3 Reasons Why CNC Carries Risks and One Alternative Stock Worth Considering

Centene’s Recent Stock Surge: What Should Investors Do?

Over the past half-year, Centene’s stock has soared by 52.4%, reaching $43.66 per share. This impressive climb may leave investors questioning their next move.

Is this a good opportunity to purchase Centene shares, or should you exercise caution before adding it to your portfolio?

Why We’re Not Enthusiastic About Centene

Despite the recent upswing, we’re choosing to stay on the sidelines for now. Here are three reasons we’re steering clear of CNC, along with a stock we prefer instead.

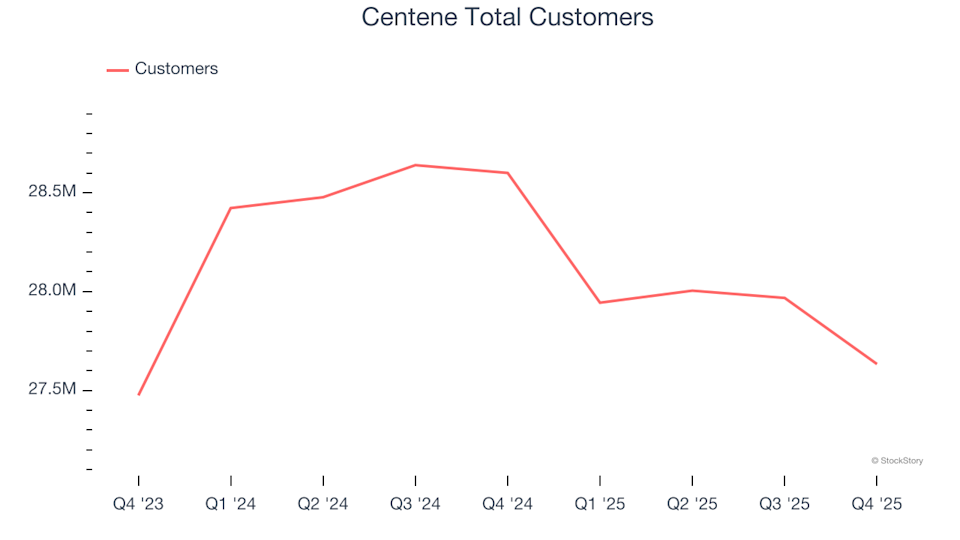

1. Customer Growth Has Stalled

Revenue expansion typically relies on both attracting more customers and increasing the average revenue per customer. A growing client base creates more opportunities for upselling, while higher spending per customer reflects successful sales strategies.

However, Centene’s customer numbers have remained stagnant over the past two years, with the latest quarter showing 27.63 million clients. This lack of growth suggests difficulties in securing new contracts and may indicate rising competition or a saturated market.

Centene Total Customers

2. Declining Earnings Per Share

We monitor long-term changes in earnings per share (EPS) to assess whether a company’s growth is translating into profitability.

Unfortunately, Centene’s EPS has dropped by an average of 16.3% annually over the past five years, even as revenue increased by 11.9%. This means that, despite higher sales, the company’s profitability per share has diminished.

Centene Trailing 12-Month EPS (Non-GAAP)

3. Falling ROIC Signals Weak Returns on New Investments

Return on invested capital (ROIC) measures how efficiently a company generates operating profit from the capital it has raised through debt and equity.

While high returns are attractive, it’s the direction of ROIC that often surprises investors and impacts share prices. In Centene’s case, ROIC has dropped sharply in recent years. Combined with already modest returns, this trend suggests that lucrative growth opportunities are scarce.

Centene Trailing 12-Month Return On Invested Capital

Our Verdict

Centene is not a poor company, but it doesn’t make our list of top picks. After its recent rally, the stock is trading at a forward P/E of 14.7 (or $43.66 per share). While this valuation seems reasonable, we lack conviction in Centene’s prospects and believe there are better opportunities available. For example, consider one of our top digital advertising selections.

Stocks We Prefer Over Centene

ONE MORE THING: Top 5 Growth Stocks. The most successful stocks often share a common trait: explosive revenue growth. Companies like Meta, CrowdStrike, and Broadcom were all identified early by our AI, delivering returns of 315%, 314%, and 455%, respectively.

Discover which five stocks are being highlighted this month—completely free.

Our list has included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which achieved a 351% five-year return. Start your search for the next big winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

GSR withdrew 3000 ETH from an exchange 3 hours ago

Olenox Industries Shares Positive Field Reports as Production Stabilizes

Vail Resorts Set to Announce Q2 Results: What Could This Mean for the Stock?