2 Things to Appreciate About CR (and 1 That’s Less Favorable)

Crane Stock Performance Overview

Currently, Crane is trading at $200.81 per share and has closely mirrored the broader market, posting an 8.5% gain over the past six months. In comparison, the S&P 500 has increased by 5.7% during the same period.

Wondering if now is a good opportunity to invest in CR?

What Makes CR Stock a Topic of Discussion?

Headquartered in Connecticut, Crane (NYSE:CR) is a multifaceted manufacturer specializing in engineered industrial solutions, including fluid management systems and aerospace technology.

Key Strengths of Crane

1. Impressive Revenue Growth Forecast

Wall Street’s revenue projections offer insight into a company’s future prospects. While forecasts aren’t always precise, rapid growth often leads to higher valuations and stock appreciation, whereas slower growth can have the opposite effect—though some deceleration is expected as companies expand.

Analysts anticipate that Crane’s revenue will climb by 24.5% over the next year, a significant turnaround from the 3.9% annualized decline seen over the past five years. This optimistic outlook suggests that Crane’s latest offerings are expected to drive stronger sales growth.

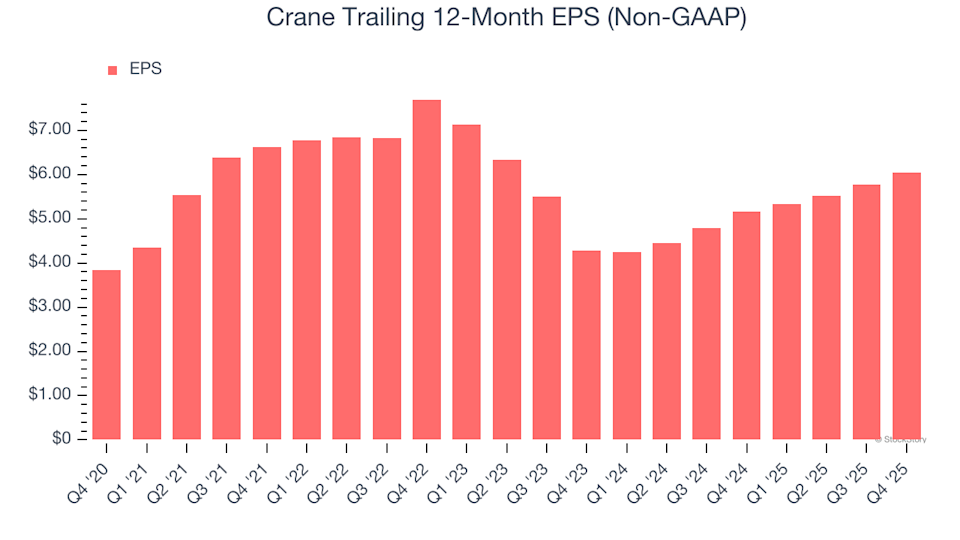

2. Consistent EPS Growth

Examining long-term earnings per share (EPS) trends helps determine if additional sales are translating into real profits, as revenue can sometimes be artificially boosted by heavy marketing spend.

Over the last five years, Crane’s EPS has grown at a compounded annual rate of 9.5%, despite a 3.9% annualized drop in revenue. This indicates that management has effectively adjusted costs to navigate a challenging demand environment.

Crane Trailing 12-Month EPS (Non-GAAP)

Potential Concern: Sluggish Organic Growth

Organic Growth Points to Softer Demand in Core Segments

To better assess companies in the General Industrial Machinery sector, it’s helpful to look at organic revenue, which strips out the effects of acquisitions, divestitures, and currency fluctuations—factors that can distort the true performance of the underlying business.

Crane’s organic revenue has grown by an average of 6.6% year-over-year over the past two years. This is slightly below the industry average and may indicate a need for enhancements in product offerings, pricing strategies, or market approach, potentially adding operational complexity.

Crane Organic Revenue Growth

Bottom Line

While Crane’s strengths appear to outweigh its weaknesses, the question remains: with shares at $200.81 and a forward P/E of 30.6, is it the right time to invest?

Other Stocks Worth Considering

DON’T MISS: This Week’s Top 6 Stock Picks. The current market is quickly distinguishing high-quality stocks from overpriced ones, with AI-driven shifts impacting entire sectors unexpectedly. In such a dynamic environment, you need more than just a list of promising companies.

Our AI-powered system identified Palantir before its 1,662% surge, AppLovin ahead of its 753% rally, and Nvidia prior to its 1,178% climb. Each week, it highlights six new stocks that meet the same rigorous criteria.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Sentio Partners Chainbase to Build AI-Ready On-Chain Data Infrastructure

New Japanese Payment System Launches on XRP Ledger to Solve Last Friction in TradFi

Algonquin Power & Utilities: Fourth Quarter Earnings Overview

2 Medium-Sized Companies That Deserve Your Notice and 1 We Consider Risky