Salesforce (CRM): Should You Buy, Sell, or Hold After Q4 Results?

Salesforce Stock Performance: Recent Trends

In the last half-year, Salesforce shares have dropped by 19.8%, currently sitting at $195.64, while the S&P 500 has climbed 5.7% in the same period. This underperformance may leave investors reconsidering their strategies.

Should you consider adding Salesforce to your holdings now, or is caution warranted?

Why Salesforce Fails to Impress

Despite a lower share price, we remain hesitant about Salesforce’s prospects. Below are three key reasons we’re not enthusiastic about CRM, along with an alternative stock we prefer.

1. Sluggish ARR Growth Signals Weak Demand

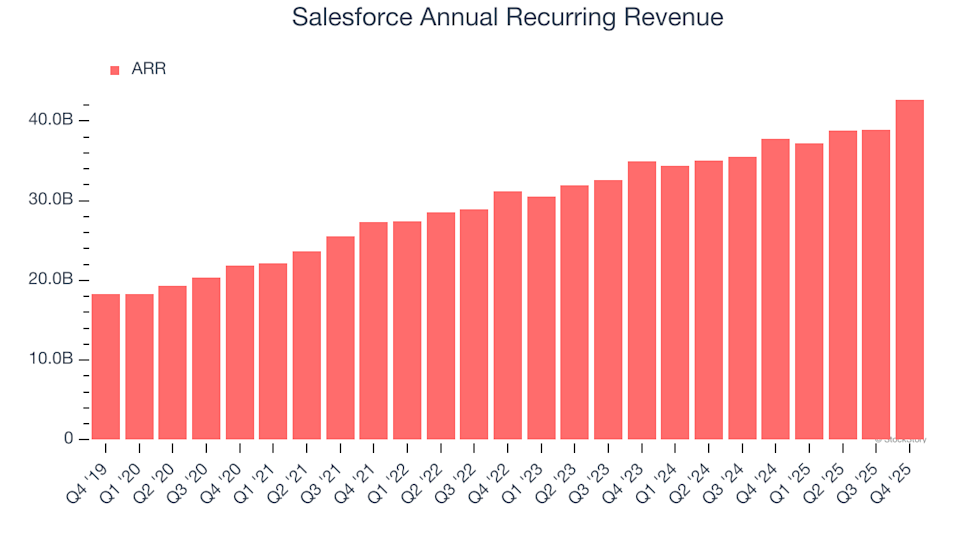

Annual recurring revenue (ARR) reflects the next year’s contracted income from software subscriptions, representing the reliable, high-margin portion of SaaS businesses. Unlike total revenue, ARR excludes lower-margin services like implementation fees.

In the fourth quarter, Salesforce reported an ARR of $42.7 billion. Over the past year, ARR growth averaged just 10.3% year-over-year—a lackluster result that points to mounting competition and challenges in locking in long-term deals.

Salesforce Annual Recurring Revenue

2. Modest Revenue Growth Forecast

Wall Street’s revenue projections offer a glimpse into a company’s future potential. While forecasts aren’t always precise, accelerating growth tends to lift valuations and share prices, whereas deceleration can weigh them down.

Analysts anticipate Salesforce’s revenue will increase by 11.1% over the next year. Although this suggests some momentum from new offerings, it still lags behind the industry average.

3. Operating Margins Improve, Profitability Up

While many software firms adjust earnings for stock-based compensation (SBC), we focus on GAAP operating margin since SBC is a genuine cost tied to attracting and retaining talent. This margin reflects the proportion of revenue left after covering all core expenses, including cost of goods sold, sales, and R&D.

Salesforce’s operating margin has improved by 1 percentage point over the past two years, benefiting from sales growth and greater efficiency. For the trailing twelve months, the operating margin reached 20.1%.

Salesforce Trailing 12-Month Operating Margin (GAAP)

Our Verdict

While Salesforce remains a solid company, it doesn’t meet our standards for quality. After its recent decline, the stock trades at 3.9 times forward sales (or $195.64 per share), which is a reasonable valuation. However, we believe there are more promising investment opportunities available. For those seeking alternatives, we suggest considering one of our leading digital advertising stock picks.

Top Stocks We Prefer Over Salesforce

Don’t Miss: Our Top 5 Growth Stocks — The most successful stocks often share one trait: explosive revenue growth. Companies like Meta, CrowdStrike, and Broadcom were all identified by our AI before their massive runs, delivering returns of 315%, 314%, and 455%, respectively.

Discover which five stocks are on our radar this month—completely free.

Our selections have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which delivered a 351% return over five years. Start your search for the next big winner with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Motorsport Games to Report Fourth Quarter and Full Year 2025 Financial Results

Daktronics to Host Investor Day on April 9, 2026, in New York City

FreightCar America, Inc. Announces Its 2026 Annual General Meeting and Record Date