Albemarle Stock Drops 7.55% After Mixed Earnings Report Trading Volume Jumps 91% to 550M, Placing 257th Among U.S. Stocks

Market Overview

On March 3, 2026, Albemarle (ALB) experienced a significant drop of 7.55%, closing at $164.73 as the broader market faced declines. Trading activity was robust, with volume soaring by 91.07% to $0.55 billion, placing Albemarle 257th among U.S. stocks by volume. This marked the fourth straight day of losses, leaving the share price 20.03% below its 52-week peak of $206.00 set on February 25. The selloff followed the release of mixed fourth-quarter 2025 results: the company posted a per-share loss of $0.53—missing analyst expectations by 3.92%—while revenue reached $1.4 billion, surpassing forecasts by 4.48%.

Main Factors Impacting Performance

The sharp decline in Albemarle’s stock price was largely driven by investor concerns over its Q4 2025 earnings. Despite revenue exceeding projections, the company’s $0.53 per-share loss was worse than the anticipated $0.51, highlighting ongoing operational hurdles. The revenue beat did little to offset worries about a -10.74% net margin, which management attributed to ongoing restructuring efforts, including the temporary shutdown of the Kemerton facility. The company also reported $450 million in productivity improvements and $700 million in free cash flow, but these positives were overshadowed by sluggish lithium demand and margin compression.

Albemarle’s losses occurred alongside a general market downturn, with the S&P 500 and Dow Jones Industrial Average falling 0.94% and 0.83%, respectively. While Albemarle underperformed compared to peers like Celanese Corp. (which rose 3.20%), its decline was consistent with broader weakness among energy transition metals and specialty chemical stocks. Analysts emphasized Albemarle’s exposure to lithium market trends, noting that global demand is expected to reach 2.2 million tons in 2026. As the world’s largest publicly traded lithium producer, Albemarle remains well-positioned for future growth, but faces immediate challenges from stagnant lithium volumes and a focus on disciplined capital spending.

Recent strategic decisions have also shaped investor sentiment. Management has shifted toward “disciplined growth,” pausing certain expansion projects and concentrating on higher-margin conversion capacity. The decision to idle the Kemerton plant reflects a move to rein in costs following a correction in lithium prices after 2024. Additionally, Albemarle declared a quarterly dividend of $0.405 per share, payable on April 1, with a payout ratio of -28.17%, signaling financial resilience despite current losses. In recent months, Bank of America and UBS have upgraded the stock to “buy,” citing robust long-term demand for lithium and Albemarle’s strong competitive advantages in assets and innovation.

Despite short-term obstacles, optimism remains for Albemarle’s future. The company’s diversified global operations—including hard-rock spodumene mining in Australia, brine extraction in Chile, and the Silver Peak facility in the U.S.—position it to benefit from evolving supply chains and the expansion of energy storage. Albemarle anticipates a 15% compound annual growth rate in energy storage sales over the next five years, in line with industry trends. While near-term risks persist, such as the potential restart of the Kings Mountain project in North Carolina, Albemarle’s emphasis on capital efficiency and productivity improvements could help stabilize its performance.

Analyst Views and Future Outlook

Expert opinions on Albemarle’s short-term trajectory remain mixed. UBS and Bank of America have recently raised their price targets to $205 and $190, respectively, while Mizuho and others maintain a “neutral” stance. Technical analysis presents a complex picture: the stock’s RSI stands at 53.47, with a bearish stochrsi, but moving averages indicate some positive momentum. Albemarle’s ability to manage lithium price fluctuations and maintain disciplined capital allocation will be crucial in the quarters ahead. As global demand for lithium and energy storage materials continues to rise, the company’s long-term success will depend on its capacity to balance cost control with strategic growth initiatives.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

QSR Shares See Modest Rise Following Strategic Shift and Analyst Upgrades, Even as Trading Volume Ranks 463rd

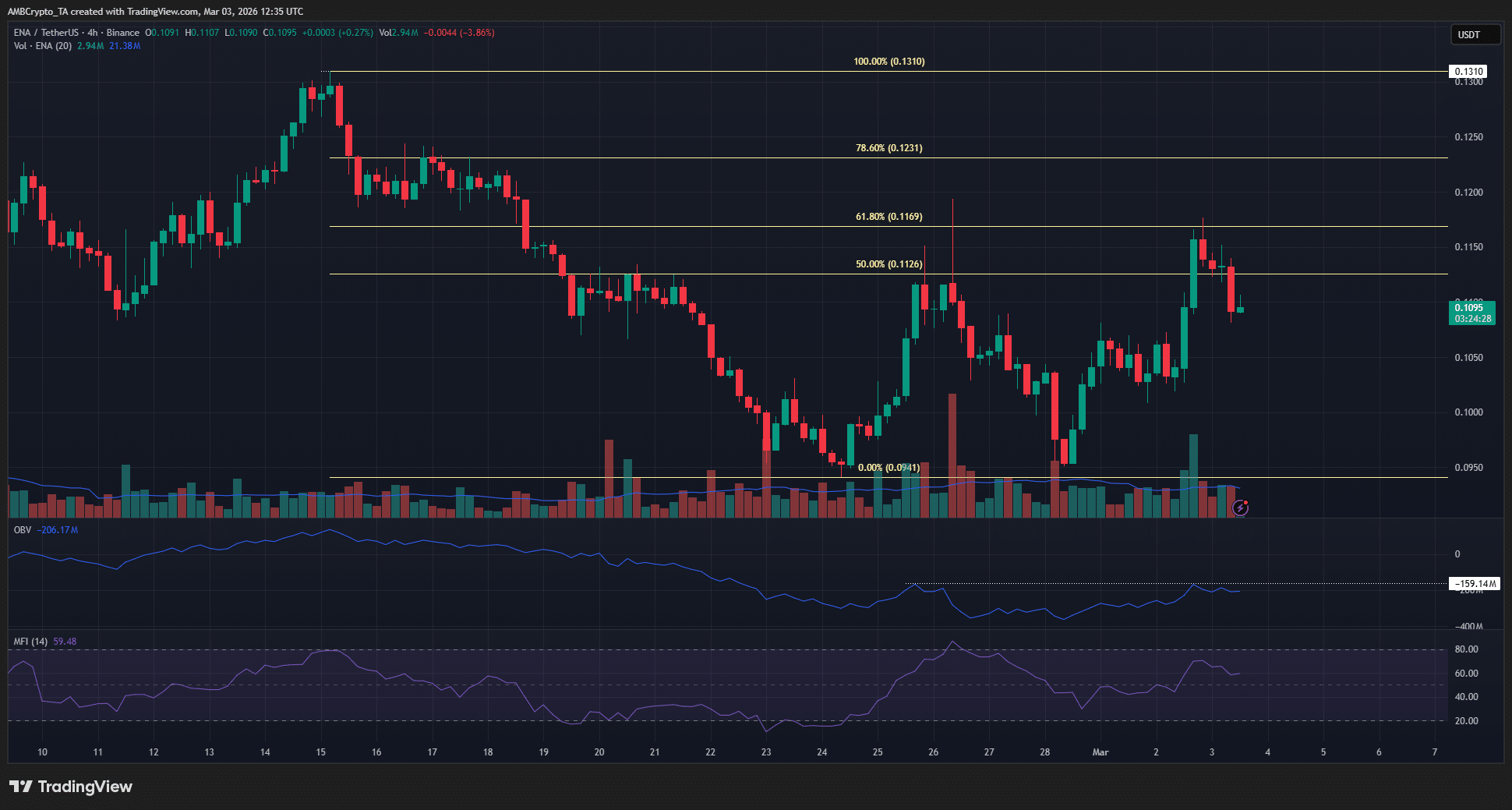

Ethena’s retracement rally, explained: Heavy volume, light conviction

DTE Energy Experiences 56% Jump in Volume, Moving Its Stock to 490th Place in Daily Trading Rankings

ASE Technology's 7.81% Plunge Amid Earnings Miss and Institutional Splits as $320M Volume Surges to Rank 446th