Martin Marietta Shares Fall 3.29% on Q4 Earnings Miss Despite Strong 2025 Performance as $350M Volume Ranks 406th and Acquisition Drives Long-Term Optimism

Market Snapshot

Martin Marietta Materials (MLM) closed 3.29% lower on March 3, 2026, following a disappointing Q4 2025 earnings report. The stock traded with a volume of $350 million, ranking 406th in market activity for the day. The decline came despite a strong full-year 2025 performance, where the company reported $5.7 billion in revenue—a 7% increase—alongside 13% growth in gross profit to $1.8 billion and a 173-basis-point margin expansion to 31%. However, Q4 results fell short of expectations, with earnings per share (EPS) of $4.62 versus the forecasted $4.85 and revenue of $1.53 billion against the expected $1.66 billion, triggering a 4.68% pre-market price drop.

Key Drivers

The immediate catalyst for the stock’s decline was the Q4 2025 earnings miss. Investors reacted negatively to the shortfall in both EPS and revenue, which fell 4.74% and 7.83% below estimates, respectively. This underperformance was exacerbated by ongoing challenges in the private construction sector, which the company acknowledged as a drag on demand. Despite these headwinds, Martin MariettaMLM-- highlighted record operational and safety performance in 2025, underscoring its resilience in a mixed market environment. The company’s full-year results demonstrated robust gross margin expansion and strong aggregates segment performance, with revenue up 11% and gross profit increasing 16%.

A critical factor supporting long-term optimism was the completion of the Premier Magnesia acquisition. This strategic move added to the company’s portfolio of value-added materials, diversifying its offerings beyond traditional aggregates. The acquisition aligns with Martin Marietta’s focus on high-margin products and positions the firm to capitalize on infrastructure demand, which CEO Ward Nye described as “strong.” The company’s 2026 guidance further reinforced this outlook, with forecasts of $2.49 billion in adjusted EBITDA, 2% shipment growth, and low double-digit gross profit growth. These projections suggest confidence in maintaining profitability despite macroeconomic uncertainties.

Analyst sentiment remained cautiously optimistic, with a consensus “Hold” rating from 17 firms. While one analyst issued a “Sell” recommendation, eight maintained “Buy” ratings, and eight advocated “Hold.” The average 12-month price target of $697.1250 reflects a 6.7% premium to the March 3 closing price of $653.39. Notably, Citigroup and UBS Group recently raised their price targets, citing the company’s strategic acquisitions and margin resilience. However, some firms, such as Loop Capital and Wells Fargo, tempered expectations by downgrading or lowering their price objectives, reflecting divergent views on the sustainability of infrastructure-driven demand.

Hedge fund activity also signaled mixed signals. Atlantic Union Bankshares Corp and HB Wealth Management LLC significantly increased their stakes in Q3 2025, while institutions like National Pension Service maintained substantial holdings. Institutional ownership now accounts for 95.04% of the company’s shares, indicating a long-term bet on its market position. The company’s financial metrics further justified this confidence, with a 52-week high of $710.97 and a trailing P/E ratio of 35.45, suggesting growth expectations outweigh current valuation concerns.

Looking ahead, Martin Marietta’s ability to navigate private construction challenges while leveraging infrastructure tailwinds will be pivotal. The company’s 2026 guidance assumes stable shipment growth and continued margin expansion, but execution risks remain. With a 1.7% dividend yield and a debt-to-equity ratio of 0.53, the firm appears well-positioned to balance growth initiatives with shareholder returns. However, the recent earnings miss underscores the need for improved forecasting accuracy, particularly in volatile construction markets. Investors will likely monitor Q1 2026 results and infrastructure spending trends to gauge the company’s ability to sustain its momentum.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Drugmaker Aspen targets Mounjaro approval in sub-Saharan Africa this year

Solana risks repeating 95% crash seen in 2022 while funding in Mutuum Finance nears $21m

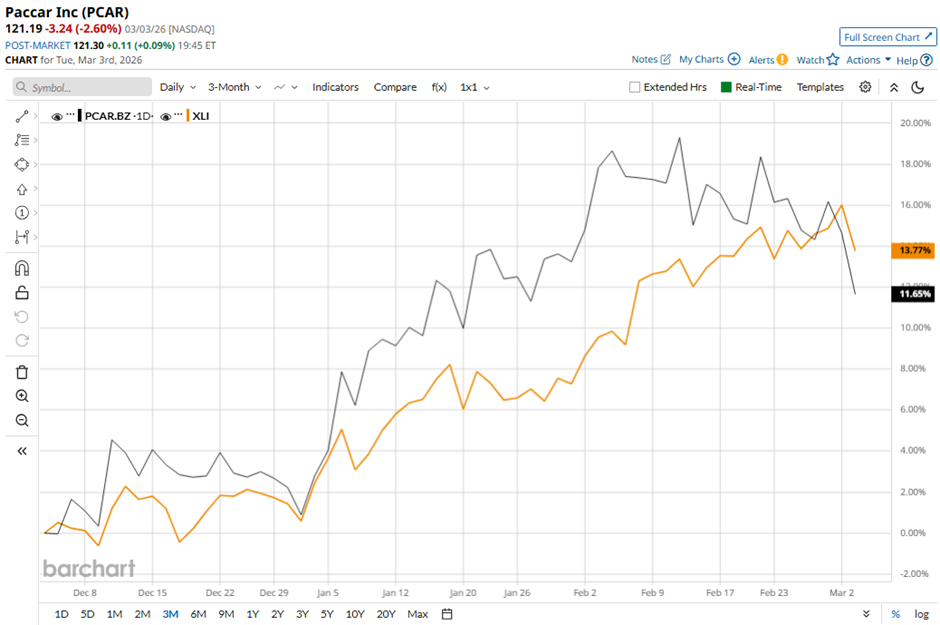

PACCAR Shares: Is PCAR Lagging Behind the Broader Industrial Market?

GenTwo hires Vontobel’s blockchain chief for digital asset expansion