Nebius Shares Plummets 4.63% on $880M Volume Ranking 161st as Q4 Earnings Misses and Costs Surge

Market Snapshot

Nebius Group (NBIS) fell 4.63% on March 3, 2026, with a trading volume of $0.88 billion, ranking 161st in market activity that day. The decline followed the release of Q4 2025 financial results, which showed revenue of $227.7 billion, missing forecasts by $19.8 billion (–8%) despite a 547% year-over-year growth. The stock’s premarket drop of 3.75% to $85.29 signaled investor concern over earnings shortfalls and operational challenges.

Key Drivers

The stock’s decline was primarily driven by the Q4 2025 earnings report, which highlighted a stark disconnect between revenue growth and profitability. While revenue surged 547% YoY, the company missed forecasts by 8%, raising questions about its ability to scale sustainably. Operating losses widened significantly in recent quarters, with Q4 2025 reporting an operating income of –$10.8 billion (–$10.795 billion) and a negative EBITDA margin of –46.67%. The income statement data reveals a deteriorating trend: operating income growth collapsed from 541.12% in 2023 to –71.09% in 2025, while net income margins swung from 7.8% in 2023 to –109.6% in 2025.

A critical factor underlying the losses is the rapid expansion of operating expenses. R&D costs jumped from $23.9 billion in 2023 to $41.8 billion in 2025, and selling, general, and administrative (SG&A) expenses grew from $57.5 billion to $125.9 billion over the same period. These outlays, coupled with a 44.1% YoY increase in total revenues to $179.3 billion, suggest the company is prioritizing growth over margin preservation. The gross profit margin also declined from 56.6% in 2023 to 27.4% in 2024 before rebounding to 69.9% in 2025, indicating inconsistent cost control.

The earnings report further highlighted structural inefficiencies. Despite a 547% YoY revenue surge, net income fell to –$19.7 billion in Q4 2025, a 98.2% decline from the prior year. This discrepancy underscores the burden of high operating leverage and the challenges of scaling AI infrastructure. The company’s core AI cloud business, while growing 830% YoY, failed to offset losses in other segments, including AI pilots and automation initiatives. CEO Arkady Volozh’s acknowledgment of “capacity constraints affecting growth” and the need for “real-time automated record checks” signaled ongoing operational hurdles.

Positive developments, such as the approval of a gigawatt-scale AI factory in Independence, Missouri, and a $650 million tax incentive package, were overshadowed by short-term earnings concerns. The factory, projected to deliver long-term benefits through STEM programs and workforce development, may not address immediate profitability issues. Additionally, the company’s cash reserves of $3.7 billion and $834 million in operating cash flow for Q4 2025 suggest liquidity is not a near-term risk, but investors appear focused on earnings execution rather than long-term potential.

The market’s reaction also reflects broader skepticism about Nebius’s ability to maintain its aggressive expansion while achieving profitability. With R&D and SG&A expenses growing at a faster pace than revenue, the company faces pressure to demonstrate that its investments will translate into sustainable margins. The recent 4.63% drop underscores the market’s demand for clearer alignment between growth and profitability, particularly as the AI sector faces increasing competition and margin pressures.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

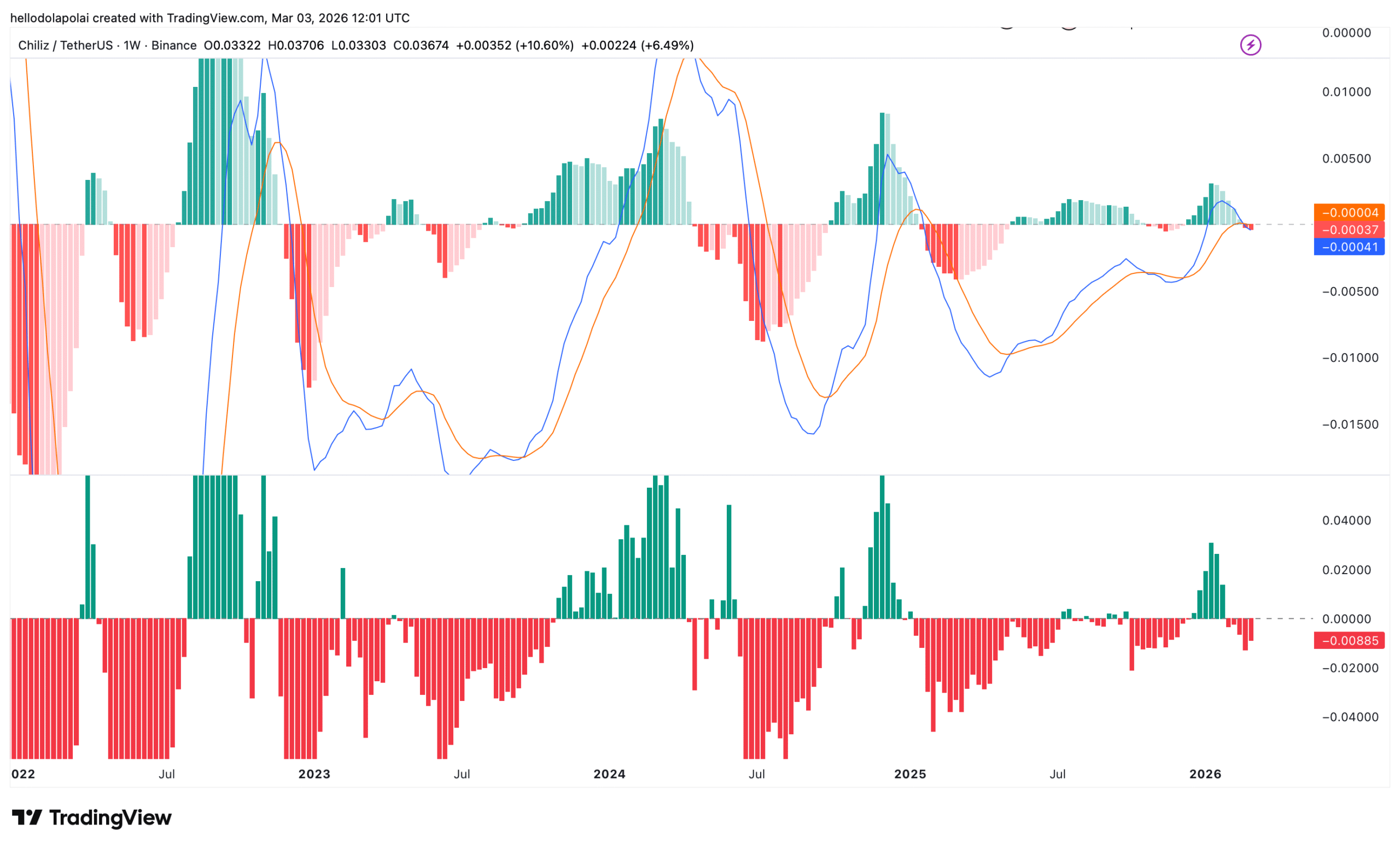

Chiliz nears key resistance: What’s behind CHZ’s fragile rally?

Marvell: Cramer's "Buy the Dip" Alpha vs. The "Lost Deal" Noise

Lumentum’s OFC Catalyst: A Strategic Move Riding the Wave of AI Infrastructure Growth

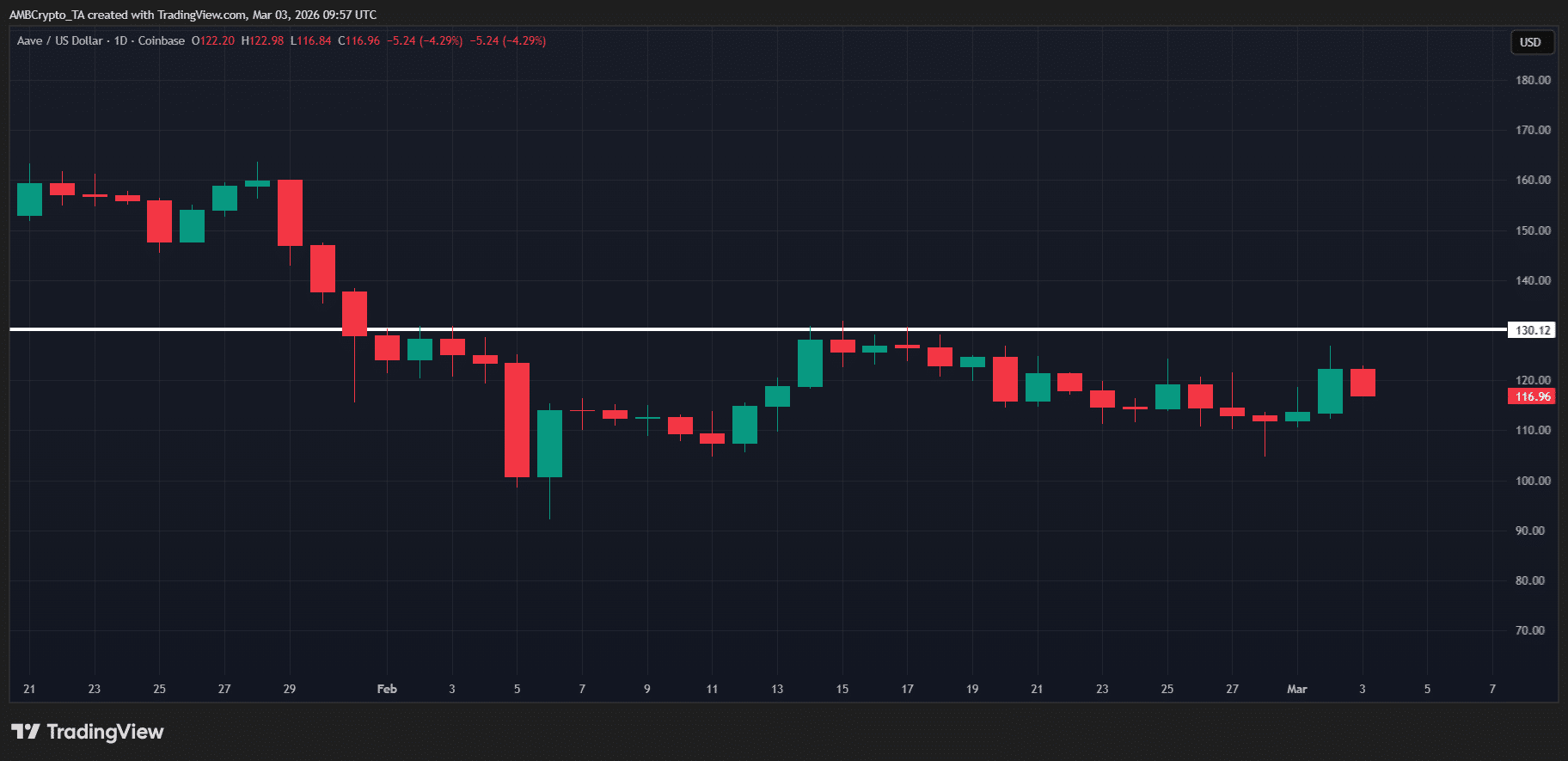

AAVE jumps 7% on $42.5 mln governance boost – Can it break $130?