VOYA Shares Priced Below Industry Average at 0.98X: Is Now a Good Entry Point?

Voya Financial: Stock Valuation and Industry Comparison

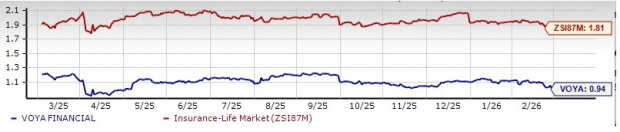

Voya Financial, Inc. (VOYA) is currently trading below the average valuation of its peers in the life insurance sector. Its forward price-to-book ratio stands at 0.94, which is notably less than the industry average of 1.81, the finance sector’s 4.24, and the S&P 500’s 8.31. VOYA has earned an ‘A’ Value Score from Zacks, highlighting its appeal among value-oriented investors.

The company boasts a market cap of $6.43 billion, with an average trading volume of 900,000 shares over the past quarter. VOYA has surpassed earnings expectations in three out of the last four quarters, with an average earnings surprise of 13.09%.

Other companies such as Reinsurance Group of America (RGA), Lincoln National Corporation (LNC), and Manulife Financial Corp (MFC) are also trading below the industry’s average valuation.

Recent Stock Performance

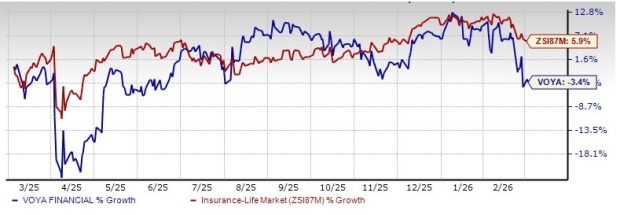

Over the past year, Voya Financial’s share price has declined by 3.4%, while the broader life insurance industry has seen a 5.9% increase during the same period.

Growth Outlook for VOYA

Analyst consensus from Zacks projects Voya’s earnings per share to rise by 11.4% year-over-year in 2026, with revenues expected to reach $1.39 billion, reflecting a 3.6% increase. Looking ahead to 2027, earnings and revenues are forecasted to grow by 16.3% and 6.1%, respectively, compared to 2026 estimates. Over the past five years, VOYA’s earnings have expanded by 8.8% annually, outpacing the industry average of 8.4%. The company’s long-term earnings growth rate is anticipated to be 15.1%.

Analyst Price Targets Indicate Potential Upside

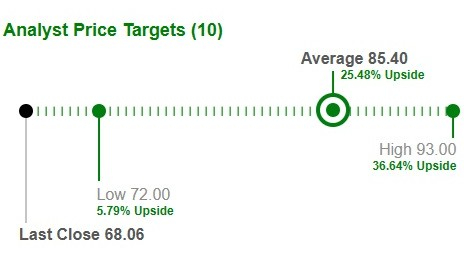

Ten analysts covering VOYA have set an average price target of $85.40 per share, suggesting a possible upside of 25.4% from the most recent closing price.

Key Drivers Supporting VOYA’s Performance

VOYA’s strong results are supported by robust performance across its Retirement, Investment Management, and Employee Benefits divisions. These segments are characterized by high growth, capital efficiency, and attractive returns, reinforcing the company’s competitive position.

- Retirement: Growth is fueled by increased revenues from acquired OneAmerica assets, favorable market trends, higher alternative investment income, and effective portfolio management. The segment continues to deliver margins above long-term targets, supporting higher fee and spread income.

- Investment Management: This segment benefits from strong market performance, increased fee-based revenues, and disciplined cost control. A strategic partnership with Allianz Global Investors has further enhanced scale and diversification.

- Employee Benefits: The segment is seeing improved results due to the absence of prior unfavorable claim developments, a smaller business block, lower premium-related expenses, and prudent expense management.

VOYA maintains a solid capital position, generating over $0.8 billion in excess capital in 2025—about 76% of after-tax adjusted operating earnings. As of December 31, 2025, the estimated combined RBC ratio was 413%.

Capital Allocation Strategy

VOYA’s operational strength enables it to allocate capital effectively to enhance shareholder value. Beyond investments in wealth management, the company uses surplus capital for share repurchases. As of the end of 2025, VOYA had $562 million remaining for buybacks. The company plans to return between $100 million and $150 million to shareholders each quarter in 2026 through dividends and repurchases, subject to market conditions.

Potential Risks

Despite its strengths, VOYA faces rising expenses related to policyholder benefits, credited interest, operating costs, and debt servicing. If revenue growth does not outpace these increasing costs, profit margins could come under pressure.

Summary and Investment Perspective

Voya Financial is well-positioned for continued growth, supported by higher investment income, favorable equity markets, positive net flows, strong retention, and strategic alliances. The company’s financial flexibility and disciplined capital management further strengthen its outlook.

With a history of reliable dividends, solid growth forecasts, positive analyst sentiment, and attractive valuation, VOYA remains a compelling hold for investors.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Loar's M&A Surge: Is the Deal Story Already Priced In?

RIVER tops crypto gains with 34% surge – But ONE zone could end it fast