EMCOR's Electrical Segment Surges in Q4: Structural Upside?

EMCOR Group, Inc. EME delivered outstanding results in its Electrical Construction segment during the fourth quarter of 2025, solidifying its role as a primary engine for the company's structural upside. The segment achieved record quarterly revenues of $1.36 billion, a 45.8% increase year over year, while full-year revenues surged by 51.8%. This strong trajectory reflects a deliberate strategic shift toward high-growth, technically complex end markets and large-scale project execution, positioning the segment for sustained performance at elevated levels.

Growth was underpinned by both higher volumes and a meaningfully improved project mix. EMCOR has increasingly prioritized complex, large-scale contracts with favorable commercial structures, enhancing margin quality and earnings durability. Notably, expansion was not solely data center-driven; roughly half of the quarterly growth stemmed from traditional verticals such as healthcare, institutional and hospitality projects. This diversification, coupled with disciplined execution and rigorous risk management, generated meaningful operating profit leverage and contributed significantly to overall profitability outperformance.

The segment's performance is further reinforced by a record-high $4.46 billion in Remaining Performance Obligations (RPOs) within its network and communications sector, providing strong visibility for the next two to three years. Strategic acquisitions have also played a critical role: the integration of Miller Electric — the largest acquisition in the company's history — has established a significant platform for growth across the Southeast and Texas. Despite a slight year-over-year dip in quarterly operating margins to 12.7%, performance remained well above historical averages, reflecting the segment's high-level technical expertise in areas like Virtual Design and Construction and prefabrication.

By prioritizing technically complex contracts and maintaining disciplined risk management, the Electrical segment has moved beyond cyclical surges and is now positioned for a fundamentally higher level of profitability as it supports enduring secular trends in onshoring, digitalization and grid modernization.

EMCOR’s Competitive Position

EMCOR operates in a highly competitive public infrastructure market alongside established peers, such as Sterling Infrastructure, Inc. STRL and Quanta Services, Inc. PWR, particularly in data center-related projects.

Sterling’s fourth-quarter results were driven by the exceptional performance of its E-Infrastructure and Transportation segments, both of which delivered substantial growth in revenues and adjusted operating income. This success was fueled by robust organic progress, the successful integration of the CEC acquisition and strong project execution. STRL’s Adjusted EBITDA surged 70% year over year to $142.1 million, while gross margin improved 30 basis points to a record 21.7% for the fourth quarter, reflecting improved mix and operational efficiency.

Quanta is a relevant peer with significant exposure to electrical infrastructure and high-demand end markets. Similar to EMCOR, PWR is benefiting from secular tailwinds tied to AI, data centers, electrification, grid modernization and power generation investment. Gross profit increased to $1.22 billion in the fourth quarter from $1.06 billion in the prior-year quarter, supported by higher revenue volume and improved project execution.

EME Stock’s Price Performance & Valuation Trend

Shares of this Connecticut-based infrastructure service provider have gained 17.6% in the past month, outperforming the broader Construction sector and the S&P 500 Index but underperforming the Zacks Building Products - Heavy Construction industry.

Image Source: Zacks Investment Research

EME stock is currently trading at a discount compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 25.85, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of EME

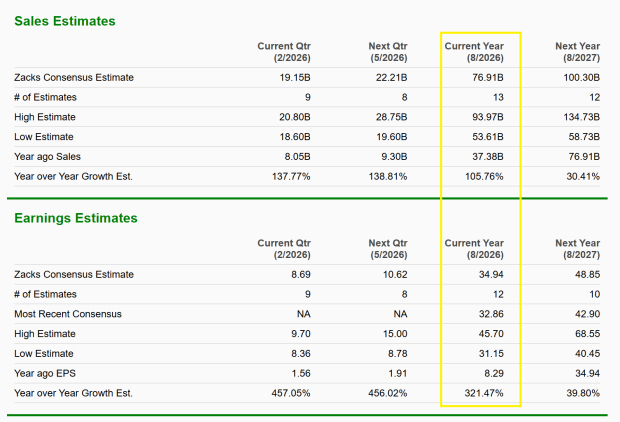

EME’s earnings estimates for 2026 have trended upward in the past seven days to $27.57 per share. The Zacks Consensus Estimate for EME’s 2026 revenues and EPS indicates 6.5% and 6.6% year-over-year growth, respectively.

Image Source: Zacks Investment Research

EMCOR currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why tokenization could make Solana a CLARITY Act winner

The unexpected Iran conflict did not discourage the dovish members of Poland's central bank

Circle's Rally: An Oil, Interest Rates, and Reserves Trade Fueled by Market Momentum

Micron: Why the Recent Pullback is an Opportunity