scale shutdown is rare in the industry, and the pace of recovery will be a key price driver.

Beyond Qatar, Israel also experienced a supply disruption last weekend. The report says on February 28 the Israeli government ordered the Leviathan and Karish gas fields to temporarily halt production, while Tamar appeared to remain operational. As a result, exports to Egypt and Jordan were paused, with some resumption by March 2. Morgan Stanley estimates the immediate impact on Egypt could be around 200–300 million cubic meters/day. Citing Platts data, the report says Egypt, due to the pipeline gas disruption from Israel, has issued an LNG tender planning to buy 20 cargoes between June and September, with three additional cargoes in March.

Why does TTF react more violently: tight balance, little buffer, hard to reroute

Morgan Stanley offers four explanations for why natural gas is more prone to amplified volatility than oil.

First, fundamentals were “tighter” before the incidents. The report notes the global LNG market was roughly balanced in recent months, with limited new winter supply, while European and Asian demand improved year-on-year. In Europe, stronger heating and power demand and lagging LNG imports kept inventories at 10-year lows.

Second, natural gas is already experiencing tangible supply cuts, not just logistics constraints. Shut downs at Ras Laffan and Israeli gas fields mean available supply decreases, making the impact more visible.

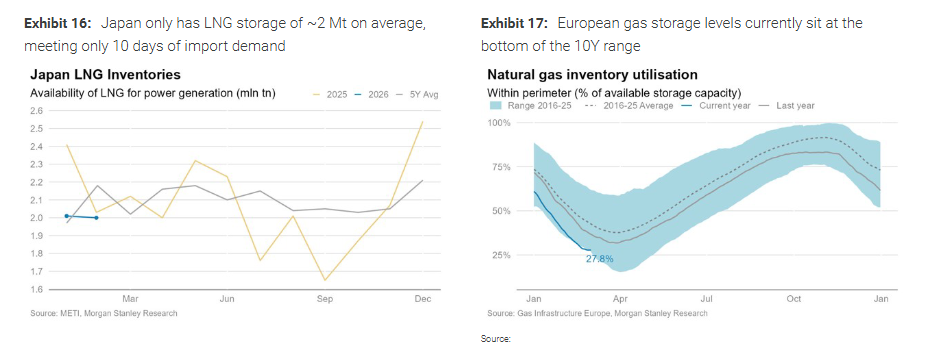

Third, system buffers are thinner and harder to reroute. The report emphasizes LNG storage is already challenging, and major importers have limited reserves: e.g., Japan’s average stocks cover only about 10 days of demand. Simultaneously, Qatar and the UAE lack alternatives to bypass the strait. Europe’s other key supply sources also offer little “spare capacity” — Norwegian and North African pipeline flows are essentially at max output.

Fourth, before the event, TTF was underpricing geopolitical risk. Morgan Stanley estimates that as of February 27, TTF was pricing in just 2–3 euros/MWh of geopolitical premium, implying less than a 10% probability of major disruption — whereas the oil market had priced in a higher probability. The result is a “catch-up” repricing in natural gas once the incident unfolded.

Scenario simulations: Baseline pricing for 1–2 weeks, key is Ras Laffan’s restart window

Morgan Stanley believes the market is currently responding to “Scenario 2”—a one to two week interruption, and treats this as the baseline scenario.

-

Scenario 1 (24–48 hours): If Qatar’s output and exports resume within 48 hours, TTF may fall back to around 35 euros/MWh in two to three weeks. The report notes Energy Aspects believes Qatar could technically restart liquefaction in as little as 3–6 hours, making a fast recovery feasible.

-

Scenario 2 (1–2 weeks, baseline): The report defines this stage’s main impact as a “fleet efficiency shock.” Their calculations show that if an average 18-day voyage is delayed by a week, it is equivalent to a sharp reduction in shipping capacity, effectively losing about 7% of global fleet capacity, or roughly 2.8 Mt/month of deliverable volume. As a result, TTF may fluctuate between 45–50 euros/MWh, JKM around $16–18/MMBtu. Since about 89% of affected volume was originally destined for Asia, Asian restocking will compete more directly with Europe, pushing TTF to higher marginal pricing.

In this baseline scenario, Morgan Stanley estimates Europe could lose about 2.3 million tonnes of LNG supply per month (including diverted volumes to Asia and reduced direct arrivals to Europe), weighing on inventory levels. The report expects that if normalcy is restored by the end of March, inventories could still be replenished to around 70%–75% in the summer, so price pressure is more concentrated at the front end of the curve. TTF still has room to fall in the summer, but risk premia will be harder to eliminate completely.

If Qatar’s shutdown is “prolonged”: 60–80 for one month, multiple months could reach 2022-style squeeze

Morgan Stanley focuses tail risk on the duration of the Ras Laffan shutdown.

-

Scenario 3 (serious interruption for one month): If the strait remains stalled for several weeks and supply from both Ras Laffan and UAE’s Das Island is limited, global LNG monthly supply loss could reach 6.8 Mt. Estimates indicate Europe’s potential monthly supply shortfall could reach about 5.5 million tonnes; TTF may need to rise to 60–80 euros/MWh to trigger demand cuts and rebalance the market.

-

Scenario 4 (Ras Laffan shutdown for several months): The report notes major LNG facilities rarely recover quickly from unscheduled outages, citing historical examples such as Freeport LNG and Hammerfest LNG, where repairs took a long time. With the extent and repair timeline for Ras Laffan still unclear, if the shutdown lasts 2–3 months, Europe would be hampered in restocking gas for summer, and prices may climb above 100 euros/MWh, potentially reaching the highs seen in 2022 if the outage drags on. At the current 45 euros/MWh, prices could “double,” but only if the shutdown stretches from “weeks” to “months” or even a “quarter.”

Supply-demand imbalance far less than 2022; should Europe be less concerned?

For Europe, Morgan Stanley’s core assessment is clear: The Middle East LNG risk in 2026 may approach the “scale” of the 2022 Russia gas cutoff, but the “transmission mechanism” is totally different.

In 2022, Europe lost around 130 billion cubic meters/year of Russian gas, 40% of its supply, a direct supply cutoff crisis. TTF more than doubled, soaring past 200 euros/MWh in summer.

This time, even with a long-term Qatar shutdown, the potential impact is about 120 billion cubic meters/year—similar in scale, but Europe’s direct exposure is only about 4% (Qatar only supplies a small portion of Europe’s total).

The key: 40% of Europe’s supply comes from LNG, which sets the marginal price. If the Middle East disruption persists and LNG is diverted to Asia, even if Europe must pay more to secure cargoes—prices may fluctuate dramatically, but the supply-demand imbalance is far less than 2022.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

2 High-Performing Stocks with Strong Financials and 1 Encountering Challenges

Amgen Inc. (AMGN) is Drawing Interest from Investors: Key Information You Need to Know

Eli Lilly and Company (LLY) is Drawing Interest from Investors: Key Information You Need to Know

Super Micro Computer, Inc. (SMCI) is Drawing Interest from Investors: Key Information You Need to Be Aware Of