Gross Bookings Growth Bodes Well for Uber: What's Ahead?

Uber Technologies UBER, the San Francisco-based ride-hailing giant, continues to benefit from robust growth in gross bookings, reflecting strong and sustained demand across its platform. The company has been witnessing healthy double-digit increases in gross bookings in both its mobility and delivery segments.

In the fourth quarter of 2025, total gross bookings rose 22% year over year and on a constant-currency basis as well, with both key segments contributing to the growth. Mobility gross bookings increased 20% year over year and 19% on a constant-currency basis, while the delivery segment recorded growth of 26%. Looking ahead, Uber’s gross bookings momentum is expected to persist in the March quarter despite the ongoing geopolitical turbulence.

The company has projected gross bookings in the range of $52-$53.5 billion for the quarter, indicating constant-currency growth of 17-21% from first-quarter 2025 levels. Sustained growth in gross bookings strengthens Uber’s revenue pipeline, enhances operating leverage across its platform and reinforces network effects between riders, drivers and merchants. This momentum not only supports top-line expansion but also improves the company’s ability to scale profitability over time as higher transaction volumes spread fixed costs more efficiently across its ecosystem.

Comparable Metrics of Other Ride-Hailing Entities

Gross bookings are strong at rival Lyft LYFT as well, mainly owing to the growing active rider base, expansion into new markets and the success of its customer-friendly "Price Lock" feature. In the December quarter, gross bookings increased 19% year over year to $5.07 billion. Management stated that this was the 19th consecutive quarter where Lyft demonstrated double-digit year-on-year growth in the key metric. The uptick was driven by the 18% growth in active riders of 29.2 million. In 2025, Lyft achieved an all-time high of 51.3 million annual riders.

The total number of rides in 2025 increased 14% year over year to 945.5 million, reaching another all-time high. Moreover, the fourth quarter was the eleventh consecutive quarter of double-digit year over year growth with respect to rides at Lyft.

Singapore-based Grab GRAB is benefiting from strong growth in its On-Demand Gross Merchandise Value (“GMV”). On-Demand GMV refers to the sum of GMV of the mobility and deliveries segments. In the fourth quarter of 2025, On-Demand GMV increased 21% year over year at Grab. Grab expects 2026 revenues between $4.04 billion and $4.1 billion, indicating 20-22% year-over-year growth.

UBER’s Share Price Performance, Valuation and Estimates

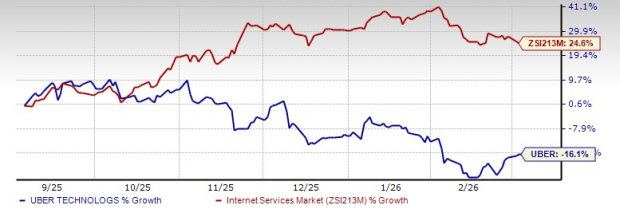

Shares of UBER have declined in double digits over the past six months. Courtesy of the downbeat performance, UBER’s shares have underperformed the Zacks Internet-Services industry over the same time frame.

6- Month Price Comparison

From a valuation standpoint, UBER trades at a 12-month forward price-to-sales of 2.64X. UBER is inexpensive compared with its industry.

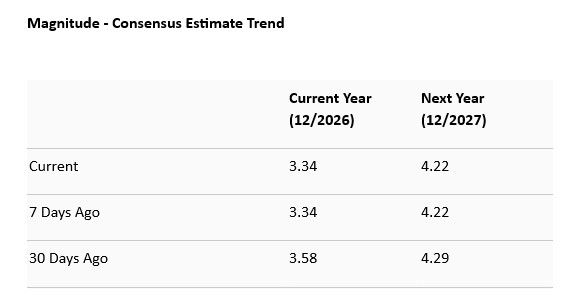

The Zacks Consensus Estimate for full-year 2026 and 2027 has declined in the past 30 days.

UBER's Zacks Rank

UBER currently carries a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

PMGC Holdings Inc. Announces Anticipated Reverse Stock Split

ACRES Commercial: Fourth Quarter Financial Overview

FalconStor Software: Fourth Quarter Financial Overview