Marathon Petroleum climbs 1.03% even with a 243rd ranking in market activity, as strong institutional purchasing and better-than-expected earnings fuel positive sentiment

Overview of Marathon Petroleum's Market Performance

On March 3, 2026, Marathon Petroleum (MPC) saw its share price rise by 1.03%, even as trading volume dropped by 25.65% to $0.58 billion, placing it 243rd in market activity rankings. This positive movement stood out against a backdrop of market volatility, with institutional investors and recent earnings reports boosting confidence. The company holds a market capitalization of $59.5 billion, a price-to-earnings ratio of 14.83, and offers a 2.0% dividend yield.

Main Factors Influencing MPC

Institutional Activity and Investor Trust

Recent disclosures show robust institutional involvement in MPC shares. Quantbot Technologies LP and Strive Asset Management LLC entered new positions in the third quarter, while Vanguard Group, Geode Capital Management, and Boston Partners expanded their stakes by double-digit percentages in the second quarter. Norges Bank also holds a substantial $527 million investment. These actions demonstrate strong institutional faith in Marathon Petroleum’s long-term outlook. Currently, over 76% of MPC shares are held by institutional investors, reflecting a broader trend of capital flowing into the energy sector as the refining industry shows resilience.

Strong Earnings and Operational Excellence

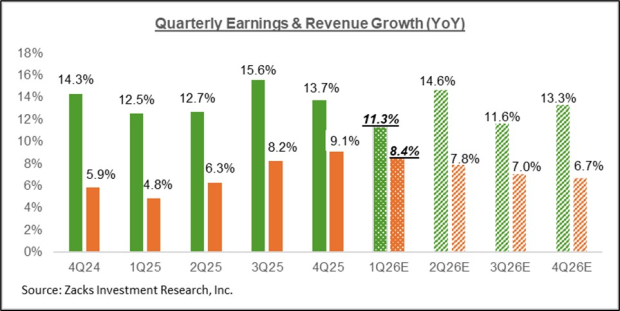

For the fourth quarter of 2025, Marathon Petroleum reported earnings of $4.07 per share, beating expectations by 35.22%. Revenue reached $33.42 billion, exceeding forecasts by 1.7%. The company maintained a 95% refinery utilization rate and achieved $3.5 billion in adjusted EBITDA, highlighting operational strength. Management noted $8.3 billion in cash generated and $4.5 billion returned to shareholders, including a dividend of $1.00 per share. Analysts from Wells Fargo and Raymond James increased their price targets to $217 and $210, respectively, citing robust cash flow and disciplined capital management.

Analyst Perspectives and Strategic Direction

Among analysts, 11 recommend “Buy” and eight suggest “Hold,” though recent reports present mixed views. JPMorgan lowered its price target to $179 due to oil price fluctuations, while Jefferies maintained a “Buy” rating at $205. The average target price stands at $202.19, indicating a possible 2.4% gain from current prices. Marathon’s planned 2026 capital budget for refining is $700 million, a 20% decrease from 2025, signaling a move toward greater cost efficiency in line with CEO Maryann Mannen’s focus on operational control.

Impact of Geopolitical Events and Market Trends

Crude oil prices spiked after supply disruptions in the Middle East on February 6, 2026, leading to a 4.5% intraday jump in MPC shares earlier that week. Analysts attributed this to increased demand for refined products and improved inventory values. Despite these gains, JPMorgan’s downgrade and Wells Fargo’s cautious outlook highlight concerns about short-term oil price corrections, with some forecasts predicting prices could fall to $55 per barrel by 2026. These factors underscore the energy sector’s vulnerability to geopolitical events and broader economic changes.

Insider Activity and Corporate Governance

Recent insider sales, including $10.1 million worth of transactions by Michael J. Hennigan in February 2026, prompted questions about executive sentiment. Marathon’s board clarified that these sales were routine portfolio adjustments and not a sign of operational issues. The company’s dividend payout ratio is 29.96%, with a quarterly dividend of $1.00 announced on February 3, reaffirming its commitment to rewarding shareholders.

Capital Strategy and Market Position

Marathon Petroleum’s emphasis on refining and logistics has enabled it to benefit from tight fuel markets. With institutional investors holding 76.77% of shares and a beta of 0.69, MPC is less volatile than many of its energy sector peers. Recent upgrades from Barclays and UBS reflect confidence in Marathon’s ability to manage cyclical changes through prudent capital allocation. However, a debt-to-equity ratio of 1.27 and an expected earnings per share of 8.47 for 2026 highlight the importance of ongoing cost control, especially in a high-interest-rate environment.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

AU: Indicator of Monthly Household Expenditure, January 2026

Looking Ahead to the 2026 Q1 Earnings Season

Blue Hat Announces an Updated Effective Time for 1-for-50 Reverse Stock Split

PagSeguro Digital Ltd. (PAGS) Tops Q4 Earnings Estimates