Herbalife (HLF): Should You Buy, Sell, or Hold After Q4 Results?

Herbalife’s Recent Performance: A Closer Look

Herbalife has experienced an impressive rally over the past six months, with its stock price soaring by 79.4% to reach $18.10. This surge has been fueled in part by strong quarterly earnings, prompting investors to consider their next steps.

Is now the right time to invest in Herbalife, or could it pose a risk to your investment portfolio?

Why We’re Not Enthusiastic About Herbalife

Despite the recent momentum, our outlook on Herbalife remains cautious. Below are three key reasons we’re not optimistic about HLF, along with a stock we find more appealing.

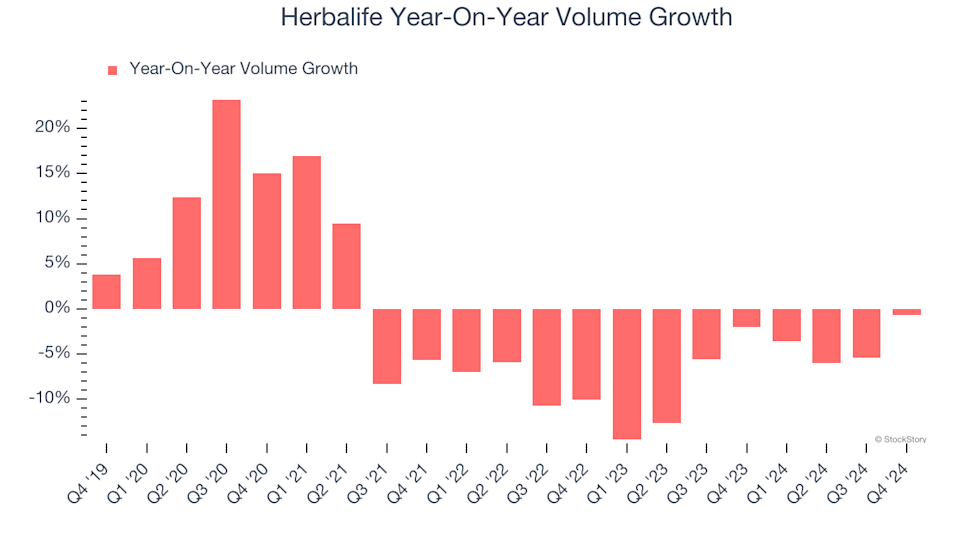

1. Declining Demand Reflected in Lower Sales Volumes

Revenue growth in consumer staples is driven by both pricing and the number of units sold. While both factors matter, volume is especially crucial—there’s a limit to how much consumers will pay for everyday items, and they can easily switch to generic alternatives if prices rise too high.

Herbalife’s average quarterly sales volumes have dropped by 3.9% over the past two years. This decline is concerning, as demand for staple products is usually steady.

Herbalife Year-On-Year Volume Growth

2. Modest Revenue Growth Forecasts

Wall Street’s revenue projections offer a glimpse into a company’s future prospects. While forecasts aren’t always spot-on, accelerating growth tends to lift valuations and share prices, whereas slowing growth can have the opposite effect.

Analysts expect Herbalife’s revenue to increase by just 4.3% over the next year. Although this suggests some improvement from new product launches, the growth rate still lags behind the industry average.

3. Earnings Per Share on the Decline

Tracking changes in earnings per share (EPS) over time reveals whether a company’s additional sales are translating into profits. Sometimes, revenue can rise due to heavy spending on marketing, which doesn’t always lead to sustainable earnings.

Unfortunately, Herbalife’s EPS has fallen by an average of 14.4% per year over the last three years—an even steeper drop than its revenue. This indicates the company has struggled to manage its fixed costs amid shrinking demand.

Herbalife Trailing 12-Month EPS (Non-GAAP)

Our Verdict

While Herbalife isn’t a fundamentally weak business, it doesn’t meet our standards for quality. Following its recent rally, the stock trades at a forward P/E of 7.8 (or $18.10 per share), which is a reasonable valuation. However, we remain skeptical about the company’s prospects and believe there are more promising investment opportunities available. For example, consider a leading digital advertising platform thriving in the creator economy.

Our Preferred Stocks Over Herbalife

DISCOVER: 9 Top Stocks That Consistently Outperform the Market

The most successful stocks don’t just beat the market once—they do it repeatedly. These companies are distinguished by strong revenue growth, increasing free cash flow, and exceptional returns on capital. The market has already recognized their strengths.

But according to our AI-driven analysis, the opportunity isn’t over yet. See which nine stocks made our list this week—completely free.

Our selections include household names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Tecnoglass, which delivered a remarkable 1,754% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

What's Going On With ASP Isotopes Stock?

DICK'S Q4 Earnings on the Cards: Is It Poised to Beat Expectations?

Subsea7 Expands Sakarya Project Scope With New TP-OTC Order