Goldman Sachs, JPMorgan map scenarios on the Strait of Hormuz, Brent crude, OPEC+: closure duration sets risk premia and spillovers to inflation and EM FX.

Will a Strait of Hormuz closure trigger a Brent crude spike?

A closure of the Strait of Hormuz would constrain seaborne flows and elevate Brent crude via a geopolitical risk premium. The magnitude depends on disruption severity, duration, and how quickly ships and insurance markets normalize.

Short interruptions often spark brief spikes that fade as flows resume. Sustained or severe closures are the scenarios that push prices toward triple digits in institutional models. Rerouting, OPEC+ spare capacity, and strategic reserve releases could soften, but not fully offset, lost throughput at the chokepoint.

Why it matters now: pricing risk, OPEC+ levers, immediate impacts

Pricing risk has intensified alongside regional tensions. As crude rallied, U.S. equity benchmarks fell, with the S&P 500 down about 2.18%, the Dow 2.27%, and the Nasdaq 100 also lower. That pattern reflects a growth and inflation scare.

OPEC+ retains levers, including quota adjustments and spare capacity. Governments can authorize Strategic Petroleum Reserve draws. These tools can cap the risk premium temporarily, though logistics and maritime insurance constraints can slow relief.

Inflation is the near-term macro channel. Higher crude and freight costs typically feed into gasoline and dining bills in import-dependent cities. Central banks may face a trade-off between disinflation progress and growth risks.

Duration remains the dominant variable across scenarios. If a closure extends from days into weeks, the risk premium tends to harden and hedging demand can climb. “If the disruption lasts weeks or months rather than days, we definitely see a scenario possible of $100/barrel,” said Jorge Leon, Head of Geopolitical Analysis at Rystad Energy.

Expert scenarios and market impacts to monitor

Forecasts compared: Goldman Sachs, JPMorgan, Wood Mackenzie, Citi

Goldman Sachs estimates that a full one-month closure could add roughly $10–15 a barrel absent offsets, with a six-week halt implying about an $18 real-time risk premium; under more severe disruptions, it has flagged a brief move near $110. JPMorgan’s worst-case pairs a full closure with broader escalation, mapping to $120–130, and assigns roughly 20–25% probability to a full disruption. Wood Mackenzie expects prices to exceed $100 if tanker flows are not restored quickly and notes planned OPEC+ increases would be largely ineffective if the strait stays blocked. Citi’s recent commentary keeps Brent in an $80–90 range under continued disruption, trending toward $100+ if supply chain issues persist.

Market impacts: inflation, gasoline, equities, and EM currencies

If Brent crude holds higher, headline inflation could re-accelerate through fuel, freight, and food. Retail gasoline tends to lag by weeks, then catch up. Import-heavy economies can see wider trade deficits and weaker currencies.

Equities usually rotate toward energy while broader indices de-rate on margin pressure. Airlines and chemicals often underperform. Emerging-market FX such as India’s rupee can soften when oil import costs rise, especially if hedging cover is limited.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

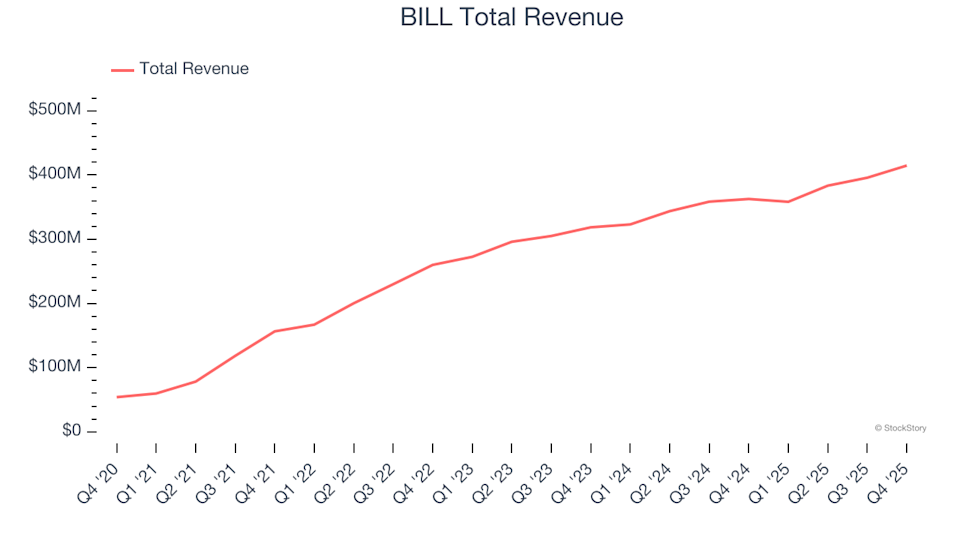

Finance and HR Software Stocks Q4 Overview: Comparing BILL (NYSE:BILL) With Its Competitors

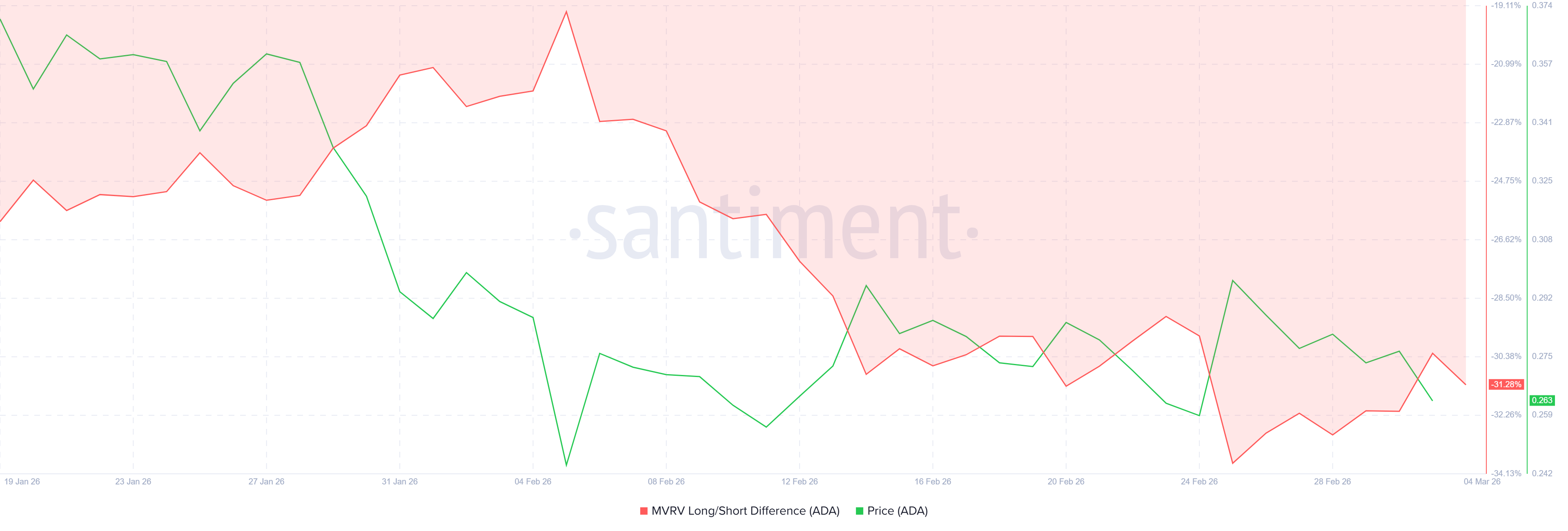

Cardano Risks a 31% Drop as Whales Dump 210 Million ADA

Putin hints that Russia might halt gas deliveries to Europe immediately

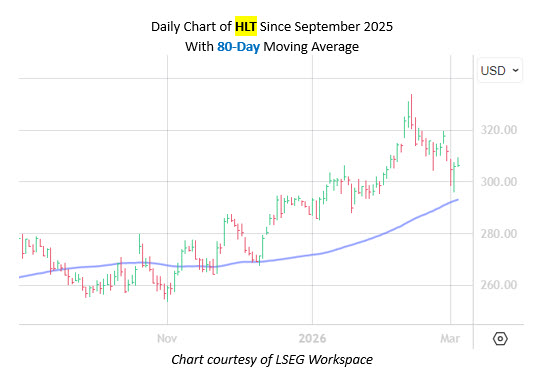

Bull Signal Flashing Amid Hotel Stock Pullback