3 Reasons Why BLDR Carries Risk and One Alternative Stock Worth Considering

Builders FirstSource Stock Faces Significant Decline

Over the past half-year, Builders FirstSource has seen its share price drop by 31.8%, now trading at $97.70 per share. This downturn has been influenced in part by weaker-than-expected quarterly results, prompting investors to reconsider their positions.

Is this a buying opportunity for Builders FirstSource, or should investors proceed with caution before adding it to their portfolios?

Why We Expect Builders FirstSource to Lag Behind

Even though the stock is now more affordable, our confidence in Builders FirstSource remains low. Below are three key reasons we believe there are more attractive alternatives to BLDR, along with a stock we prefer.

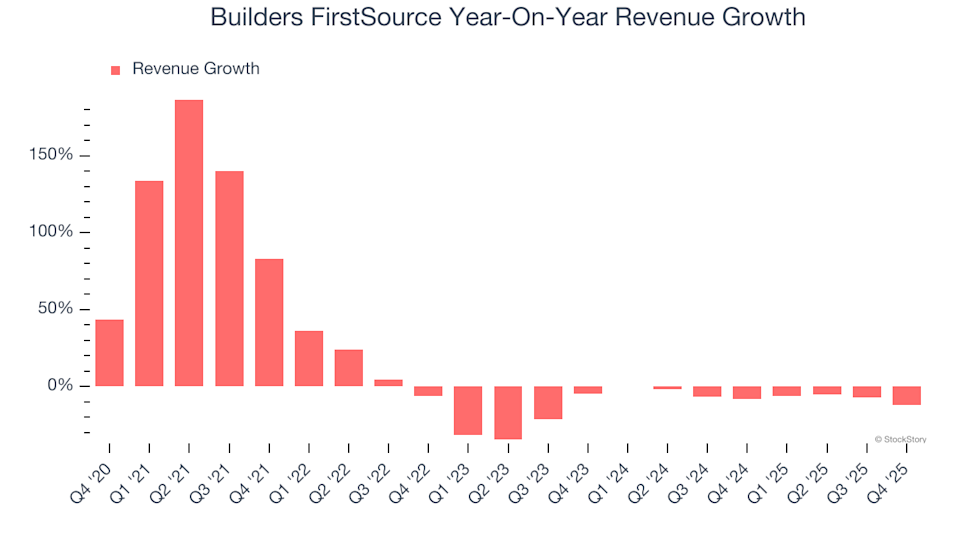

1. Revenue Is on the Decline

While long-term growth is crucial, focusing solely on historical performance can overlook recent shifts in the industrial sector. Builders FirstSource has deviated from its five-year trajectory, with annual revenue shrinking by an average of 5.7% over the past two years.

Builders FirstSource Year-On-Year Revenue Growth

2. Earnings Per Share Have Fallen Sharply

Monitoring short-term EPS trends can reveal emerging challenges or opportunities for a company. Unfortunately, Builders FirstSource’s EPS has dropped even more steeply than its revenue, falling 31.4% over the last two years. This suggests the company has struggled to adapt to reduced demand.

Builders FirstSource Trailing 12-Month EPS (Non-GAAP)

3. Declining ROIC Signals Ineffective New Investments

Return on invested capital (ROIC) measures how efficiently a company generates operating profit from its capital base. While high returns are desirable, the direction of ROIC often has a bigger impact on stock performance. Builders FirstSource has experienced a notable decrease in ROIC in recent years. Although management has made strong moves in the past, the downward trend may indicate a lack of lucrative growth opportunities.

Builders FirstSource Trailing 12-Month Return On Invested Capital

Our Verdict

Builders FirstSource does not meet our criteria for a high-quality investment. After its recent drop, the stock trades at a forward P/E of 16.8 (or $97.70 per share). While this valuation isn’t excessive, we don’t see compelling upside at this time. We believe there are stronger opportunities available. Consider exploring instead.

Stocks We Prefer Over Builders FirstSource

ONE MORE THING: This Week’s Top 6 Stock Picks. The current market is quickly distinguishing quality stocks from overpriced ones, with AI-driven volatility shaking up entire sectors. In such a rapidly changing environment, you need more than just a list of solid companies.

Our AI-powered system previously identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia before its 1,178% climb. Every week, it highlights six new stocks that meet the same rigorous standards.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Consumer Stocks That Make Us Hesitate

Broadcom Locks Key AI Chip Supply Through 2028

Maris-Tech Announces $2.0 Million Registered Direct Offering

Robinhood Ventures Fund I (RVI) Announces Pricing of Initial Public Offering